The February Jobs Report Is Just Plain Ugly

The Jobs Recession Is Getting Worse, Not Better

There is no denying the obvious reality of the February Employment Situation Summary. It blew past “ugly” and landed deep in “fugly” territory.

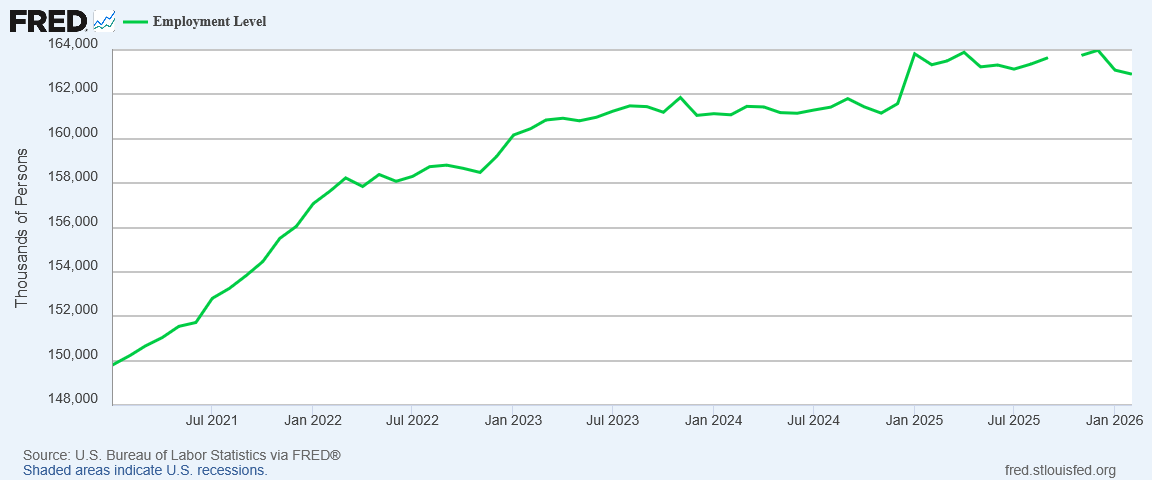

Total nonfarm payroll employment edged down by 92,000 in February, and the unemployment rate changed little at 4.4 percent, the U.S. Bureau of Labor Statistics reported today. Employment in health care decreased, reflecting strike activity. Employment in information and federal government continued to trend down.

There is quite a bit to unpack in this jobs report, and for the sake of clarity and concision I am going to focus on the jobs numbers themselves in this article. Later in the week I shall address data quality and other ramifications of the February jobs numbers separately.

One conclusion is clear: the jobs recession is still getting worse. It is not getting better.

