The other day I speculated that a new banking crisis was potentially about to unfold.

Adding to the financial stress are the mounting unrealized losses on banks’ securities portfolios. As yields rise, banks’ legacy investments in low-yield securities lose market value, reducing the capacity of those investments to be sold to cover deposit demands as people continue to pull their cash out of the banking system. When we look at the market value of various Exchange Traded Funds dealing in debt securities, we can immediately see the valuations are heading south again. Unless market sentiment has shifted, things are approaching the same meltdown threshold that was reached in early March. That means a fresh banking crisis is potentially just days away.

It appears I was very much on target, as one of the star players in the March banking crisis, First Republic Bank, is once again taking up headlines with bad news (and red ink).

Troubled regional bank First Republic said Monday that its deposits fell 40.8% to $104.5 billion in the first quarter, which saw the collapse of two other mid-sized banks and sparked fear from customers about widespread bank failures.

The deposit flight at First Republic was worse than Wall Street expected, with analysts estimating the figure at the end of the first quarter to be about $145 billion, according to the consensus estimate from FactSet’s StreetAccount. Analysts’ deposit estimates ranged from $100 billion to $206 billion, according to FactSet.

Somewhat unsurprisingly, Wall Street reacted to this bit of bad news—released after the close of Monday’s trading—by eviscerating First Republic’s stock as soon as trading opened on Tuesday.

Prior to Monday’s press release, First Republic’s stock had largely stabilized, although at a share price that was a fraction of its previous levels.

One thing should be noted, however: Wall Street’s reaction is almost certainly premature and panicked, because the press release only announced a few key earnings items. It was not the bank’s full quarterly 10-Q statement, which is not likely to be released until sometime next week or the week after (going by the timing of previous 10Q statements).

It is not hard to determine what triggered Wall Street’s reaction: the bank’s earnings have plummeted, as have their deposits.

When earnings per share drops by more than a third, Wall Street investors are not going to react kindly.

Yet a question still remains: with positive net income, positive net interest income, positive earnings per share, why are so many talking about First Republic as if it were on the brink of collapse? The bank is still making money, just not as much of it has before.

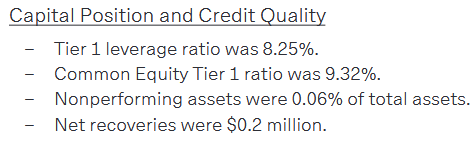

Even the bank’s capital ratios are, relative to industry norms, healthy.

The Common Equity Tier 1 ratio (CET1) is double what the Fed mandates for large banks. That should be a depiction of financial health, not financial weakness. Non-performing assets is significantly below the national averages.

While First Republic’s revenue numbers are poor, how does this translate into imminent insolvency?

First Republic’s problem today is the same as it was in March: deposit flight and declining market values of its securities portfolios. While the bank is still profitable, the banking environment has still produced dramatic deposit flight, and the need to cover those exiting deposits is straining the bank’s liquidity.

I examined the details of First Republic’s balance sheet as of their 2022 10-K (still the most recent available presentation as of this writing) in my earlier article discussing Dimon’s Eleven and their $30 Billion lifeline to First Republic, which did little more than buy the bank a small grace period to figure out how to fix things on a more permanent basis.

Is First Republic “out of the woods”? Probably not, although they likely have at least 120 days’ grace to work out a more permanent solution—which at this juncture very likely entails a sale to one of the bailout partners. However, given that First Republic has not held a fire-sale on their debt securities portfolios, it seems reasonable to infer that First Republic was not yet at the SVB position of having to desperately raise cash by any means necessary. In time, First Republic could come to that same SVB position of desperation, which would necessitate a shuttering and fire-sale auction of either the entire bank or its assets piecemeal, but it is not there yet.

While it has not been even 60 days since the lifeline was thrown to First Republic, it appears the bank is rapidly running out of time to resolve its liquidity issues, and may even be out of time, with the FDIC starting to breathe heavily on the bank’s neck.

US bank regulators are weighing the prospect of downgrading their private assessments of First Republic Bank — a move that may curb the troubled firm’s access to Federal Reserve lending facilities.

The Federal Deposit Insurance Corp. has been giving the bank time to reach a private deal to shore up its finances. But as weeks keep passing without a transaction, senior officials are increasingly weighing whether to downgrade their scoring of the firm’s condition, including its so-called Camels rating, according to people with direct knowledge of the talks. That would likely limit the bank’s use of the Fed’s discount window and an emergency facility launched last month, the people said.

If bank regulators are aware of the irony in cutting First Republic off from the very liquidity facilities created for their precise situation, that has not been evident in the reporting.

This has set up a game of “financial chicken” between Wall Street and the FDIC, with Wall Street waiting for the FDIC to step in with a bailout and the FDIC waiting for Wall Street to rescue First Republic without a bailout. Reading between the lines, it may even be that the FDIC’s contemplated downgrade of First Republic is a pressure tactic intended to force Wall Street to act—although cutting First Republic off from the Fed’s liquidity resources might also precipitate the collapse and bailout they are trying to avoid.

