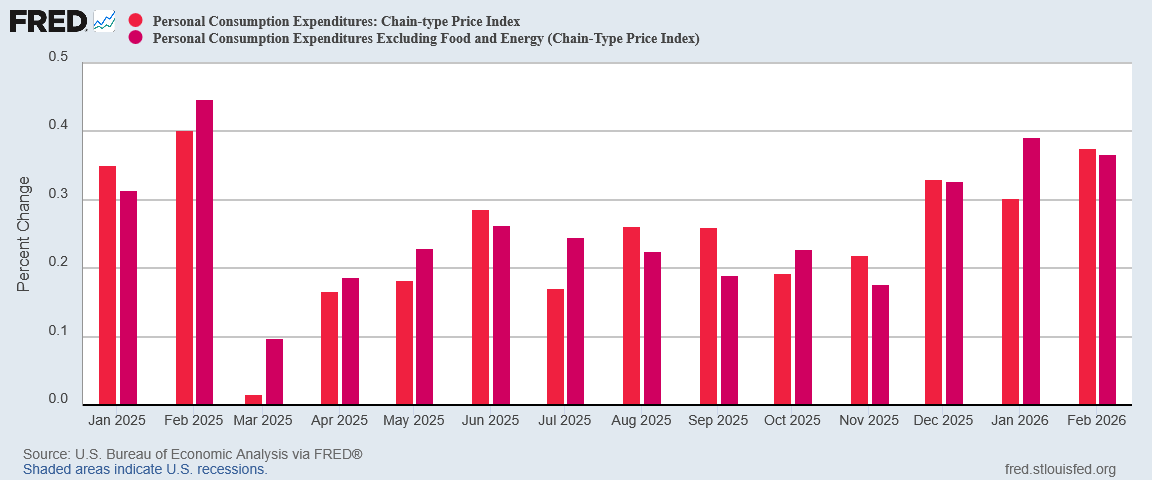

From the preceding month, the PCE price index for February increased 0.4 percent. Excluding food and energy, the PCE price index also increased 0.4 percent.

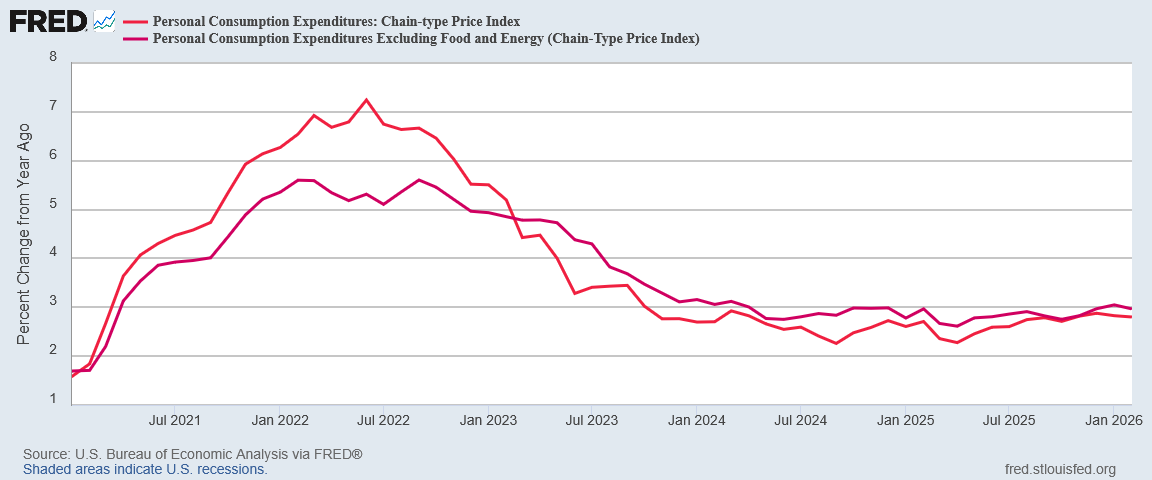

From the same month one year ago, the PCE price index for February increased 2.8 percent. Excluding food and energy, the PCE price index increased 3.0 percent from one year ago.