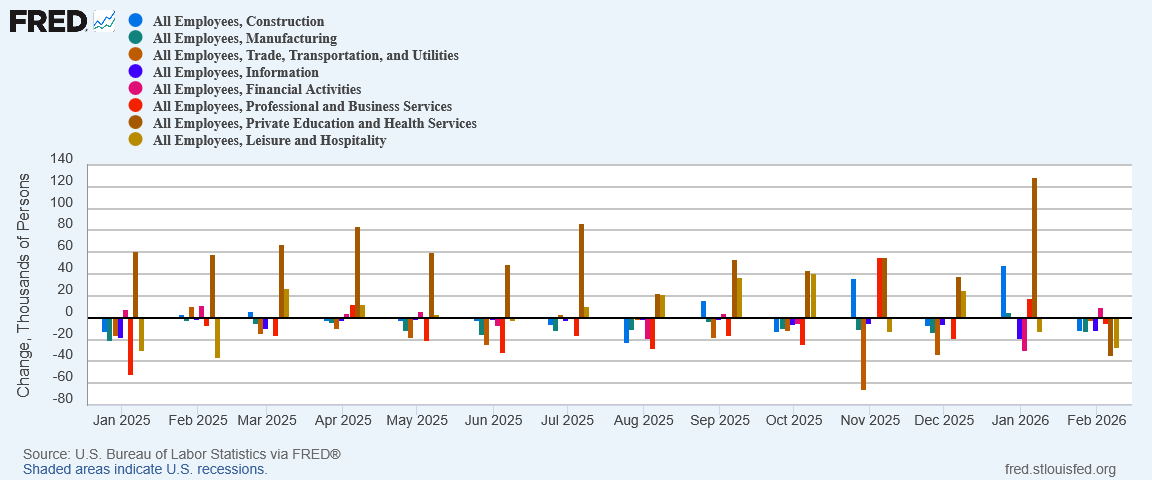

All Sectors Were Down

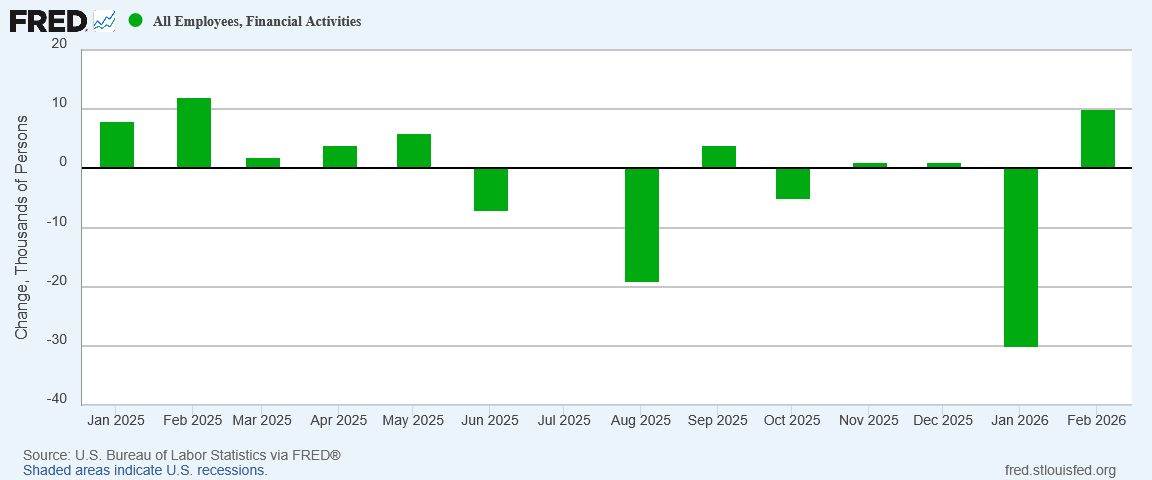

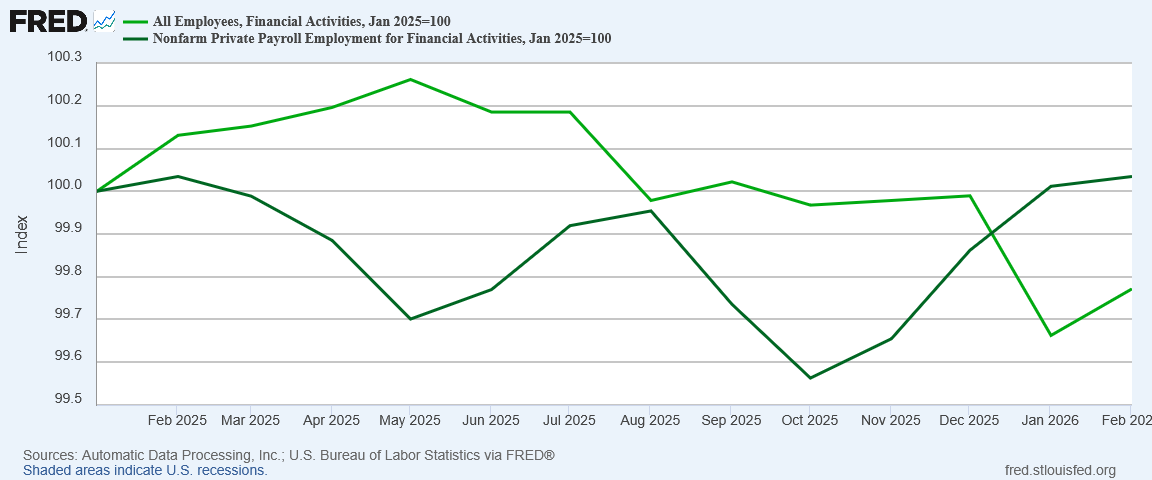

How fugly is the jobs report? Enough so that there is not one single sector that printed good results for February. All but finance posted job losses on the month, and even finance saw only marginal job gains.

