With the November Consumer Price Index Summary due out this morning, it is fitting to take a look at what other inflation metrics are showing, and to note where various forecasters expect consumer price inflation to be for November.

The most notable inflation indicator to come out ahead of the November CPI summary is last Friday’s Producer Price Index Summary, which showed producer price inflation—widely viewed as a leading indicator of consumer price inflation—cooling slightly while remaining high.

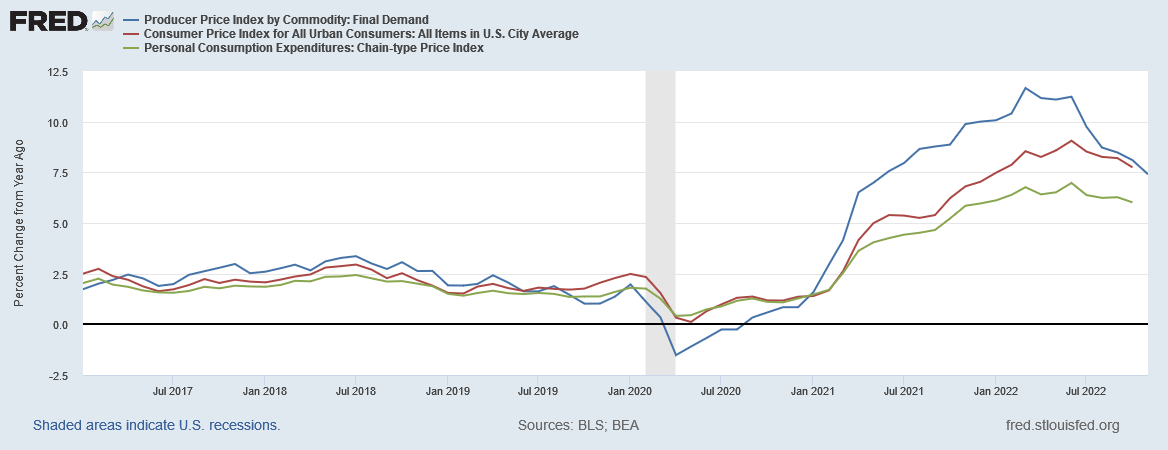

The Producer Price Index for final demand advanced 0.3 percent in November, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices also rose 0.3 percent in both October and September. (See table A.) On an unadjusted basis, the index for final demand moved up 7.4 percent for the 12 months ended in November.

November is the 5th straight month of decline in year on year producer price inflation.

However, month on month producer price inflation cooled only marginally from October, after having risen steadily since June.

The slight rising trend in producer price inflation viewed monthly potentially is one reason the yearly numbers came in slightly higher than many economists had expected.

The Producer Price Index, which measures prices paid for goods and services by businesses before they reach consumers, rose 7.4% in November compared to a year earlier, the Bureau of Labor Statistics reported Friday. That’s down from the revised 8.1% gain reported for October.

US stocks fell immediately after the report, as economists surveyed by Refinitiv had expected wholesales prices to have risen just 7.2%, annually. The higher-than-expected inflation readings raised concerns about whether the Fed will be able to slow the pace of rate hikes.

The producer price index arguably shows that inflation is cooling, but only slightly, and may even be in a transitory trough prior to a rise in the annual inflation rates beginning early next year. At a minimum, the PPI is showing that inflation is not cooling “fast enough” to expect the Federal Reserve to moderate much its stance on rate hikes—and the next Fed rate hike is scheduled for Wednesday afternoon (December 14th).

Still, producer price inflation for consumer energy goods is continuing to decline, which indicates that energy price inflation will continue to recede for the near term at least.

However, producer price inflation for final demand foods rose sharply, both year on year and month on month.

This does not augur well for future food price inflation within the CPI.

This somewhat contradictory set of inflation trends within the PPI, coupled with the rising personal income data from the BEA’s Personal Income and Outlays Report for October is undoubtedly one of the factors leading the Cleveland Federal Reserve’s inflation nowcast to show only a modest decline in consumer price inflation to 7.49% year on year for November at the headline level, down from October’s 7.7%

The Cleveland Fed’s nowcast is approximately 0.2% higher than the forecasts by economists polled by the Wall Street Journal.

If the forecast is spot on, the annual rate of inflation would taper off to 7.3% from 7.7% in October and a peak of 9.1% in June.

The CrowdWisdom LIVE forecast for November consumer price inflation is at roughly the same level.

Our Forecast for US Inflation in November is 7.0% to 7.3%.

Our Forecast for July was 8.5 to 8.9%, Actual at 8.5%

Our Forecast for August was 7.9 to 8.3%, Actual was 8.3%

Our Forecast for September was 8.1 to 8.4%, Actual was 8.2%

Our Forecast for October was 7.7% to 8.0%, Actual was 7.7%

Based on recent months’ forecasts, CrowdWisdom has a decent record for forecast accuracy, which suggests that year on year consumer price inflation for November will be around 7.3%, and possibly slightly lower.

What the PPI indicates—and what economic forecasts predict—is that the CPI will continue its marginal cooling trend, but consumer price inflation per the CPI will likely remain above 7% for November. Inflation is coming down, but only by the tiniest of steps relative to where the Fed would like it to be.

The PPI confirms the cooling trend that has been shown by all the major inflation metrics—PPI, CPI, and PCE.

This marginal cooling trend in consumer price inflation puts the Fed in something of a bind. On the one hand, inflation is coming down, and, most importantly, inflation has not been going up in recent months.

However, despite the declines to date, consumer price inflation is remaining stubbornly high, which raises the question of how large should Wednesday’s rate hike be?

If the forecasts are accurate, a 7.3% annual inflation rate for November would be a 1.8% decrease from June’s inflation peak, which is roughly the same percentage point decrease from peak inflation over the subsequent five months during the Volcker Recession of the early 1980s.

At that time, then Fed Chairman Paul Volcker opted to keep up interest rate pressure even as inflation continued to subside. If current Fed Chairman Jay Powell follows the Volcker script, he very likely will push for yet another 75bps rate hike, rather than the 50bps hike that Wall Street as a whole is anticipating.

If the CPI should come in much higher than 7.3%, Powell is almost certain to push for another 75bps rate hike on Wednesday. If the CPI prints significantly below 7.3%, the pressure will quickly mount on Powell and the Federal Reserve to keep the Wednesday rate hike to at most 50bps.

How much impact even a 75bps rate hike can have is at this juncture fairly problematic, as the Federal Funds rate is already higher than the 5 Year and 10 Year Treasury yields.

The murkiness and contradictions contained within the available inflation data and current forecasts ultimately illustrate the limitations of the Fed’s data dependent approach to rate hikes. When the data shows no clear and emphatic trend for inflation, either up or down, selecting the size of the next rate hike quickly reduces to little more than guesswork by the Fed. No matter how Jay Powell will attempt to gussy up the next rate hike with references to a variety of economic data, the reality of the next rate hike is that Powell would be just as effective in hiking rates by throwing a dart at a target on the wall.

When today’s CPI print comes out, we are likely to see inflation has cooled a little. It will be something of a surprise if we find that inflation has cooled by a lot, and only slightly less of a surprise if we should learn that inflation has cooled not at all.

With the government spending worse than drunken sailors?

At least the sailors spend their own money!

I wonder how much what we don't know is going to hurt us?

And America is still the best place to put your money?

At this rate, how long can that last?