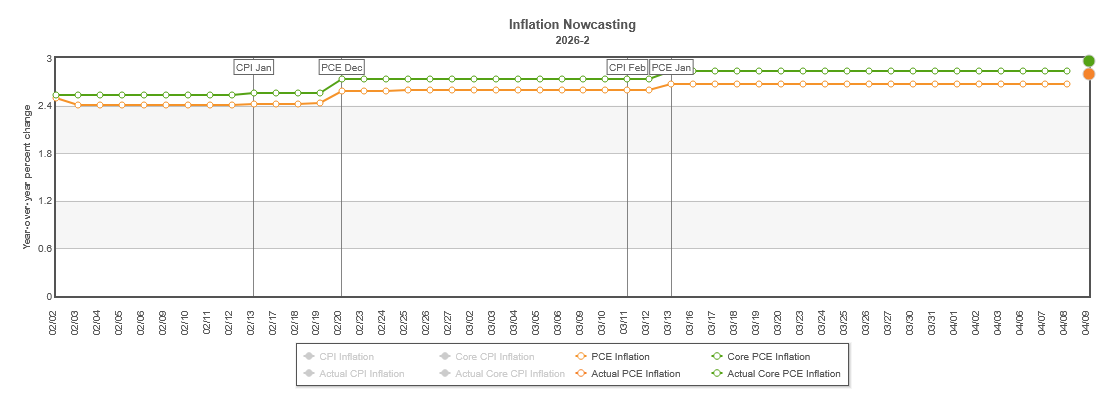

Year on year, the numbers aligned with Wall Street as well as Trading Economics almost perfectly.

While the numbers may have been in line with Wall Street’s expectations, the Cleveland Fed’s InflationNow nowcast was more noticeably off the mark, under-assessing inflation by 0.1pp year on year for the headline and core numbers.

Still, February’s inflation data on the surface presented no surprises whatsoever. On the surface, February’s inflation data was, like January, “more of the same.”

We should enjoy that. Next month will be a completely different situation. Whatever else we can see in the February PCE data, one thing is already clear: most if not all of the trends within will be ended by the war with Iran and the energy price shock it has delivered to the world.

Yet when we peel back the layers, we see that inflation was already ramping up even before the start of the war with Iran. Energy prices were up, and durable goods prices especially were up. Consumption was up. Disposable personal incomes were down.

Even before the first bombs fell in Operation Epic Fury, February’s inflation data were precursor and prelude to the inflation shocks coming in March and April.

Every article I publish takes time, care, and independence. A paid subscription fuels that work and shields it from outside pressure. If you’re able, join me today.

Headline Numbers Were Predictable…And Predicted

When the data meets expectations, finding a meaningful comment becomes a bit of a challenge. We talk about surprises. Normalcy invites little in the way of discussion.

On the surface, the PCE inflation data did meet expectations. Headline inflation remained the same, with the core data year on year printing a slight decline.

On the surface at least, things are not looking bad with respect to consumer price inflation, although if this were the whole story we would again have to wonder if the US economy was slipping into stagnation.