The only reason the job gains in finance look at all good is because of how bad job losses in the sector have been over the past year.

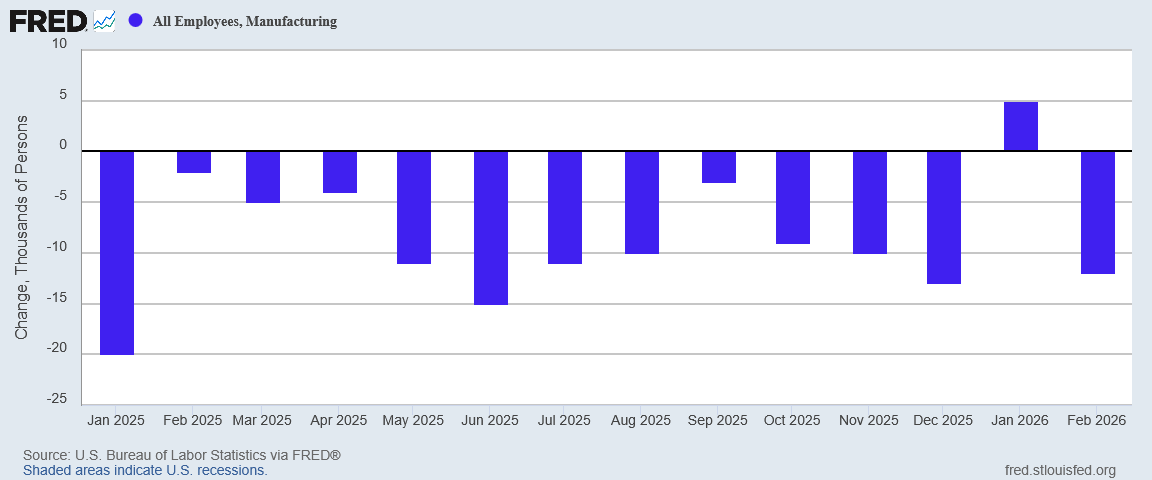

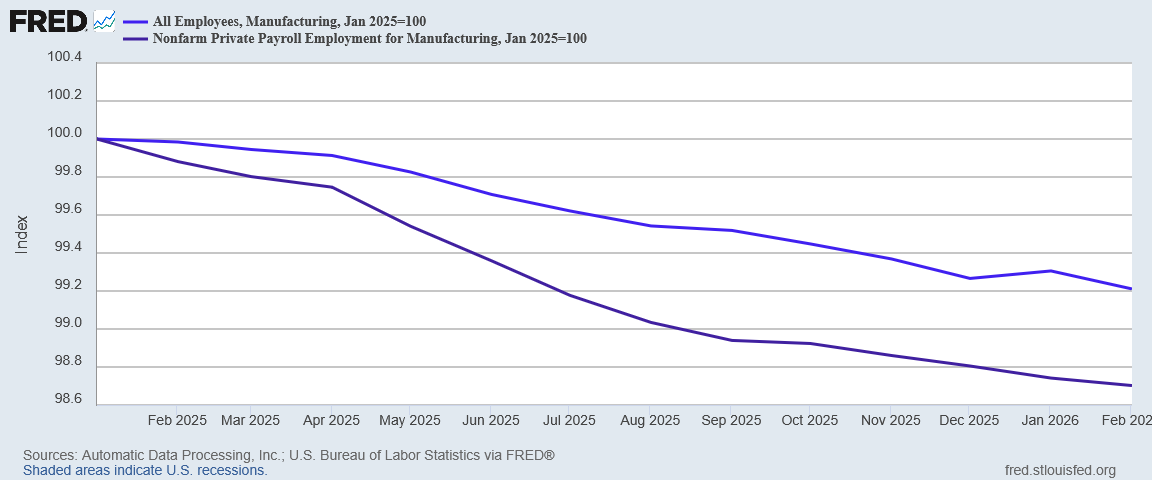

Manufacturing gave up its January gains and then some.

