Employment Situation Summary: Not A Blood Bath, Still Not A Good Jobs Report

Despite High Expectations, The Reality Remains Underwhelming

After the blood bath that was the October Employment Situation Summary, the Bureau of Labor Statistics was mathematically certain to issue a better report for November—and the BLS succeeded in getting over that bar.

That was about the only way the BLS exceeded expectations.

Economists largely shrugged off October’s horrific numbers in predicting moderately robust job growth for November.

Economists predict an increase in nonfarm payroll employment of 215,000 in November, according to FactSet. That would follow an increase of just 12,000 in October, which was far below the forecast of 120,000. The Bureau of Labor Statistics noted that hurricanes Helene and Milton and strikes in the manufacturing sector likely depressed hiring activity.

On the surface, the November Employment Situation Summary exceeded that expectation.

Total nonfarm payroll employment rose by 227,000 in November, and the unemployment rate changed little at 4.2 percent, the U.S. Bureau of Labor Statistics reported today. Employment trended up in health care, leisure and hospitality, government, and social assistance. Retail trade lost jobs.

However, as per usual, once you unpack the numbers and look at the details underneath, the results quickly start to underwhelm.

Alas, the jobs recession still has not gone away.

The first noticeable miss was in private sector employment, which missed economists’ estimates by around 6,000 jobs.

Private sector payrolls expanded by 194,000, close to the 200,000 expected. Retail trade lost 28,000 jobs, suggesting softer than usual seasonal shopping hiring. Warehousing and transportation added a slight 3,400 jobs.

With private sector job growth coming up short, that means that government jobs were what pushed job growth over expectations.

There was, however, one nice surprise in the jobs report: for only the fourth time this year, the revisions for the prior two months were to the upside.

The change in total nonfarm payroll employment for September was revised up by 32,000, from +223,000 to +255,000, and the change for October was revised up by 24,000, from +12,000 to +36,000. With these revisions, employment in September and October combined is 56,000 higher than previously reported.

While the increases are undeniably positive news, they still leave job growth during October at an anemic 36,000 jobs across all industries.

This was where the good news ended.

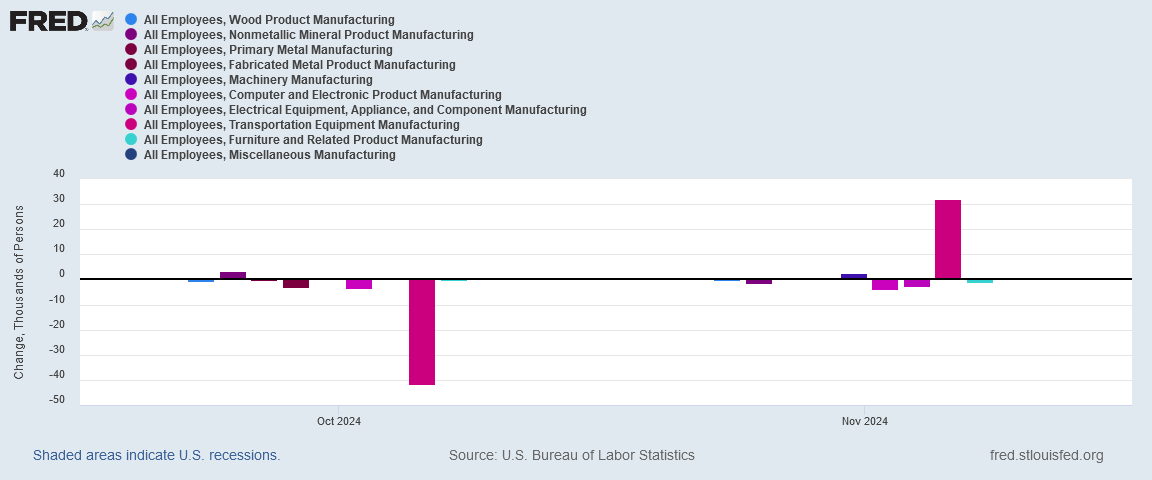

Manufacturing remains weak—and getting weaker, looking at the overall trend.

The only reason Manufacturing posted any jobs gains at all is because some 32,000 workers returned from being out on strike (i.e., Boeing). But for that healthy dollop of transportation-related jobs, there would have been no manufacturing job growth at all in November.

Outside of Transporation Equipment Manufacturing, the story on Manufacturing jobs was the same that it has been all year: mostly job losses and not job gains.

