Fed Chairman Jay Powell made his view of the US labor market crystal clear in his brief address at Jackson Hole last Friday: The US labor market is strong and resilient—and that’s the problem.

The U.S. economy is clearly slowing from the historically high growth rates of 2021, which reflected the reopening of the economy following the pandemic recession. While the latest economic data have been mixed, in my view our economy continues to show strong underlying momentum. The labor market is particularly strong, but it is clearly out of balance, with demand for workers substantially exceeding the supply of available workers. Inflation is running well above 2 percent, and high inflation has continued to spread through the economy. While the lower inflation readings for July are welcome, a single month's improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down.

As regular readers of this Substack already know, I have a rather different take on America’s labor markets.

What Powell simply will not acknowledge is that the jobs numbers simply do not add up, and have not added up for quite a while now. Far from being strong, US labor markets are simply dysfunctional, and toxic rather than tight.

With the July Job Openings and Labor Turnover Survey due out later this morning, the question must be asked: will that report support Powell’s view of the labor market or will it support mine?

Headline Numbers Will Look Good

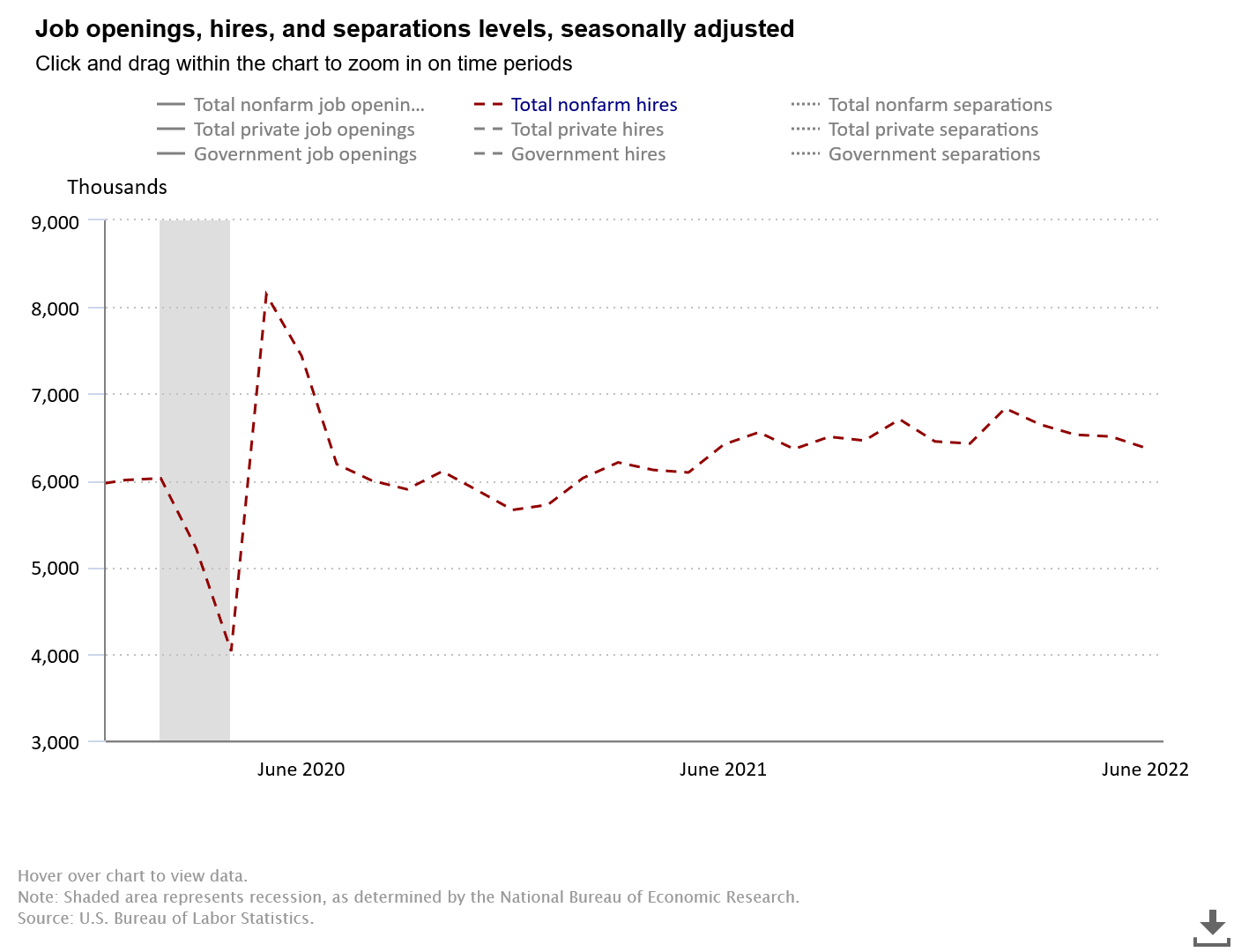

On the surface, the June JOLTS report portrayed a labor market with a fair amount of strength that was only just beginning to recede. How else to view a jobs market where there are more reported jobs openings than there are unemployed workers to fill them?

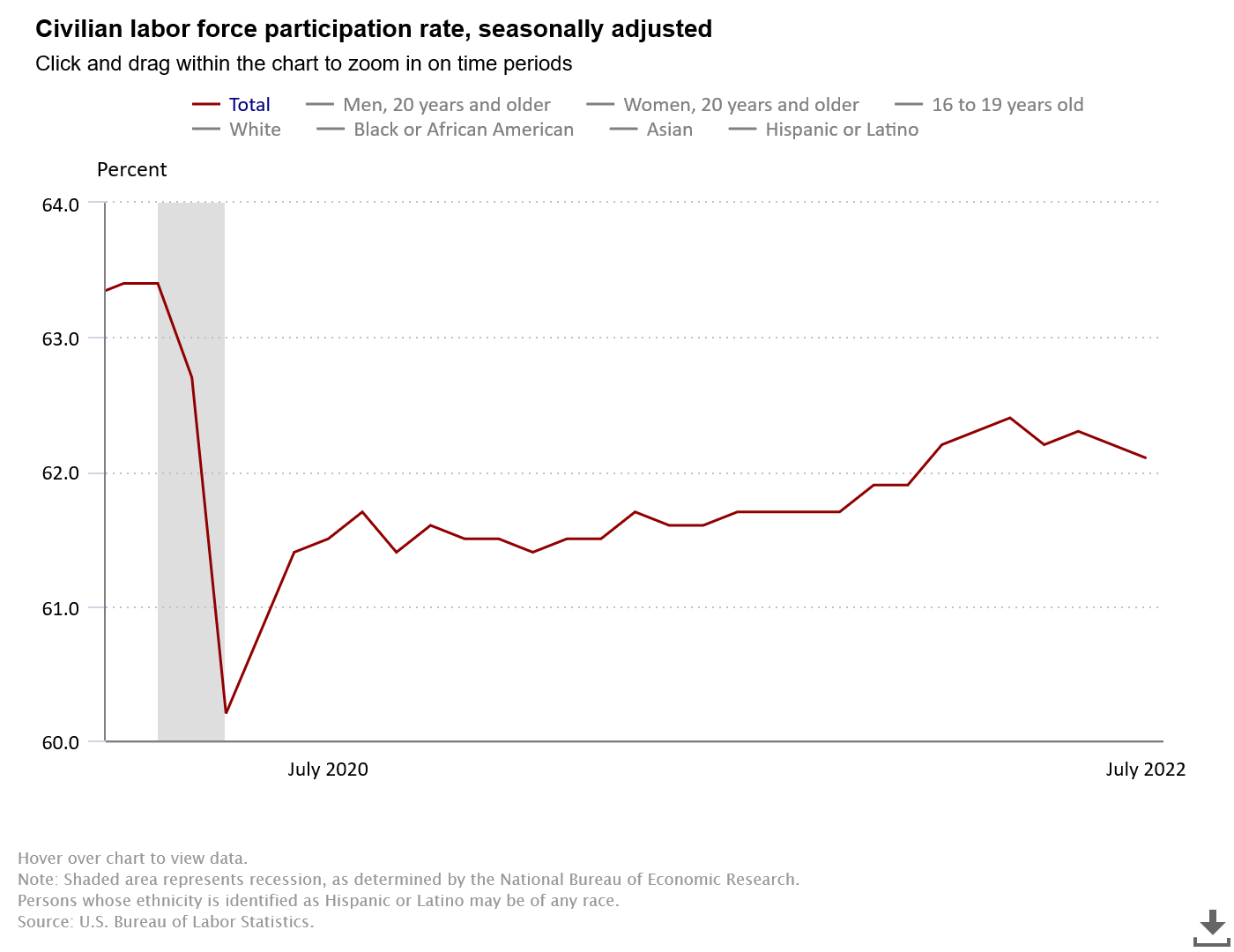

However, that view overlooks the reality of poor labor force participation, which actually decreased in July (one of many reasons the July Employment Situation report is little more than an exercise in Lou Costello Labor Math).