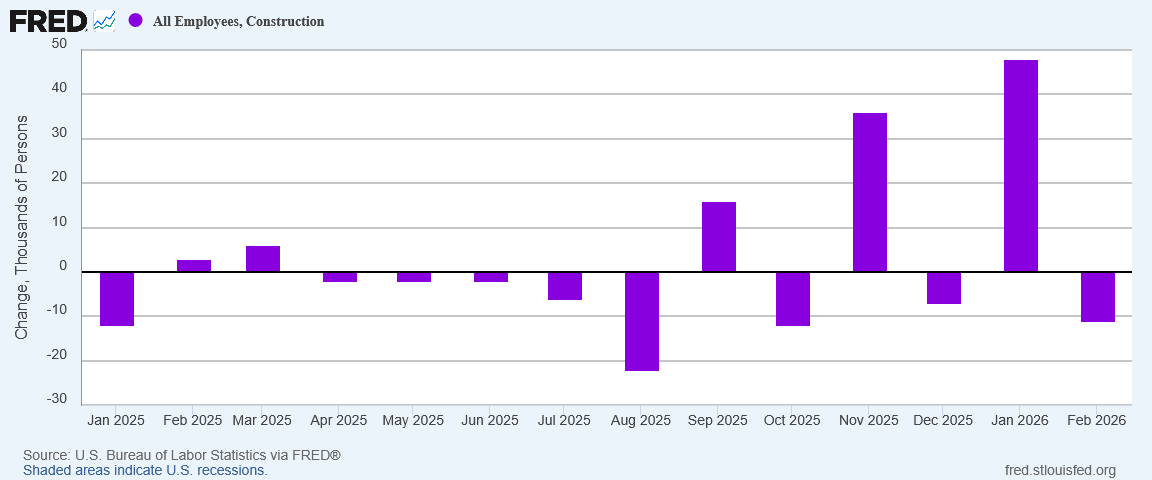

Construction, likely battered by severe winter weather, surrendered 11,000 jobs.

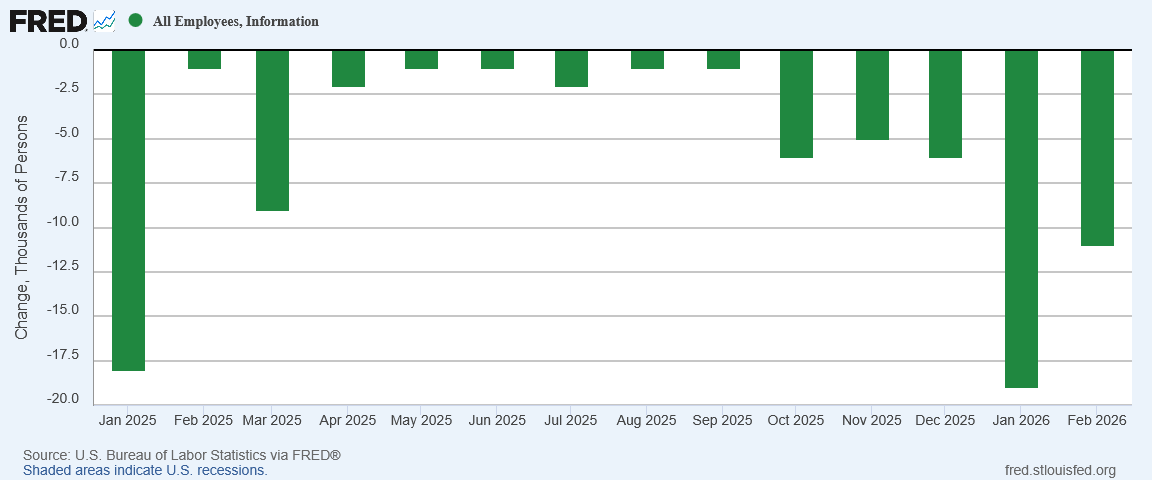

Information posted its fourteenth consecutive month of job losses.