The jobs recession in Manufacturing is not going away, not in the slightest.

The ongoing softness in Manufacturing is very likely one reason the unemployment rate ticked up by a tenth of a percentage point in November, to 4.2%

For all of the White House talk about creating jobs, the reality of the jobs market has been that the unemployment rate has been steadily rising since early 2023. Rising unemployment is hardly a signal of economic strength or robustness.

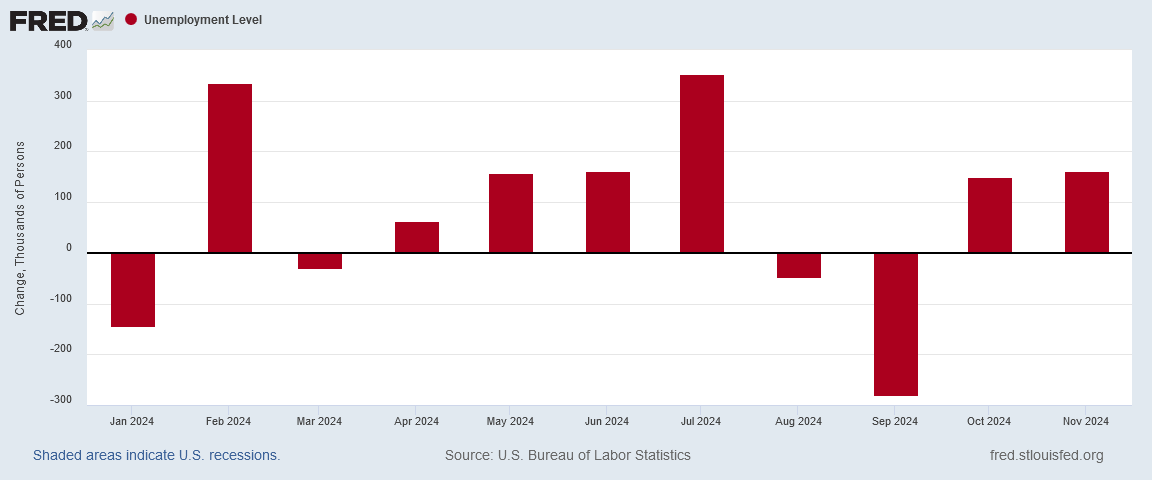

In human terms, that tenth of a percentage point increase meant that 161,000 workers joined the ranks of the unemployed in November.

Notably, the November increase in the number of unemployed exceeded that for October, meaning more people either lost their jobs in November or struggled to find work after being out of the labor force. Losing one’s job or not being able to find a job are also not signs of a strong economy.

A far more concerning metric, however, is the declining Employment-Population Ratio, which fell again in November.

The “Never Trump” cohort within corporate media will come unglued to be confronted with this, but the highest Employment-Population Ratio this country has had in the past 15 years at least was in February 2020, just before the COVID Pandemic Panic, during Donald Trump’s first term of office.

In many respects this percentage is a more meaningful metric than the official unemployment rate. The Employment-Population Ratio charts what percentage of the overall population is gainfully employed. If that ratio is decreasing, even if absolute job numbers are increasing, the overall population is increasing faster, and that means more and more people do not have jobs.

For young people especially, this is cause for grave concern.

We should be especially concerned about the declining employment population ratio for the younger age brackets. A declining ratio among young people means an increasing number of people in the 16-24 age range who are not gainfully employed. That’s an increasing number of people in the 16-24 age range who are not learning the skills they need in order to work—they are not mastering a technical skill of some sort and they are not mastering the “soft” skills necessary to navigate the workplace. Unemployed youth are a far greater economic concern than the unemployed in all other age groups simply because the economic costs of that unemployment are much longer lasting.

The declining ratio in November tells us we still need to be gravely concerned.

With such displays of weakness in the overall employment picture, it comes as no surprise that Manufacturing is the source of the greatest weakness.

Manufacturing employment has actually been declining over the past few months, and only reversed in November. However, even more concerning is that Manufacturing job growth plateaued in October 2022, and has not appreciably increased since then.

How much manufacturing job growth has there been in this country over the past couple of years. Not only zero but actually less than zero. Once again the data shows that we’re shedding manufacturing jobs in this country. Jobs that are about making “things” are simply not on the increase in this country.

Further, if we index Manufacturing and Total Private Employment from January of 2021, we see that the weakening trend began early on in the (Biden-)Harris Administration, as Manufacturing diverged from Total Private Employment almost immediately in 2021.