As I noted while assessing the July Employment Situation Report, the decrease in labor force participation accounts for nearly all of July’s decline in the number of unemployed1.

What Powell likely wants to see is a greater decline in the number of reported job openings, even though the seasonally adjusted number of hires has itself declined every month since March.

Jobless Claims Are Rising…Aren’t They?

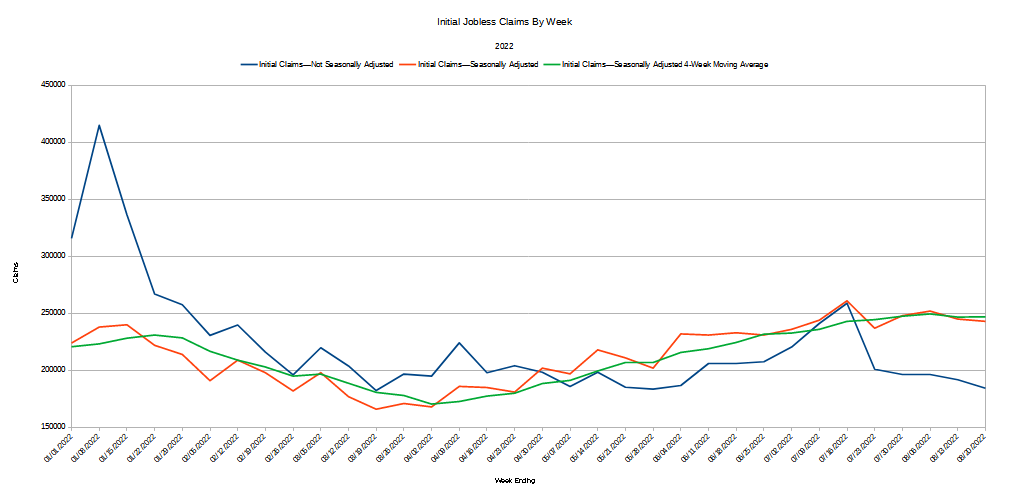

Jobless claims data notionally would offer some insight into the strength of the labor markets, but that data is also questionable. While the data shows the seasonally adjusted number of initial jobless claims in the US trending up since April, the unadjusted figures break sharply down from the seasonally adjusted figures beginning in the middle of July.

Normally, adjusting unemployment claims data for seasonal variances makes sense, as a number of jobs have seasonal aspects. However, a sustained deviation between the raw unadjusted claims numbers vs the seasonally adjusted ones has emerged since the middle of July,

Will the July JOLTS report pick up on this unusual signal?