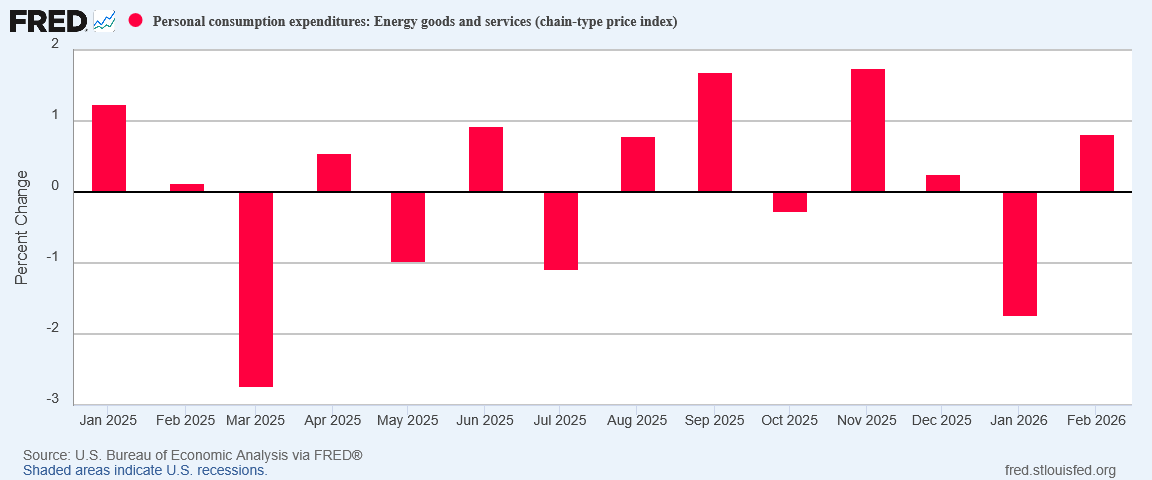

When market energy prices are rising across the board, there is little left to pull prices back down again.

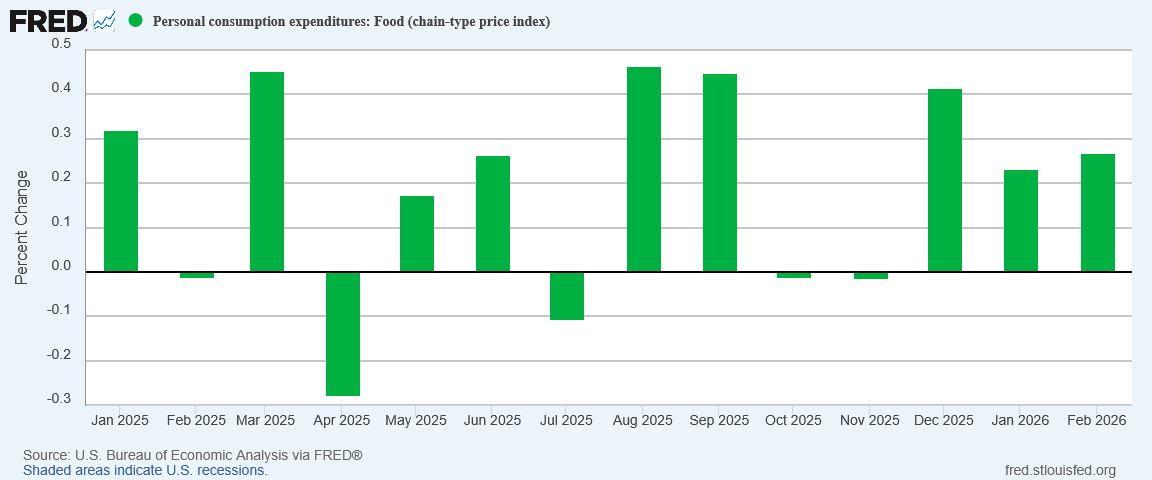

Food price inflation also heated up incrementally in February, rising from .23% to .25% month on month.

The combined impact of both rising energy price inflation and food price inflation for February was to hold the headline inflation metric constant even as the core metric ticked down.

