Is Beijing Behind Zhongzhi's Insolvency?

Unintended Consequences of China's Liquidity Policies

Financial fears of contagion returned to China last week, as "shadow bank” Zhongzhi Enterprise Group was finally forced to acknowledge insolvency.

Zhongzhi Enterprise Group, one of mainland China’s largest shadow banks, has warned investors that it is unable to repay its debts, setting off alarm bells in the trust sector which invests a large portion of investors’ money in real estate projects.

The Beijing-based wealth management company said late on Wednesday its total liabilities had mounted to between 420 billion yuan (US$59 billion) and 460 billion yuan, while its total tangible assets stood at just 200 billion yuan, implying a shortfall of as much as 260 billion yuan.

Readers may recall that Zhongzhi first came to notice in August, when a Zhongzhi subsidiary, Zhongrong International Trust, missed multiple payments on trust products.

Anxious Chinese retail investors are bombarding listed companies with questions about their exposure to Zhongrong International Trust Co after missed payments by the trust company triggered fears of contagion across the country's financial system.

Investors had submitted more than 100 questions to dozens of Shanghai- and Shenzhen-listed companies via investor relation platforms asking whether they had bought Zhongrong's products, after two listed firms disclosed late on Friday that they had not received payment on maturing trust products from Zhongrong.

Last week the contagion fears from August seem to have been confirmed.

Yet a question arises from the timing of Zhongzhi’s insolvency declaration: why now? What has happened to push the private wealth management company (i.e., “shadow bank”) into bankruptcy?

As it turns out, the answer to that question may very well be “Beijing’s liquidity injections and debt stimulus programs.”

Unsurprisingly, the initial contagion fears emerged from property developer Country Garden’s inexorable death spiral into debt default, with Zhongrong’s missed payments being preceded by missed interest payments by Country Garden.

Given the long-standing preference by purveyors of various trust and wealth management products for real estate investments, this synchronicity is only to be expected.

Defaults by Zhongzhi surfaced in sync with the mainland’s intensifying property crisis which involved mainland China’s biggest developers such as China Evergrande Group and Country Garden Holdings, as real-estate sales dived and cash flows dried up. Many trust products had invested heavily in real estate projects.

“We expect private trust companies to continue struggle, with more possible failures, but state-owned trust companies we believe will receiving more funding from their parent financial institution to prevent the loss of retail client investments and confidence,” Everbright Securities International said in a research note on Thursday.

Indeed, contagion from China’s collapsing property sector has been regarded by many as a near certainty, so much so that it is perhaps remarkable that Zhongzhi held out this long after Country Garden’s final tumble into debt default last month.

Yet it should also be noted that Beijing has been steadily ramping up support for China’s ailing property sector, including new policies encouraging banks to extend more loans to Country Garden and other distressed developers.

Beijing has stepped up efforts to solve China’s property crisis, calling on formal banks to increase their support for 50 large developers including Country Garden, the country’s largest real estate company, which defaulted for the first time last month. Country Garden’s share price rallied after Beijing’s intervention, which was reported by Bloomberg on Wednesday but has yet to be announced officially.

While as of this writing the policy has yet to be officially announced, the emergence of a draft list of developers eligible for additional bank support represents the latest incremental effort by Beijing to rescue ailing real estate markets.

As part of a package of new measures to backstop the real estate industry, regulators are considering allowing banks to issue so-called working capital loans to some developers, the people said, asking not to be identified discussing a private matter. Unlike other types of loans available to builders that typically require land or assets as collateral, the new financing facility would be unsecured and available for day-to-day operational purposes, potentially freeing up capital for debt repayment, the people said.

Officials are also weighing a mechanism that would allow one lender to take the lead on supporting a specific distressed builder by coordinating with other creditors on financing plans, the people said.

Perversely, the mode of support for distressed developers may very well have played a role in Zhongzhi’s final fall from grace.

To understand how this might be the case, we have to take a brief look at a recent transitory liquidity crunch in China.

