JOLTS Shows Job Markets Are Not OK. The Fed Pretends They Are

Powell Likely To Ignore the Jobs Crisis Again

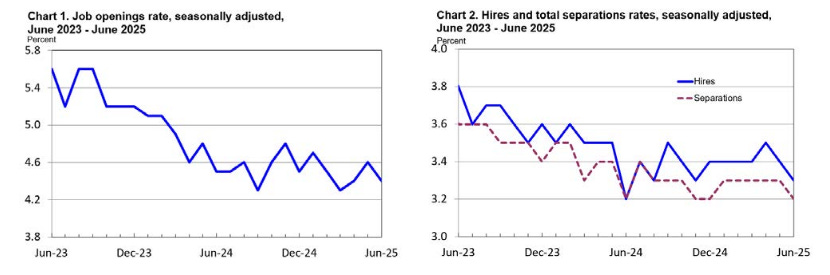

To apprehend the significance of the Bureau of Labor Statistics’ June Job Openings and Labor Turnover Summary report, do not read the words first. Study the charts.

Quite obviously, the charts show two important things:

Job openings, hires, and total separations all declined in June.

Job openings, hires, and total separations have been broadly declining for the past two years.

Why these points matter is made immediately apparent when you read the lead paragraphs of the summary report itself (emphasis mine):

The number of job openings was little changed at 7.4 million in June, the U.S. Bureau of Labor Statistics reported today. Over the month, both hires and total separations were little changed at 5.2 million and 5.1 million, respectively. Within separations, quits (3.1 million) were little changed while layoffs and discharges (1.6 million) were unchanged.

This release includes estimates of the number and rate of job openings, hires, and separations for the total nonfarm sector, by industry, and by establishment size class. Job openings include all positions that are open on the last business day of the month. Hires and separations include all changes to the payroll during the entire month.

Does “little changed” indicate either short-term or long-term decline? No. Not in any variant of either American English or the King’s English does “little changed” signify decline.

When you read the summary paragraphs describing the changes in job openings, hires, and total separations, nowhere is an aggregate decline on the month mentioned, nor a downward trend over the past two years.

Declining job openings, declining hires, and declining separations are the data reality the June JOLTS report, but you would not know it reading the reports introduction.

When we unpack the numbers within the report, the narrative does not improve.

June was an ugly month for hiring, according to the JOLTS report.

Worse yet, with Jay Powell about to announce the Fed’s latest interest rate decision, the Fed is likely to ensure June will be only the latest of a series of ugly months for hiring.

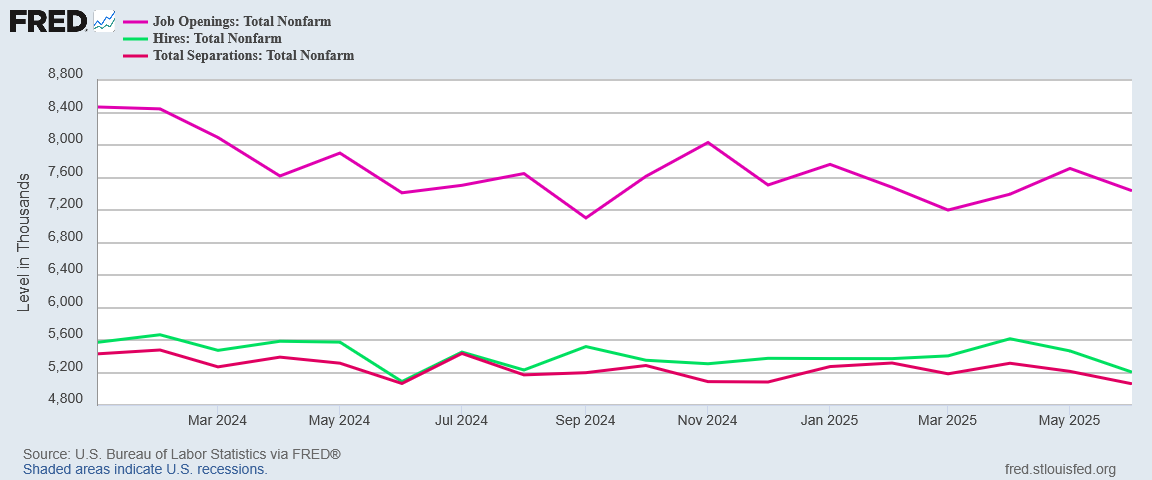

What the JOLTS report goes to some lengths to conceal is that aggregate job openings declined 275,000 in June, with non-farm hiring declining 261,000 and total separations falling 153,000.

