First Republic Becomes The Third Banking Domino To Fall

Bank Failure? Banking Regulation Failure? Or Banking Regulator Failure?

If the corporate media has the sense of things, the FDIC takeover of First Republic Bank has finally begun, with the banking regulator soliciting takeover bids for the troubled bank from its larger (and presumably healthier) rivals.

The Federal Deposit Insurance Corp. has asked banks including JPMorgan Chase & Co. and PNC Financial Services Group Inc. to submit final bids for First Republic Bank by Sunday after gauging initial interest earlier in the week, according to people with knowledge of the matter.

The regulator reached out to banks late Thursday seeking indications of interest, including a proposed price and an estimated cost to the agency’s deposit insurance fund. Based on those submissions Friday, the regulator invited at least two firms to the next step in the bidding process, the people said, asking not to be named discussing the confidential talks.

With the FDIC apparently hoping to secure a takeover—in effect, a “shotgun marriage” as was common during the Great Financial Crisis and subsequent recession of 2007-2009—before the markets open on Monday, First Republic Bank thus becomes the third banking domino to fall, as the banking crisis returns to Wall Street.

This moment has been an inevitability since First Republic shared its earnings numbers on April 28, ahead of its 10Q SEC filing. In an ironic replay of what triggered Silicon Valley Bank’s final demise, the admission by First Republic that some 41% of its uninsured deposits had fled the bank panicked investors and remaining depositors alike, leading to an inevitable share price collapse.

The press release confirmed that the banking industry’s bad news had returned with a vengeance.

It appears I was very much on target, as one of the star players in the March banking crisis, First Republic Bank, is once again taking up headlines with bad news (and red ink).

Their subsequent stock price performance proved it, shedding more than 80% of its remaining share price to close out Friday’s trading at $3.51, falling to $2.33 in after hours trading on Friday.

Despite the pace at which First Republic hemorrhaged share price after the Monday press release, the FDIC took no action throughout the week, even after a report (rumor?) that the bank was about to be placed in receivership by the banking regulator.

For an entire week, the FDIC simply left First Republic twisting in the wind.

The irony of the regulatory inaction is that, while First Republic Bank shares were getting monkeyhammered by Wall Street, the banking regulator released a post-mortem of its actions before, during, and after the SVB collapse, in which it concluded that it had not acted “forcefully” enough during the crisis.

The weekend of March 10, 2023, was unprecedented. The speed with which depositors withdrew funds from SBNY and SVB was unexpected and surprised the regulators and the banking industry. The coincidence of these two failures and their unprecedented speed may lead to changes in regulation and supervision and reevaluating liquidity risk management. The goal of bank supervision is to promote safety and soundness and financial stability, not to prevent bank failures. Maintaining safety and soundness requires effective challenge from the regulators and receptivity and responsiveness from the banks. In the case of SBNY, our internal review found that the bank could have been more measured in its growth, implemented appropriate risk management practices, and been more responsive to FDIC’s supervisory concerns, and the FDIC could have been more forward-looking and forceful in its supervision.

As of this writing, the FDIC appears to be soliciting takeover bids for the ailing bank and may very well have them before the markets open on Monday.

Yet we must not lose sight of the fact that, in most regards, First Republic’s banking operations were, while not extraordinarily profitable, were not themselves direct money-losers.

Yet a question still remains: with positive net income, positive net interest income, positive earnings per share, why are so many talking about First Republic as if it were on the brink of collapse? The bank is still making money, just not as much of it has before.

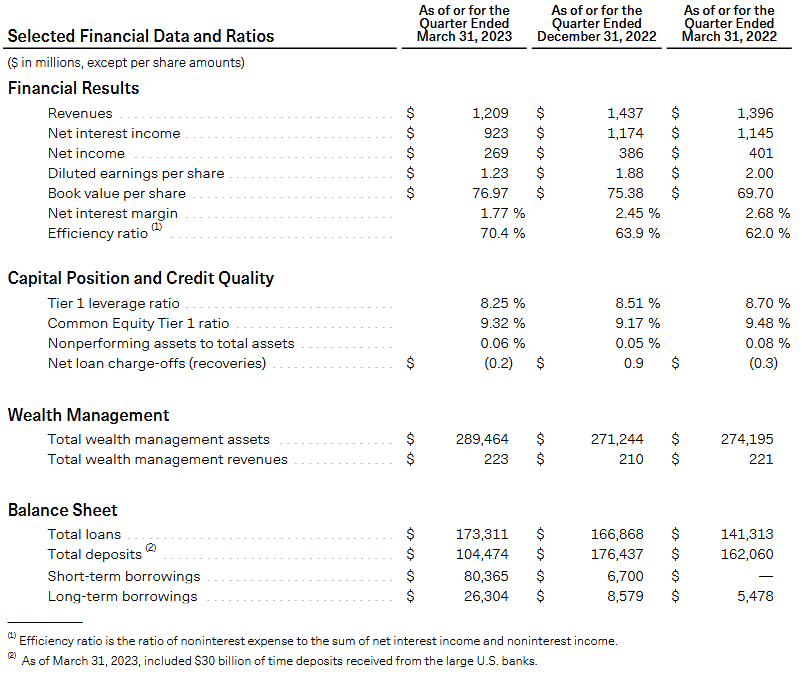

When we examine the numbers shared in the press release, we see that, while the numbers are far from being stellar, they are nevertheless largely devoid of red ink.