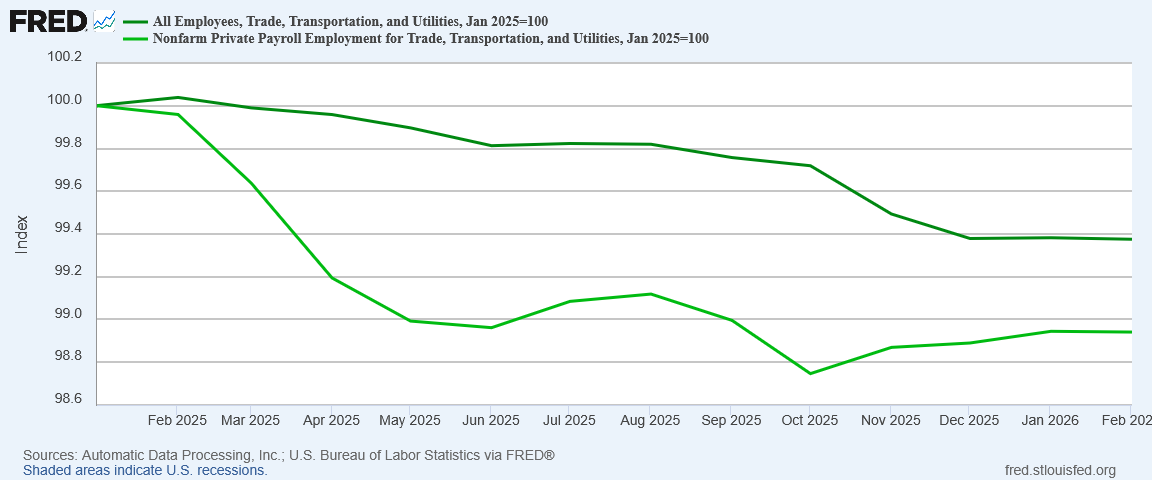

Trade, Transportation, and Utilities, as well as Leisure and Professional Services reversed from job growth in January to job loss in February.

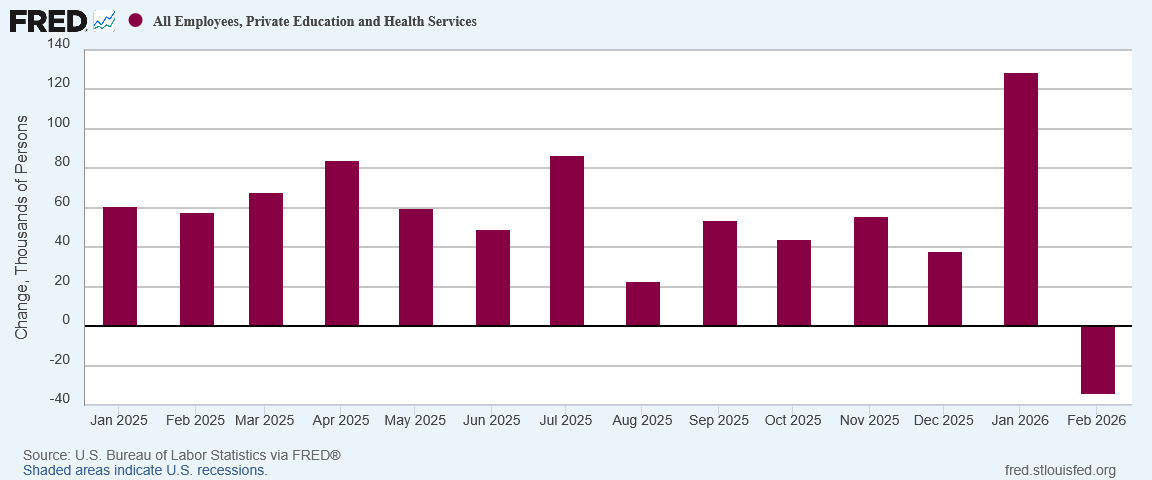

Even Healthcare, which has carried the jobs report in several months, saw job losses in February.

Across the board, the private sector job news was bad.