These declines are what the BLS counts as “little change”.

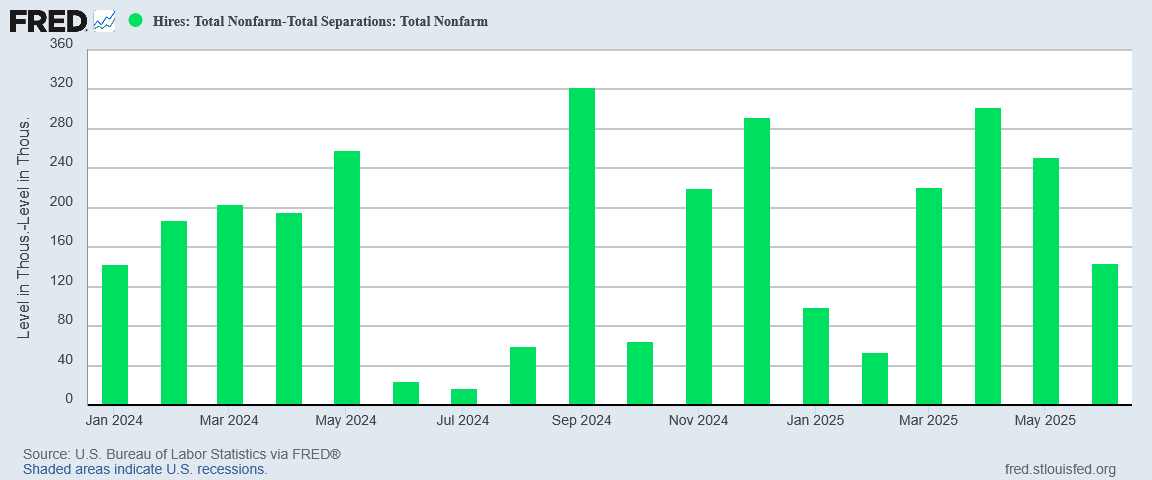

Those are not encouraging numbers, and they do not make for an encouraging graph.

Unsurprisingly, those numbers mean that net hiring slowed by almost half—from 252,000 to 144,000.

That is what the BLS counts as “little change”.