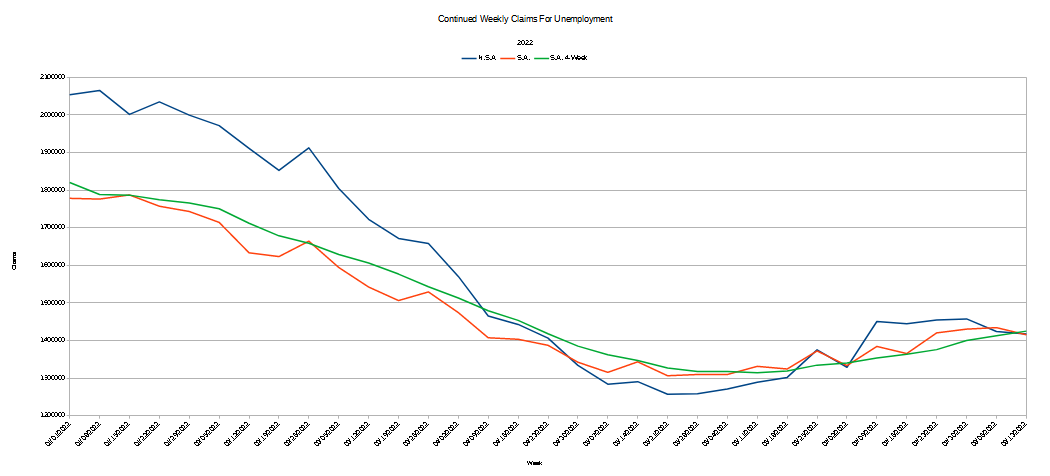

Lending weight to the seasonally adjusted initial jobless claims in spite of the anomalous behavior of the unadjusted data is the data for ongoing jobless claims. The seasonally adjusted moving average shows that continuing jobless claims—claims for unemployment insurance benefits after the first week—have been trending up since May.

Unlike the initial claims data, the raw data does not show any unusual deviation from the seasonally adjusted figures.

Excepting the unadjusted initial claims figures, the unemployment benefits data indicates that joblessness is on the rise in the US, despite the supposed “decline” in unemployment to 3.5% in July.

Will the JOLTS report be in line with a continued increase in unemployment?

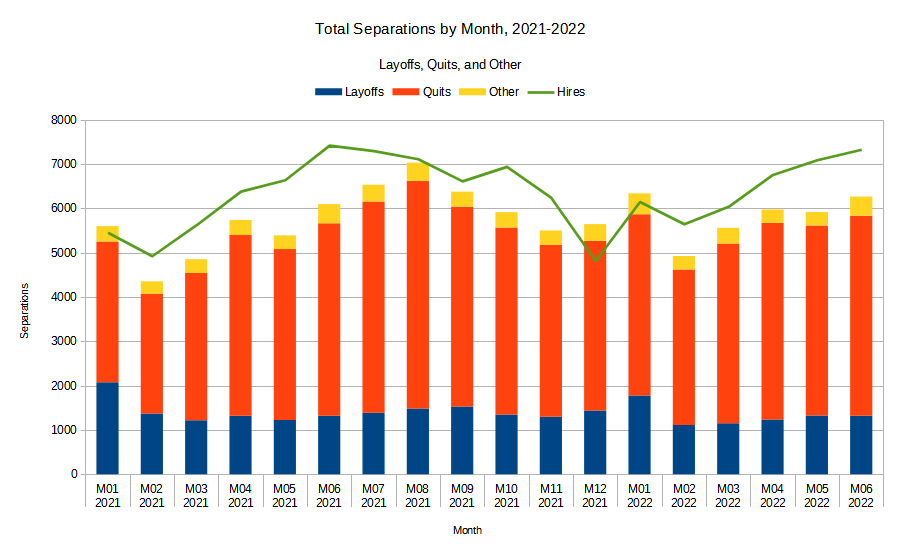

Hiring Has Been Outpacing Separations

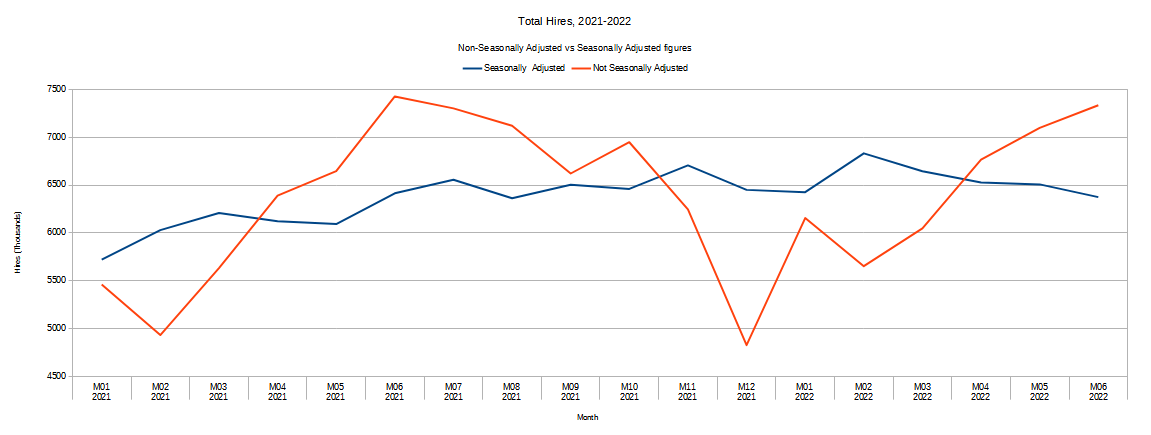

One data set that does show inarguable strength in the labor market is the pace of hiring relative to separations. Even as hiring has declined in recent months, the pace of reported hiring has surpassed the pace of reported job separations (not seasonally adjusted) in this country.