ADP Was Even Worse In Some Sectors

I have not often made side by side comparisons of the ADP and BLS jobs data, but it is worth noting that, since the start of 2025, ADP has reported relatively greater job loss in key sectors.

Manufacturing job loss from the start of 2025 was a half-percentage point worse in the ADP data set relative to the BLS data.

Trade, Transportation, and Utilities—a significant service providing sector—likewise printed 0.5pp more relative job loss in the ADP report.

Finance, the lone bright spot in the BLS jobs report, was 0.2pp worse in the ADP report.

Construction, Information, and Professional and Business Services saw somewhat less job loss on the ADP report.

Healthcare and Leisure actually saw marginally greater job gains on the ADP report.

While the ADP data posted some interesting divergences from the BLS data across 2025, broadly speaking the two reports show similar jobs trends across sectors—and most of those trends were negative in 2025.

Unemployment Relapse

No matter how we look at the unemployment data, there was a clear relapse in February. Joblessness got demonstrably worse.

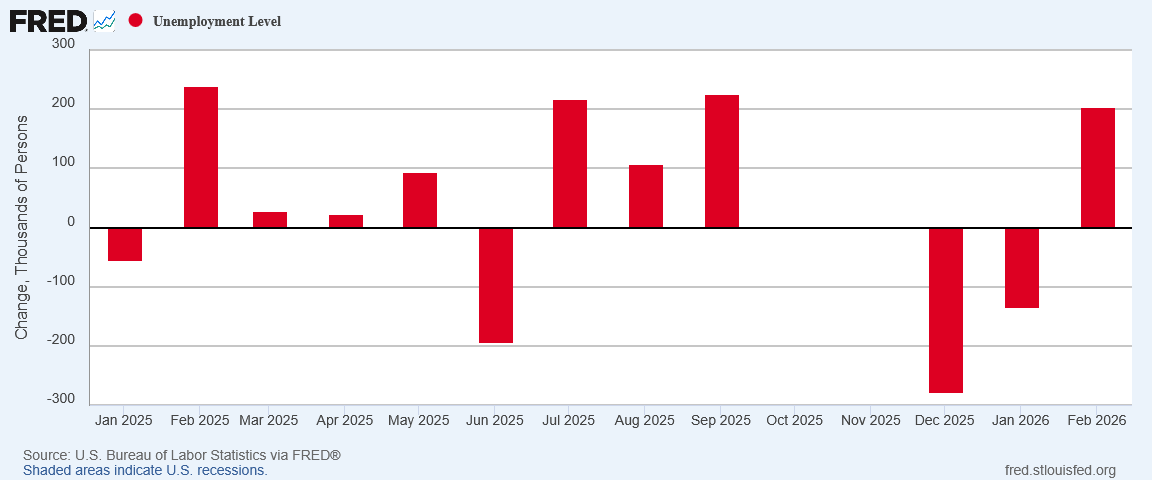

After posting two months of significant declines in the number of “officially” unemployed, February saw the official count surge by 203,000.