That divergence magnified in October, 2022, when Manufacturing job growth in this country more or less stopped.

If Manufacturing isn’t providing all the new jobs in this country, what is? Two things: Services and Government.

By far, throughout all of 2024 Service-Providing job gains have outpaced both Goods-Producing jobs gains and Government job gains.

However, if we ignore Service-Producing job gains, we quickly see that Government jobs have produced far more gains in 2024 than Goods-Producing jobs.

November was in fact only the second month all year that Goods-Producing jobs (barely) outpaced Government jobs. In all other months, Government jobs grew considerably more. About the only thing of which we seem to be making more is government bureaucracies.

That is not a healthy trend—not economically and certainly not politically.

The softness in Goods-Producing jobs, especially the Manufacturing jobs subset, becomes readily apparent when we see how full-time employment is declining in this country.

While Full-Time Employment was increasing fairly steadily in 2021 and early 2022, that growth began to weaken in mid-2022. Since the spring of 2023, Full-Time Employment has been declining in this country, and only three months in 2024 have seen Full-Time Employment increase.

People working less is never a good economic signal—and that is what we have happening in this country: people are working less.

The decline in Full-Time Employment quickly brings our attention around the that population cohort Not In the Labor Force, a cohort which began to increase in earnest in this country right around the time that Full-Time Employment began to falter.

This is a red alert at the most fundamental level of the economy. When this metric rises, people who were employed but fell out of employment not only became unemployed, but they quickly fell out of the labor force as well. These are people who not only do not have a job, not only are not actively looking for a job, but are without a job and have, in large measure, resigned themselves to not having a job.

This is not good for any economy. As a general rule, populations not in the labor force need to be drawn back into the labor force. Instead, in the US economy more and more people are being added to their number.

Even when people are working, they are still working less, as the Average Hours Worked per Week has been declining since at least 2021.

The one cause for hope with the Average Hours Worked is that it has been fluctuating between 34.2 and 34.3 hours per week since April. For now at least, there has been a floor established on the number of hours people are working each week. However, in order for there to be meaningful economic expansion, people have to be working more hours, not fewer. In economic terms, more work is always far better then less.

When we look at all of these metrics together, there is one detail that is important to note: Nearly all of them have an inflection point sometime between late 2022 to early 2023.

As I have said repeatedly over the past few months, America is in an extended “jobs recession.”

Regardless of what other economic metrics may show, the employment metrics have for well over a year now shown weakness and decline.

Fewer people are working full time jobs.

People are working fewer hours.

People are working fewer manufacturing jobs.

Relative to America’s growing population, fewer people are working, period. More and more people are either unemployed or have dropped out of the labor force altogether.

For the high expectations of economists and “experts”, the reality revealed by the details within the jobs report remains completely underwhelming.

It is foolish to talk of economic growth when there is not also job growth—and despite what the top-level numbers show, when you peel the layers back and examine the gory details of the Employment Situation Summary, the one thing you do not find is job growth.

When you peel the layers back and examine the gory details of the Employment Situation Summary, what you find is declining employment.

When you peel the layers back and examine the gory details of the Employment Situation Summary, what you find is rising unemployment.

When you peel the layers back and examine the gory details of the Employment Situation Summary, what you find is a rising number of people not in the labor force.

The November Employment Situation Summary is not the jobs bloodbath the October report was. That is not enough to make it a good jobs report, and, in the details, it is apparent that it is not a good jobs report.

As usual, will be be waiting for the revised numbers.

Biden/Harris was slipped in under the radar while OWS was running full tilt after COVID was 'released' into Erde's human population (Mistake? Deliberate? Pick one of two....) and what protections had existed for maybe decades for 'free and fair' elections were swept to the roadside to defeat Trump.

The collateral damage that resulted pretty much killed whatever resurgence of productive employment might have benefitted the US economy, given the yet-persistent 'work-at-home' rules for Government employees (the surge we saw) vs. employees who can't Work @ Home, because that's not where their jobs exist!

Oh, and the inflation from 'free' money handed out with abandon to citizens and illegals.

We'll have to wait for Act II in 2026 to see what lasting effects the Election of 11/24 brings us. The lawfare of 2021 - 2024 certainly turned a lot of voters towards Trump who then voted their preference over a VP Roundheels Presidential candidate while the Lame Duck in Chief hands out pardons for crimes – and crimes only thought about, if not actually committed – while his ice cream melts and his Depends fills.