Revenues are roughly $200 million lower for the first quarter 2023 than a year ago, but book value per share is almost $7/share higher. Its Tier 1 and CET1 ratios are healthy, and it even managed to recover some of its previously charged-off loans. These are not numbers that speak to an imminent failure by the bank.

While there remains a lingering interest rate risk and vulnerability from its securities portfolios, that vulnerability was diminishing, as the market value of its held-to-maturity portfolio had been recovering throughout March.

With First Republic’s portfolios largely involving mortgage-backed securities, the market value outlook for those are actually positive year to date, based on related ETF valuation changes.

The most glaring weakness in First Republic’s released data is its balance sheet numbers.

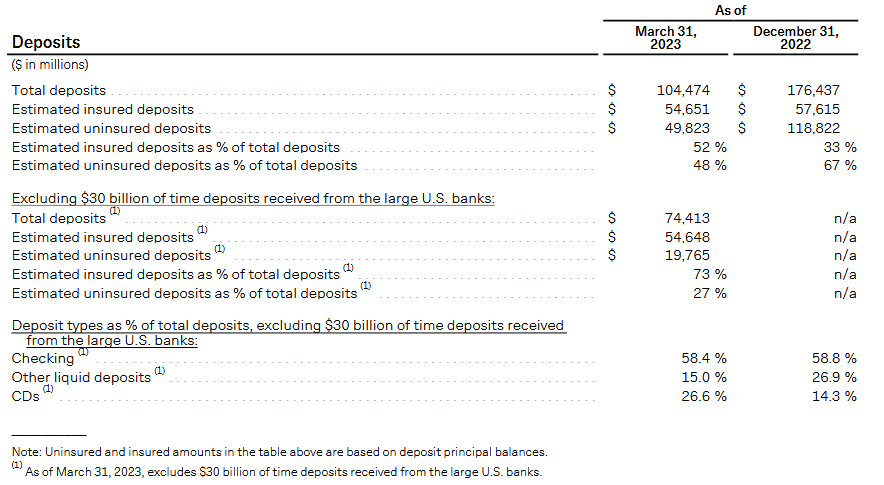

Borrowings had exploded during the first quarter and deposits had imploded, even as overall loan activity increased somewhat.

However, the deposit flight was chiefly among uninsured deposits—which is perhaps unsurprising, particularly after SVB’s collapse in March.

The bank’s borrowings largely reflect its efforts to secure sufficient liquidity to cover the deposit flight.

But for the deposit outflows, the borrowings for the first quarter of 2023 would have been largely the same as for the fourth quarter of 2022.

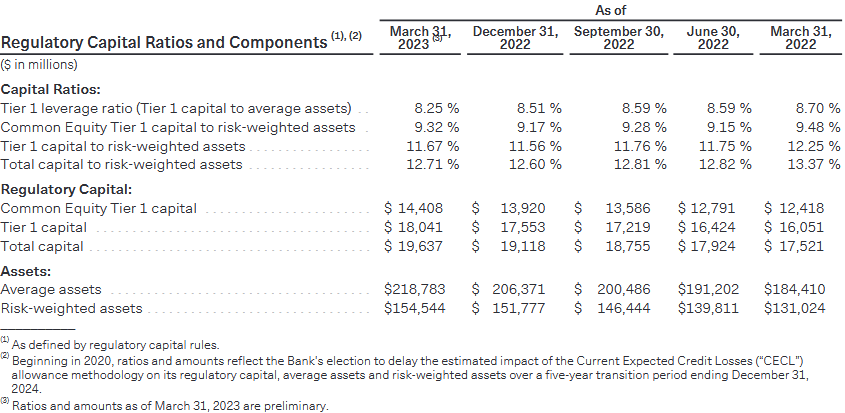

Even the regulatory capital ratios at First Republic have remained largely solid.

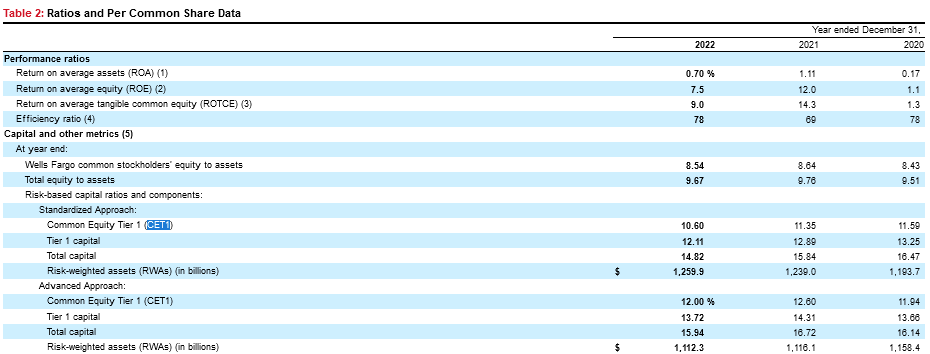

Absent a bank run scenario, these are not numbers which should give anyone heartburn. The ratios are very much in line with a presumably “stable” bank such as Wells Fargo, for example, as evidenced by Wells Fargo’s 2022 10K filing.