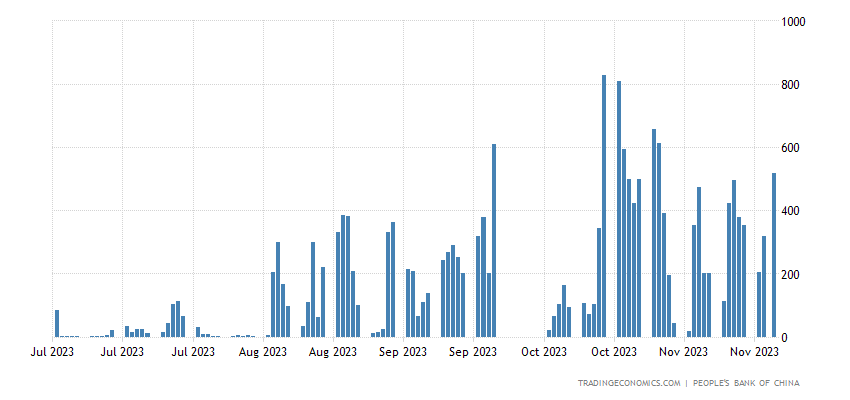

At the beginning of November, China’s money markets literally ran out of cash, and Beijing was the ironic likely reason why.

A brief cash squeeze rattled China’s money markets earlier this week, illustrating how the nation’s tightly-managed financial system is under strain from the government’s deluge of debt sales.

Interest rates on an overnight interbank loan soared to as high as 50% in isolated transactions for non-bank institutions on Tuesday, worsening a usually mild month-end funding crunch. A confluence of factors, from capital requirements for banks to tax payments and large government bond sales, were behind the surge in demand.

The surge in interest rates for non-bank borrowing occurred at least in part because Beijing has recently authorized a surge of new debt issuance both by the central government and by local governments and their financing vehicles.

Money market rates climbed in late October as banks came under pressure to meet regulatory requirements, companies faced tax payments and China’s central and local governments sold a record amount of bonds. A bank trader said at that time that cash demand was too high for large banks, the main providers of funding, to satisfy.

Put simply, Beijing’s newly authorized government debt issuances threatened to crowd out non-bank institutions, effectively stranding them without access to liquidity at the very moment Beijing was injecting a significant amount of liquidity into their finanaicl system.

“As bank balance sheets get clogged up with all this government bond issuance, leveraged, non-bank investment companies will likely continue getting squeezed,” Adam Wolfe, an economist at Absolute Strategy Research, wrote in a note. “So we continue to expect more liquidity support from the PBOC, including a cut to banks’ required reserve ratio.”

In other words, central and local government debt is depriving non-bank institutions of important access to fresh liquidity at the precise moment that liquidity is most needed to cover the growing shortfalls from their now significantly underperforming real estate investments.

That Beijing notionally takes liquidity issues seriously is easily demonstrated by the record level of liquidity injected into the financial system by the People’s Bank of China—a record 1.45 trillion for the month of November alone.

Even in the daily reverse repo markets, Beijing has been injecting a rising amount of liquidity over the past week.

Yet so great has been the central government’s own recent borrowing spree that it consumed all available liquidity and then some, thus producing record interbank interest rates and a true if temporary liquidity crisis—which according to some reports impacted the shadow banking industry most of all.

State broadcaster China Central Television blamed unidentified financial institutions for disrupting the market Tuesday. “Some institutions, with the aim of maximizing profits, depend too much on rolling-over financing, borrowing short and investing long — creating their own liquidity risks, which disturbs the market and creates a tense mood,” CCTV said in a report.

The jump in overnight borrowing costs Tuesday was seen mostly in over-the-counter borrowing by non-banks, traders said, asking not to be identified as they aren’t authorized to speak publicly. Those loans aren’t captured in public data.

Even the timing of Beijing’s latest debt issuances suggests they play a role in Zhongzhi’s latest solvency crisis, as the central government is turning more and more to traditional stimulus to reinvigorate an increasingly moribund economy.