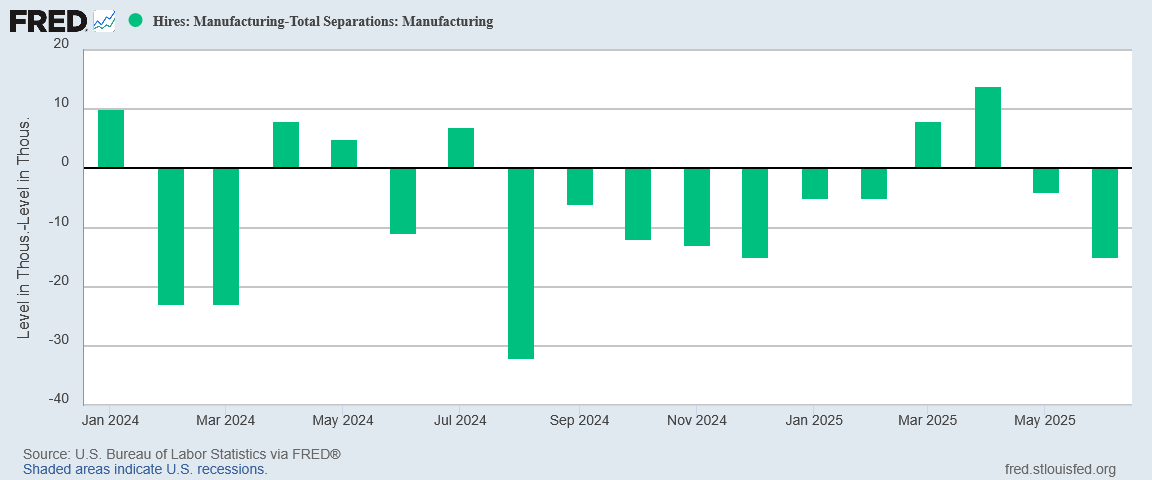

Net hiring in manufacturing went even more negative in June.

Manufacturing is one economic area in which Donald Trump pledged dramatic growth as part of Agenda 47.

If we are losing manufacturing jobs this is not a pledge that can be realized. Since January 2024 the prevailing trend in the US has been net loss of manufacturing jobs, per the JOLTS data. That same data shows President Trump has had only marginal success reversing that trend.

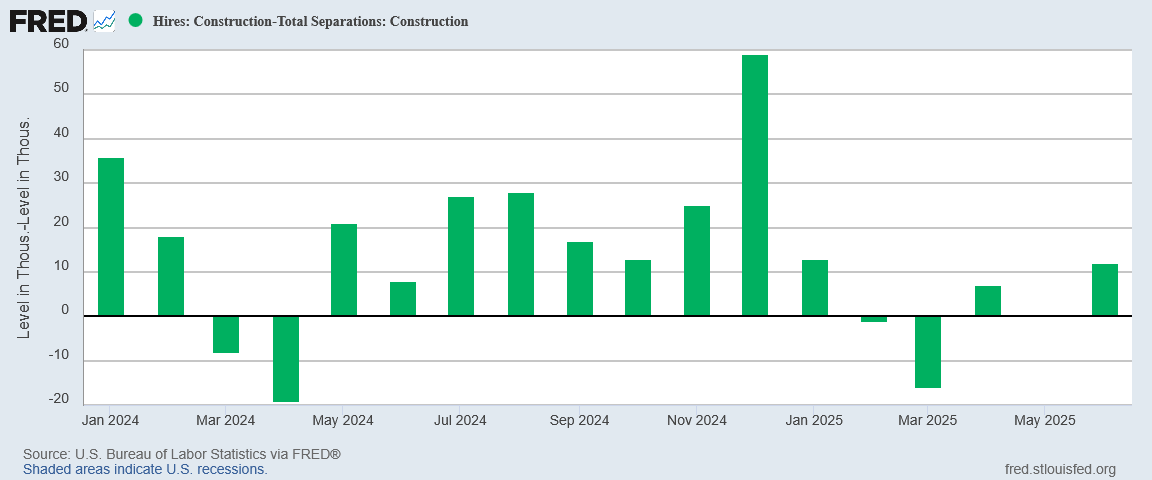

This is not to say there were not some bright spots in the JOLTS report. Net hiring in construction did increase.

Still, net hiring for construction in the first half of 2025 is demonstrably weaker than it was for all of 2024.