Here also, we encounter another anomaly in the reported data, as the unadjusted figures show hiring increasing since February, while the seasonally adjusted figures show hiring decreasing.

While some variance due to seasonal adjustment is to be expected, the function of seasonal adjustments is to smooth out data fluctuations that occur solely because of recurring seasonal patterns that exist independent of overall economic conditions. Thus, when the unadjusted and seasonally adjusted data diverge for multiple months, the accuracy of the adjustment calculations should be called into question.

At a minimum, this divergence is yet another reason the jobs figures reported by the government each month should be viewed with extreme skepticism. We have more than a few reasons to suspect the data is tainted.

Still, when we look at the unadjusted numbers, hiring has been outpacing separations since February, and has been trending up every month this year—to the extent that the total hires exceeded total separation by more than a million jobs in June.

The unadjusted numbers also show the number of quits—voluntary separations—increasing every month since February. There is plenty of hiring activity going on—but people do not appear to be staying settled in their jobs, and there is significant churn in the labor markets at present.

This churn, coupled with a gradual rise in layoffs throughout the year to date, does not reconcile well to Powell’s perception of labor market “strength”. Strength in labor markets would show sustained hiring growth without the rising quits and layoffs.

What To Look For In The July JOLTS Report

The one thing that is certain about the upcoming JOLTS report is this: the headline numbers will not tell the real jobs story in this country any more than the headline employment numbers do. To apprehend the state of labor markets in this country, one will have to peel apart the data to view what lies beneath the headline numbers.

Compare the seasonally adjusted figures to the reported raw data. Will the apparent divergence in total hires continue?

Look at the unadjusted number of quits. Is the “Great Resignation” an ongoing phenomenon or has it begun to abate? Quits are a sign of labor market churn, and arguably point to instability in labor markets, which, while not exactly a sign of weakness, could tend to undermine an assessment of labor market strength.

Are unadjusted layoffs increasing or decreasing? Increasing layoffs would be a sign of labor market weakness.

Is unadjusted hiring exceeding unadjusted separations? Such excess is perhaps the best argument in favor of Powell’s perception of labor market strength, so the continuation of that phenomenon bears close scrutiny.

The stronger the labor markets appear, the more justified Jay Powell will feel in sustaining increased interest rate hikes. The weaker the labor markets become, the weaker that justification and the less defensible Powell’s rate hikes become.

Paying attention to the subtle signals of strength and weakness in labor markets—something neither Powell nor anyone else in government is doing at the moment—will give the clearest indication of the degree of economic damage Powell’s rate hikes are likely to do going forward. Because Powell is not viewing the jobs data with a critical eye, the one certainty that exists is that his rate hikes are going to do damage, for the simple reason that he is not assessing the impacts of the rate hikes at all, but simply using them as a sledgehammer against rising consumer price inflation.

Sledgehammers swung wildly tend to break things, and Powell’s rate hikes are going to be no exception.

The BLS requires that one be “actively” looking for work to be counted among the unemployed. Otherwise, a person is simply counted as out of the labor force.

Toxic indeed. Way too many employers are still requiring proof of clot-shots for new hires.

Ignore the adjustments. In the end that doesn't matter. You have a job or not. Of course traditionally these adjustments made sense, as during certain periods there are more temp-jobs and you want to smooth that out. But in the end jobs-offers are not declining and people are not mass-fired. So it seems this time it is mostly Big Money that will need to eat the correction and not so much the little guy.

I don't think Powell knows what he is doing, but at least he is making the right moves: rates up-up-up. It won't stop inflation, as that was just the extra money placed in circulation in '20/'21, but rates need to go up to have any chance of not having a total system collapse down the road. It may be too late, but we got to try. And if it is not hurting jobs, I see no reason to stop now. Not at least until saving rates are back at 4% and bonds somewhere just below.

Yes that will hurt, but it is more like the cancer patient needing surgery. Not doing it is worse.