In October, China unveiled a plan to issue 1 trillion yuan ($139 billion) in sovereign bonds by the end of the year, raising the 2023 budget deficit target to 3.8% of gross domestic product (GDP) from the original 3%.

Chinese leaders have pledged to "optimize the structure of central and local government debt", suggesting the central government has room to spend more as its debt as a share of GDP is just 21%, far lower than 76% for local governments.

Apparently, in the process of “optimizing” central government borrowing, Beijing overlooked non-bank actors such as Zhongzhi, and their own need for liquidity access.

Fans of government regulation are convinced that the real problem for China has been a lack of strong regulatory oversight of the shadow banking industry, decrying its predilections for “excessive leverage”.

By the end of 2021, Zhongzhi’s cash pools, not including that of its trust affiliate Zhongrong, had reached 300 billion yuan. They were backed by about 150 billion yuan worth of underlying assets, reported financial media outlet Caixin. No surprise then that, when new fundraising dried up, Nacity’s money was not returned at maturity.

The government, of course, frowns upon this practice. A polite description is excessive leverage, while a more crude one is a Ponzi scheme. However, because of their complex nature, regulations covering cash pool products have only been loosely enforced, according to CreditSights. Officials don’t get to see the lending documents — they are, by definition, private. They don’t have the resources to sift through and understand the tailor-made borrowing terms either.

However, this perspective overlooks the obvious market saturation effect when 1 Trillion yuan of new central and local government debt is in the process of being dumped on financial markets. With or without regulatory oversight, there is only so much appetite for debt. As shadow banks as a rule do not deal in government debt, they are invariably pushed to the back of the line, and the fundraising and borrowing efforts which keep many trust products viable suffer the consequences.

There is even some indication that Beijing recognizes the dilemma the structure of these latest debt stimulus proposals presents. While the liquidity issues presented by imbalances in various borrowings are ultimately transitory, they are also anticipated to be a recurring theme through at least the end of the year.

Liquidity is expected to tighten after Beijing said last week it’s raising the fiscal deficit ratio and authorizing the sale of 1 trillion yuan of debt in the remaining months of the year.

“The PBOC may not target to address brief liquidity tightness among some market participants,” said Frances Cheung, a rates strategist at Oversea-Chinese Banking Corp. “Rather, we expect liquidity injection to buffer the broader liquidity demand arising from bond issuances.”

The issue the PBOC is simply choosing to overlook is the piecemeal imbalance among borrowing entities brought on by the surge of new debt issued by both the central government and various local governments.

The cautionary lesson to be learned is that even in tightly controlled centrally planned economies such as China, there is no escaping the consequences of government policy.

While Beijing can opt to issue however much debt it wishes, it cannot expand the overall market for debt issuances. The more the government borrows, the less credit is available for private borrowers, the higher the cost of that credit to private borrowers, and the more likely it is that private borrowers will be caught short as they are unable to utilize previously viable fundraising policies and practices.

Ironically, with Beijing on the verge of instructing the formal banking sector to extend even more credit to distressed developers, such a policy has the potential to exacerbate the funding imbalances which have caught out Zhongzhi, leaving them structurally insolvent, as the more the formal banks lend to developers, the less they will be able to lend to shadow bank players needing to avoid a funding crunch.

Country Garden’s debt and solvency woes may very well have been the catalyst for Zhongzhi’s own spiral into insolvency, but Beijing’s response to Country Garden has very likely helped that insolvency along. If this is in fact the case, then just as Country Garden is but the latest developer to fall from grace, Zhongzhi will only be the first of several shadow banks to grapple first with liquidity pressures and then ultimately insolvency.

Beijing may very well be on the verge of jumping out of the real estate frying pan into the shadow banking fire. Every debt solution it tries to solve one economic dilemma is likely to cause or exacerbate other problems.

The end result is likely to be an ongoing serial set of financial crises where the solution for each crisis succeeds only in magnifying subsequent ones.

And Xi expects Xiden to bail him out, $980 Billion worth?

This is madness.