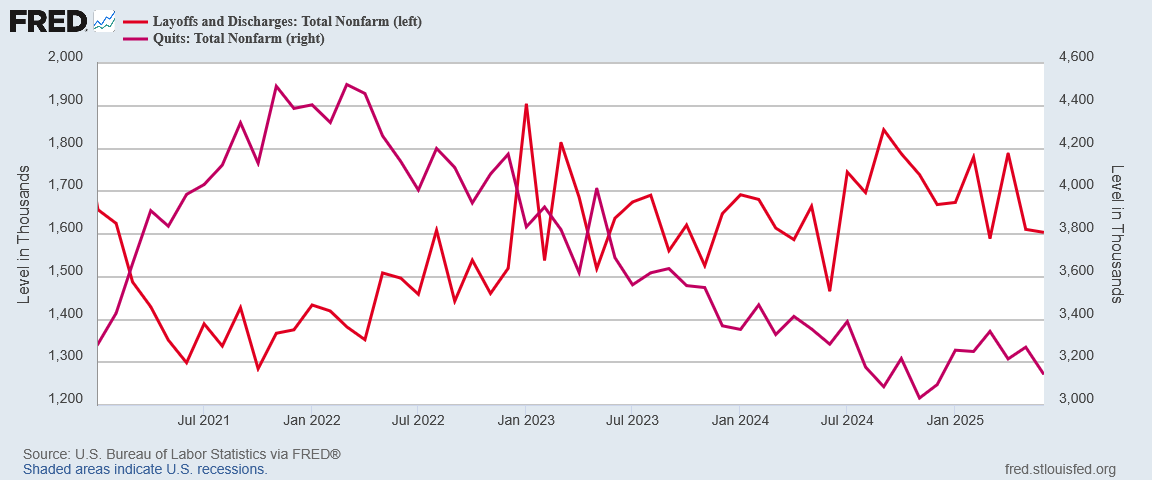

Additionally, layoffs and quits did not follow the divergent paths they have had for several months now.

However, despite these small silver linings, the JOLTS data for June was simply not good news for workers.

As the June JOLTS data was not good, we have to anticipate the likelihood that July will not be any better, and could be worse, particularly for manufacturing. That likelihood is all too real, unfortunately.