The clock for striking such a deal began ticking louder late last week. US regulators reached out to some industry leaders, encouraging them to make a renewed push to find a private solution to shore up First Republic’s balance sheet, according to people with knowledge of the discussions.

Lost in the Kabuki theatrics swirling around First Republic is the reality that, in virtually all technical respects, First Republic is still a sound bank. Their loan book is solid even if low yielding. But for the issue of deposit flight, there would be no questions of solvency for the bank.

In the eyes of some Wall Street analysts, First Republic’s greatest weakness is the quality of their depositors. Even back during the initial March crisis, this was a prevailing sentiment on Wall Street.

The reason has a lot to do with the high-net-worth people who bank there.

“It’s the biggest example of a bank that could go down and shouldn’t go down — a first-class bank,” said a source close to the 48-hour deal to infuse First Republic with $30 billion in cash.

It turns out that there is a particular risk involving high-net-worth clients: they can be skittish about their money.

“These depositors are particularly trigger-prone,” said Patricia McCoy, a law professor at Boston College. “They’re sophisticated, they know they have other options, and they have mechanisms in place to move money quickly.”

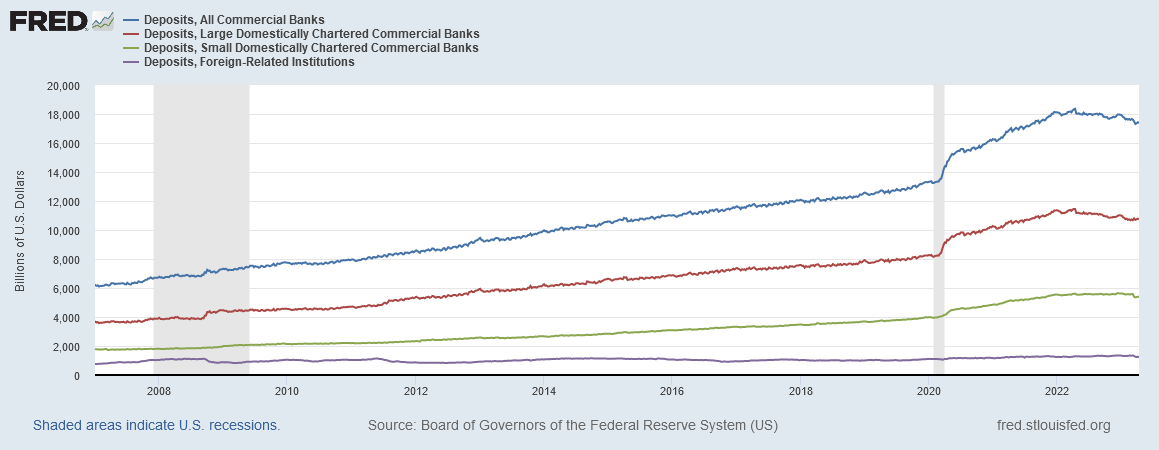

However, putting the onus of deposit flight on wealthy depositors conveniently ignores why the deposits are fleeing First Republic—deposits are flowing out of First Republic because deposits are flowing out of the banking system as a whole, and have been since the Federal Reserve began its campaign to push up interest rates.

Total deposits in the banking system peaked in April, 2022, at $18.4 Trillion dollars, and by April of this year had dropped by over $980 Billion.

Nearly one trillion of deposits have left the banking system in the past 12 months, with $700 Billion of that in the large banks alone.

Nor is there any mystery why deposits have been flowing out of the banking system: rising interest rates have made bank deposits a less attractive place to store idle cash. While interest rates began rising before the Fed started hiking the federal funds rate, their rate-hike campaign has not been kind to banks’ liquidity.

Large banks in particular (and this would include First Republic) have felt the greatest deposit loss.

Concurrent with this decline in deposits, the Fed has been shrinking the money supply, with both the M1 and M2 money supply metrics dropping significantly from April 18, 2022 onwards.

If we index both metrics to April 18, 2022, we see that in the twelve months since the M1 has dropped over 10% and the M2 has dropped over 5%—and the pace of reductions in the M1 appears to be increasing.

Note that these declines began shortly after the first federal funds rate hike.

There is no great surprise that the money supply should shrink chiefly by seeing deposit flight—bank deposits remain an essential element of the money supply, and so the two rise and fall necessarily in tandem.

First Republic is losing deposits because the Fed is draining them away.