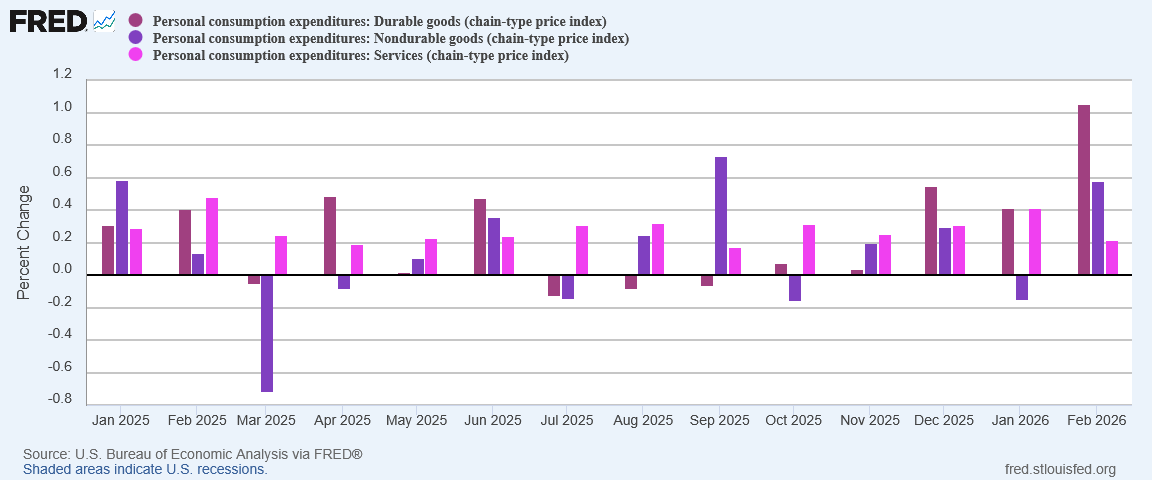

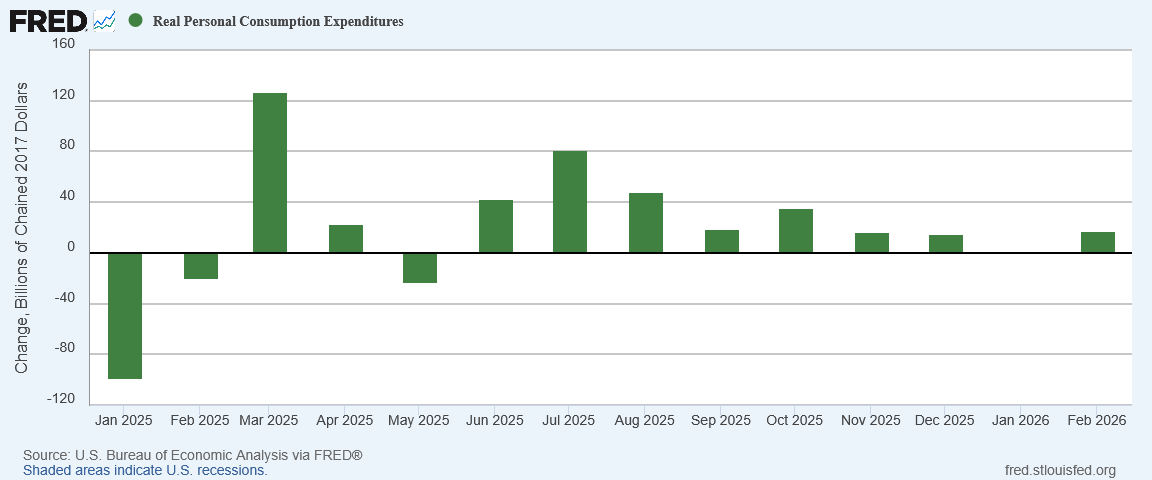

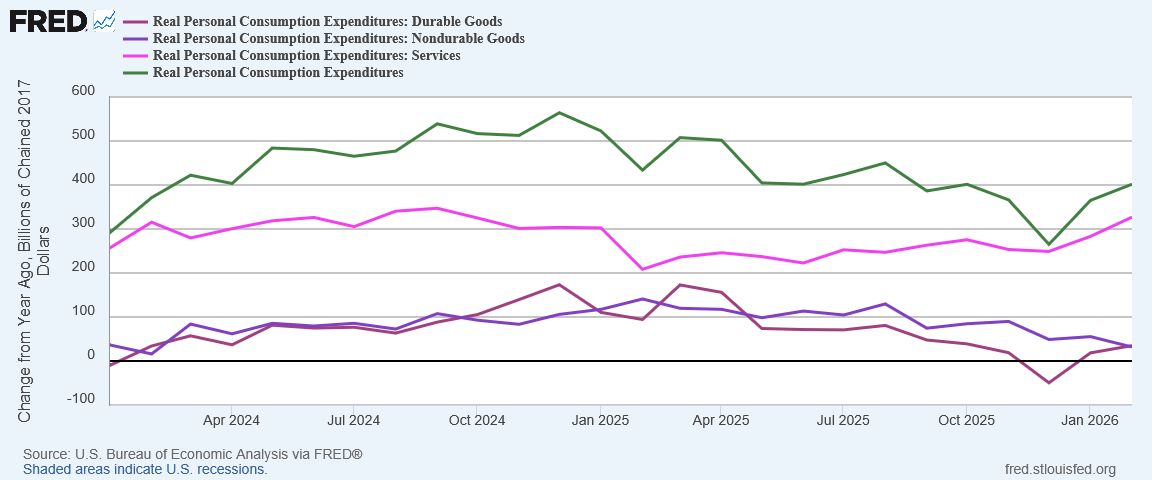

With a significant rise in durable goods consumption, we should not be surprised that the increased consumption resulted in bidding