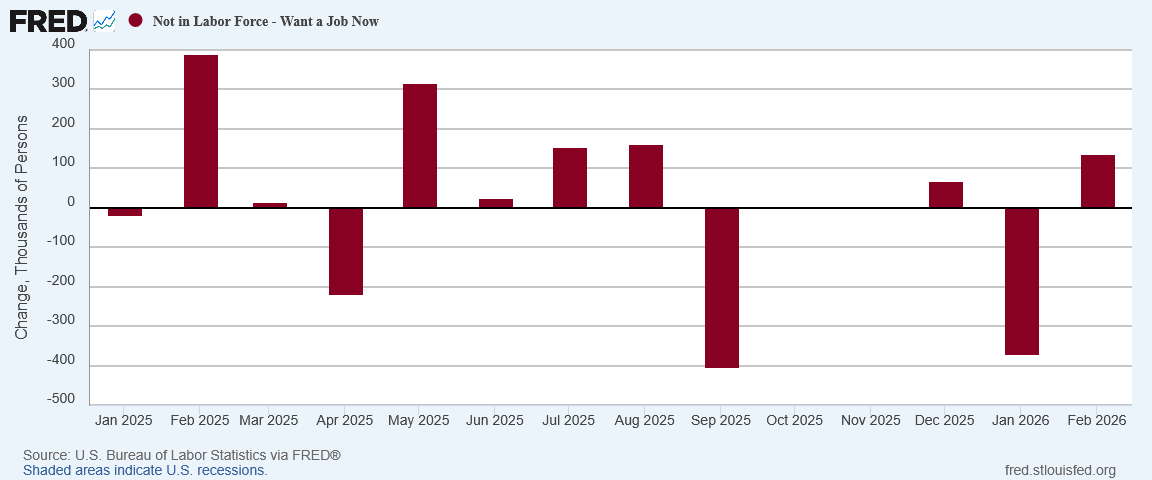

The number of persons technically not in the labor force but who want a job now also rose by a not-insignificant 136,000.

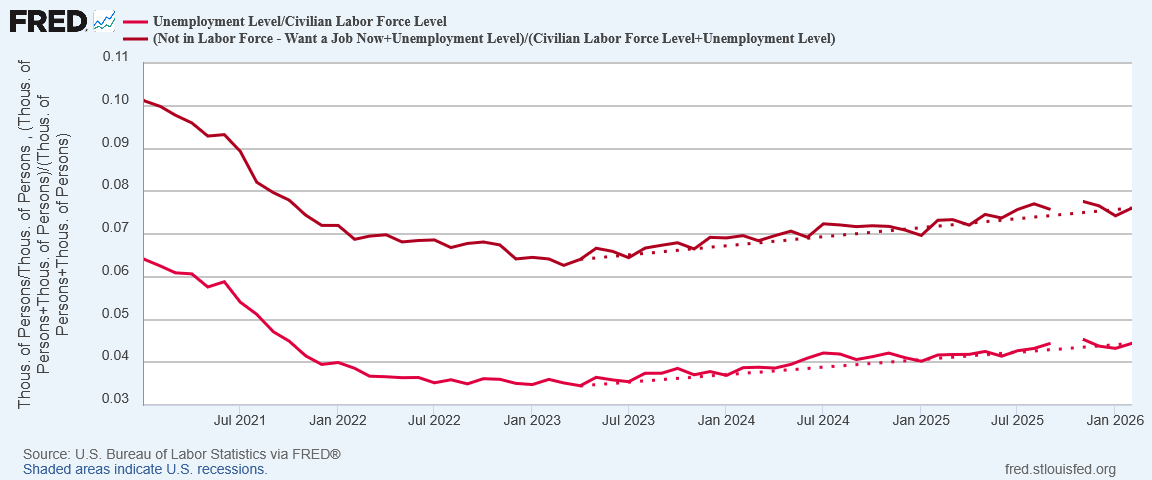

As a direct result of these twin growths in joblessness, both the “official” and the “real” unemployment rate rose by 0.1pp (I calculate the “real” unemployment rate by adding the number not in the labor force but who want a job now to both the size of the labor force and the number of unemployed workers and take a percentage from there.)

By every metric, joblessness moved in the wrong direction in February.

The grim reality driven home by this jobs report is that overall employment plateaued in 2025, and has dropped in the first two months of 2026.