First Republic Bank is, by every normal measure, not an institution on the verge of bankruptcy.

Ultimately, the existential crisis for First Republic Bank is that it has been facing a bank run, with depositors pulling out deposits at an highly accelerated rate and forcing the bank to go to great lengths—and borrow heavily from the Federal Reserve—to cover the demand for cash presented by the deposit outflows.

Yet, as even the corporate media observed, every bank would be in trouble during a bank run.

Banks never have all the cash on hand to cover all deposits. They instead take in deposits and use the cash to make loans or investments, such as purchasing US Treasuries. So when customers lose confidence in a bank and rush to withdrawal their money, what is known as a “run on the bank,” it can cause even an otherwise profitable bank to fail.

Why is the bank run happening? Because interest rates have risen and are anticipated to keep rising. This shift in the financial environment is causing large banks in particular to lose deposits across the board.

Among domestic banks, the 25 largest banks—what the Federal Reserve terms “large domestically chartered commercial banks—had as of March 1 lost 5.5% of their January 2022 deposit balances. All other domestically chartered commercial banks held 0.5% more of their January 2022 deposit balances as of that same date.

The rise in interest rates is prompting bank depositors to move their money elsewhere, in many cases chasing better interest rates, but lately fleeing banks perceived to be “unstable”.

First Republic, just like Silicon Valley Bank before it, is a victim of this behavior. An otherwise viable bank is being squashed by what can only be described as depositor panic.

Let us be clear: the banks and only the banks are responsible for their being saddled with securities whose value can only decline so long as the Federal Reserve is in a mood to push interest rates higher. They’ve had more than a year to adapt their investment strategies to a rising interest rate environment and simply have not done so.

There are many reasons to criticize Powell for his rate hike strategy—the chief one being that it hasn’t worked, and that deliberately causing a recession is sucky economic policy on a good day coming in a close second. That Wall Street is now “broken” isn’t one of them. Wall Street has been tantruming for months over interest rates rather than doing a little adulting and resolving their balance sheets.

Yet let us also be clear that the banking regulators have also seen these trends of deposit outflow and unrealized losses among legacy securities. The irony of their now seeking greater regulatory authority is that they failed to make effective use of the regulatory authority they already have to resolve issues they saw months ago.

Unlike during the Great Financial Crisis, this is not a case of investments going bad because of rising defaults. This crisis is happening because low-yield securities are worth less than high-yield securities, all else being equal. This crisis is inevitable anytime there is a prolonged rise in interest rates, as there was during the summer of 2022.

Similarly, it was obvious at the time Dimon’s Eleven deposited $30 Billion in First Republic Bank that, absent a sea change in the interest rate outlook, the added deposits were a temporary lease on life and no more than that.

Is First Republic “out of the woods”? Probably not, although they likely have at least 120 days’ grace to work out a more permanent solution—which at this juncture very likely entails a sale to one of the bailout partners. However, given that First Republic has not held a fire-sale on their debt securities portfolios, it seems reasonable to infer that First Republic was not yet at the SVB position of having to desperately raise cash by any means necessary. In time, First Republic could come to that same SVB position of desperation, which would necessitate a shuttering and fire-sale auction of either the entire bank or its assets piecemeal, but it is not there yet.

By the FDIC’s own admission, they did not, during this time period, sit down with banks large and small and hammer out an approach to confronting deposit outflows. They saw the train wreck unfolding in slow motion and did nothing to help stop it.

Even though First Republic, much like Silicon Valley Bank before it, is a failure of bank management, First Republic, like Silicon Valley Bank before it, is also a failure not of banking regulation but banking regulators. If bank regulators are going to take over critical thinking for bank officers they need to deliver on that commitment. They need to spot the danger zones far in advance and work with banks to navigate the problems. This they did not do—this they have admitted they did not do.

First Republic Bank is the latest banking domino to be knocked over by bank regulators and the Federal Reserve. First Republic Bank will not be the last such banking domino. The Federal Reserve and the FDIC’s regulators are sure to see to that.

Every day when I read the headlines in the Wall Street Journal I find myself thinking, ‘yep, Peter Nayland Kust is right again!’ What still mystifies me is how so many MBA Finance grads could mess up so many common-sense banking fundamentals. So, my next question: do you think this latest bank failure will placate everyone into thinking the banking crisis is over, or do you think it will spark the nervous herd into a stampede to get their deposits out of Dodge?

The kind of people who gravitate toward becoming regulators are good at crunching numbers but lack the knack for "pulling the trigger." That's why more regulations and regulators is the wrong way for taxpayers to be forced to go.