up durable goods prices. That consumption rose overall further reinforces this possibility.

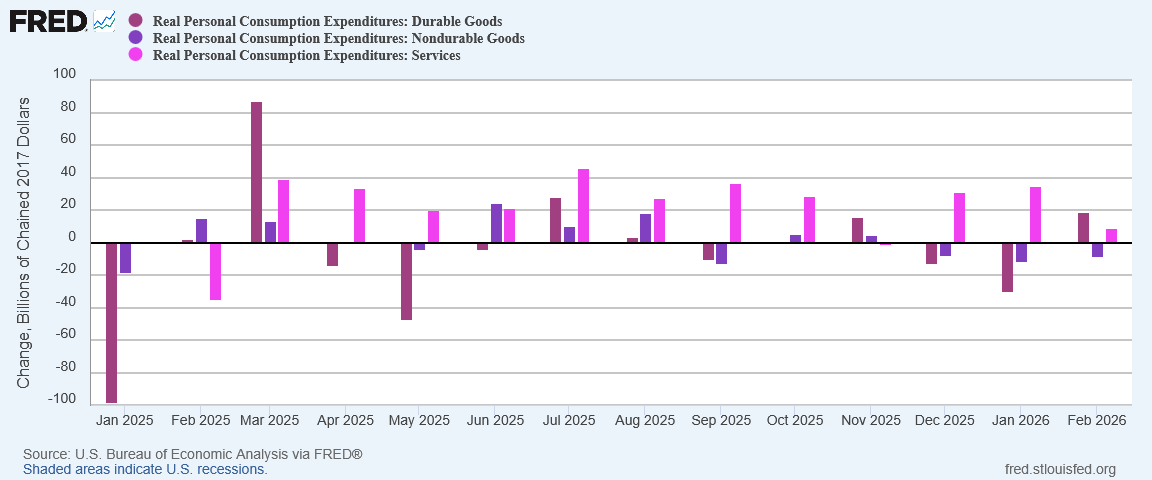

Rising consumption is broadly a good thing, as rising consumption largely translates into economic expansion and growth.