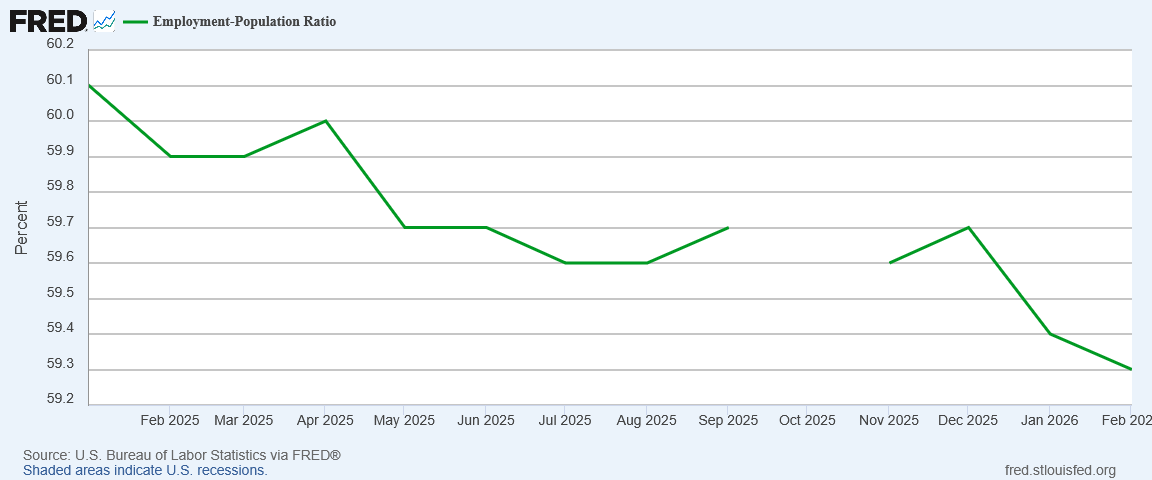

Even when the employment level was more or less steady in 2025, the ratio of employed workers to the overall population dropped by 0.8pp.

The jobs recession which I called in 2024 and which began in 2023 has not gone away. In February, it became demonstrably worse.

America’s jobs markets turned toxic during the Biden years, but thus far President Trump has clearly failed to detoxify them.

When Does It Get Better?

For all of President Trump’s rhetoric about America’s “Golden Age”, the February jobs report is clear on this much: the one group of Americans being left out of that “Golden Age” at present is the American worker.

Workers need work. Workers need jobs. America in February failed to provide those jobs.

Without jobs workers do not get a shot at higher wages—one has to have a wage first before one can aim for a higher wage.

Without jobs workers do not get opportunities to work more hours, thereby boosting the impact of higher hourly wages by increasing weekly earnings even more.

For all of the trade deals that have been signed, for all of the investment commitments that companies around the globe have made to President Trump, job growth is not happening in the United States at present. Job growth has not been happening for a number of years. The downward trend which began under Joe Biden has not been stopped by Donald Trump.

America needs that downward trend to stop. American needs the trend in jobs to be improving and getting better.

When will that downward trend stop? When will the trend get better?

Job growth is the single most effective way to ensure the greatest number of Americans have the greatest participation in the presumptive prosperity Trump touts with his “Golden Age” rhetoric.

America needs factories to start hiring more—and it isn’t.

America needs service producing companies to start hiring more—and it isn’t.

America needs to pull more people off the sidelines and back into the productive economy—and it isn’t.

We are now a full year into the second Trump Administration. President Trump has had a full year to implement his economic policies, and we have had a full year to assess their impacts.

Contrary to the TDS-inflected fears of Democrats and corporate media alike, President Trump’s economic policies have not completely crashed the economy. If Wall Street is any guide, some portions of the economy have done rather well. Inflation has not returned (although that may quickly change as the ramifications of Operation Epic Fury become clear).

What the Employment Situation Summary makes plain is that Main Street is still not doing well. Wall Street may be prospering, but Main Street is not. Main Street is still waiting for its “Golden Age” to arrive. Main Street is still asking when its economy will get better.

The hope is always that President Trump’s policies will yield benefits for everyone including Main Street. In the longer term, they still may, and I certainly hope they do.

In the meantime, Main Street is still waiting for real job growth. February’s Employment Situation Summary reminds us Main Street has yet to see any.

Thank you, Peter, for a sobering view. I’m going to cling to some bits of optimism. Health care jobs are down due to strikes, so that will reverse in time. Construction jobs were hit by severe weather, so that also might surge back with warmer weather. Government jobs have decreased and hey, that’s what I voted for! If the war continues, some of the unemployed will find jobs in the military or in war-related manufacturing.

I get the sense that several aspects of the economy are in a state of flux due to Trump’s policies. If the next item on his agenda is demolishing the drug cartels, that will bring additional fluctuations, as illegals are driven out of the country and addicted individuals are restored to functional living. We seem to be in a period of large, fundamental changes in our economy. Long term, it could work out well, right?