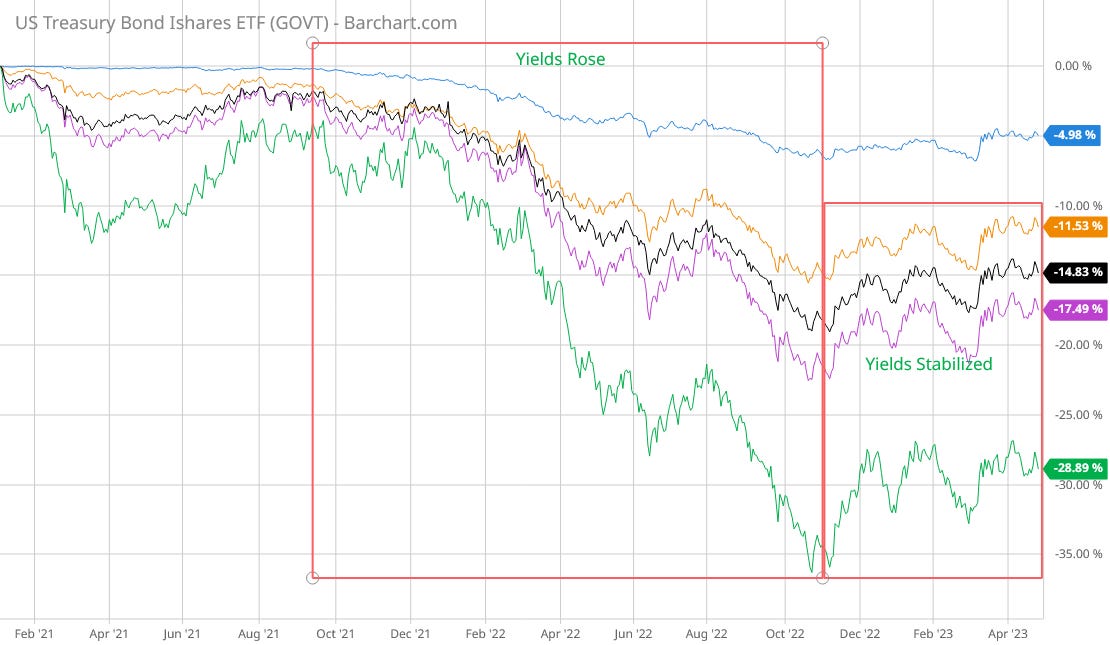

At the same time, pushing interest rates up has impaired the value of First Republic’s securities portfolios.

Tracking various Exchange Traded Funds focused on US Treasuries, the market value of these funds—and the market value of the underlying securities issuances by extension—have dropped nearly 15% overall, and nearly 30% for 10- and 20- Year Treasuries over the past two years with the bulk of the decline coinciding with the period of interest rate increases.

These funds began to recover some of their market value as interest rates stabilized last November.

We see a similar pattern with corporate bond ETFs as well—value loss as interest rates rose, and value recovery after interest rates stabilized last November.

Again, there is no mystery here. Higher yields on more recent assets make the lower yields of legacy assets less valuable.

Yet it is this loss of market value that is undoing the bankers’ calculus. Notionally, these interest bearing securities are “safe” investments, as the chances of default are fairly low. Unfortunately for banks, bond issuers can only be a factor in default risk. Interest rate risk—the potential for loss of market value due to rising rates—is entirely a product of market interest rates and the various factors that influence them.

First Republic kept its low yield assets on the books even as interest rates rose, bleeding away the market value of those assets. At the same time, rising interest rates began pulling deposits away from banks including First Republic. Thus a liquidity crisis was born, where First Republic eventually must run out of cash to satisfy deposit outflows because the remaining market value of its assets is not enough to cover the remaining deposits—and its depositors know this.

Deposit flight, monetary supply reduction, and market value decline of fixed-income securities are all inevitable outcomes in a period of rising interest rates. These not merely things that can happen, but things that absolutely will happen.

Deposit flight, monetary supply reduction, and market value decline of fixed-income securities are all what the Fed’s campaign to hike interest rates were bound to produce. The Fed’s strategy was always going to carry these negative consequences, and yet these risks have been completely dismissed and ignored by both the Federal Reserve and by Wall Street.

At First Republic, this bleeding away of both the market value of their assets and the amount of their liabilities is producing the equally inevitable result of First Republic not having the money needed to satisfy depositor demands.

First Republic is suffering because its leadership failed to address the changing interest rate environment early on, when the solution was manageable. Yet First Republic did not cause the changing interest rate environment, and in that regard, the bank is hemorrhaging because Jerome Powell has pushed them to the brink.

Previously I asked how much farther Jay Powell could push the banking system before something breaks.

Wall Street is providing the answer: no farther. The breaking has already begun.

How often do you say predictably or inevitable or WILL happen.

Kinda like my supply of canned soup - I eat oldest first and when I replenish it goes to back of my inventory - it rotates.

Like a store.

Like its my core business.

Where was the monetary uptick or benefit to these banks to NOT rotate stock as any other entity does w their core assets? Besides laziness or incompetent staff/leadership there has to be sizeable upside for them to ignore the

Inevitable

Certainties

On the horizon that all knew was occurring.

What is missing from equation - does it make sense they were just caught napping?