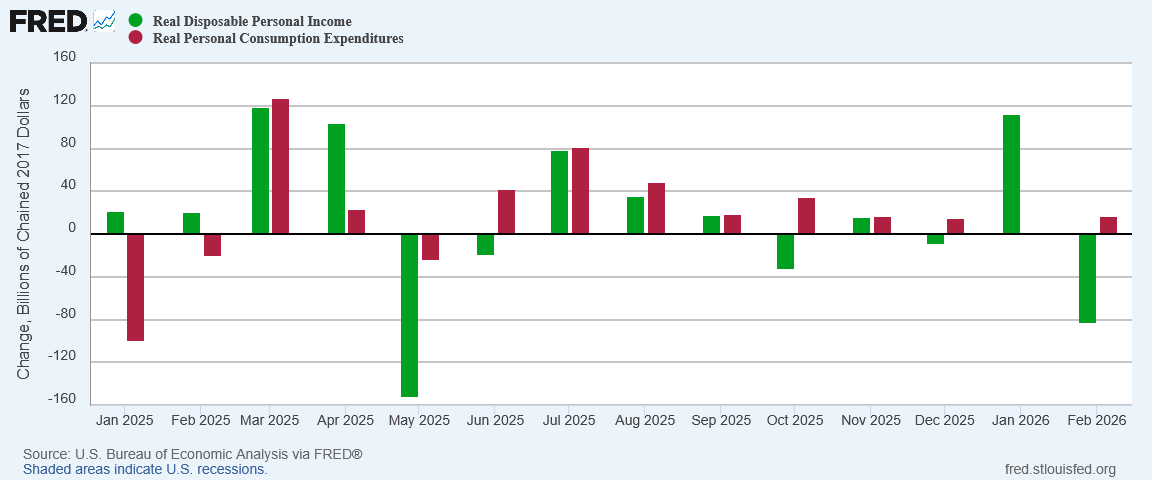

The income drop is disconcerting. Not only does it presage the decline in weekly paychecks reported on the March Employment Situation Summary, the decline was the second largest since Donald Trump took office.

One does not need to hold a PhD in economics to realize that declining disposable incomes will at some point put a constraint on how much consumption can increase. Potentially, this would explain why consumption peaked in late 2024 before trending down even before Donald Trump took office.

One reason stagflation hypotheses have lingered is because of declining metrics such as real consumption expenditures. When circumstances result in zero growth or very little growth for consumption, economic growth is simply not happening.

February saw signs that inflation was heating up in parts of the economy. The jump in durable goods especially was an indicator that inflation overall might be heating up even if just somewhat.

While the rise in consumption is, broadly speaking, a good sign, the drop in disposable personal incomes is not. The ongoing decline in disposable personal incomes is a distinctly worrisome trend. Lack of disposable personal income is a constraint on consumption, and it is distinctly possible that constraint has played a role in keeping inflation trending down in this country.

However, we know that March will not be the continuation of any such trend. Thanks to Operation Epic Fury and the war with Iran, we already know that March inflation will be significantly higher, and driven mainly by energy prices.

Wars are disruptive that way. We would anticipate that even without considering the impact of rising crude oil and diesel prices that we have seen throughout March. Even without consumption, even with a constraint on consumption from falling disposable personal income levels, the energy price shock from the war with Iran is going to reshape price levels and inflation across the whole of the economy.

We already know much of this because we have already seen some of the price shifts in real time.

While the stellar jobs numbers for March work against such a scenario for March, labor markets have been toxic and dysfunctional for long enough that any dramatic and sustained surge in prices starts to look an awful lot like the 1970s, when rising unemployment collided with rising consumer prices. Certainly February’s PCE data does little to dispel such concerns.

If the war with Iran continues to drag on, and especially if the recently and still quite fragile ceasefire fails to hold, we might see inflation and unemployment combinations that look distressingly stagflationary. The inflation data from both January and February leave that possibility very much on the table.

The key word in that assessment, of course, is “if”.

If the war with Iran reiterates anything for us it is to not get ahead of the data. We know the March Consumer Price Index data will show surges in headline, energy, and core inflation. We do not know if April will bring major corrections to the March jobs data, nor do we know how long the inflation surge will last. We will not be concerned with stagflation if the inflation metric goes up and then goes right back down in the subsequent month.

Will we get back to something like February’s data once the war with Iran is over? That we do not know, and cannot know.

If oil prices remain elevated for whatever reason, we will not be returning to February-like numbers on inflation and consumption even after the war with Iran is over.

If oil prices drop down to pre-war levels, a return to February-like numbers on inflation and consumption is not at all out of the question.

February was the end of several trends regarding inflation and economic growth. We can see looking back that it was a precursor and prelude to the inflationary price shocks coming on from the war with Iran.

March will bring a jump in consumer price inflation. March may bring significant shifts in both income and consumption. We do not know what April will look like at all.

The fog of war is extending into the economics of wartime.

If this story gave you real value, help me keep going. All Facts Matter is powered by readers who believe facts should stand on their own. Your subscription makes that possible.

The whole world is waiting to see how Trump responds. Who knows what you’ll be writing about at mere week from now?

Looking forward to it, Peter!