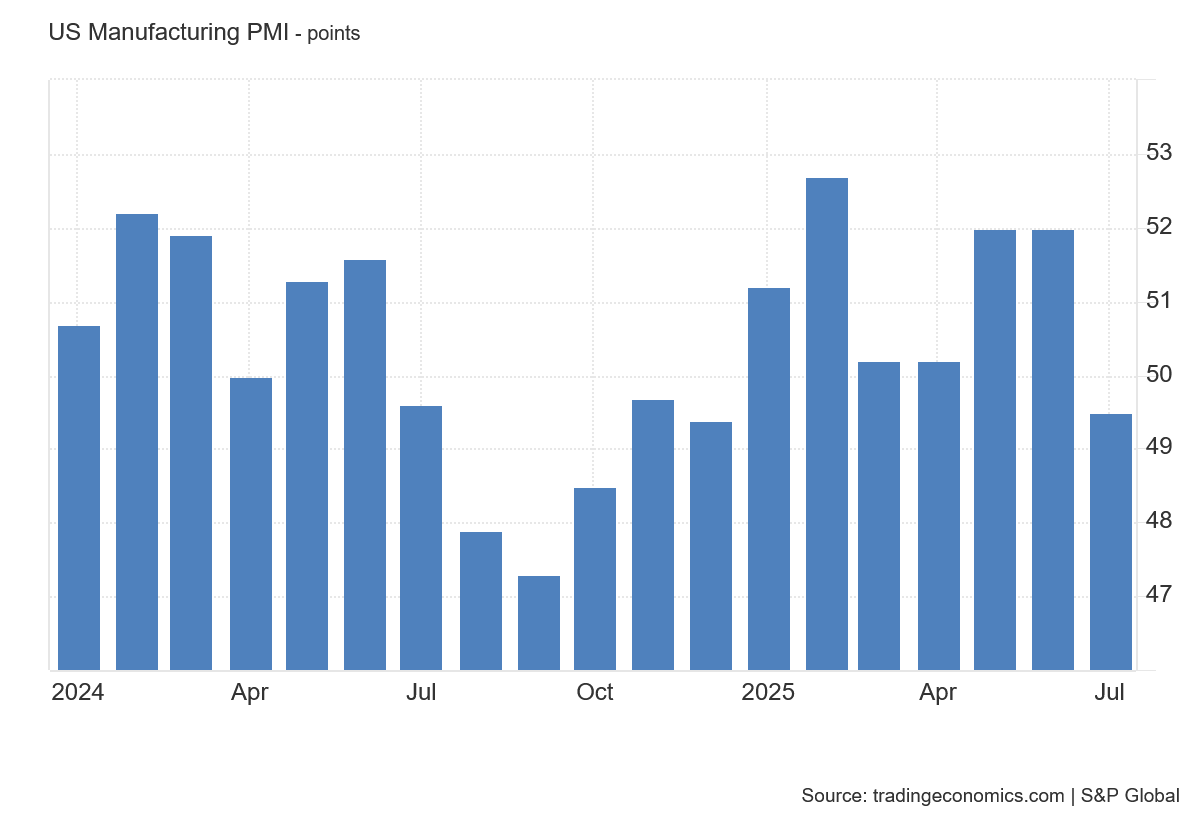

Manufacturing overall in the United States fell into contraction for July, according to the S&P Global Purchasing Manager’s Index.

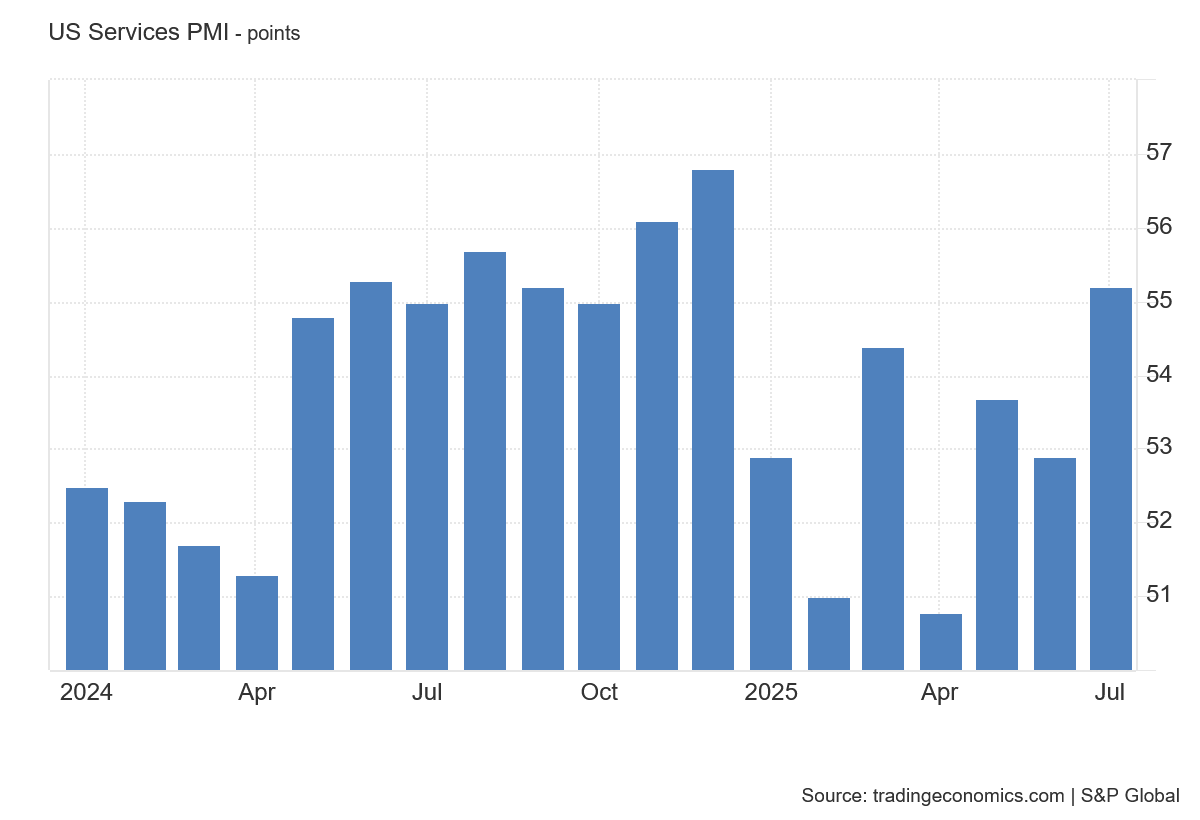

Services, on the other hand, saw an increase in expansion in July, according to the Services PMI.

An economy which favors service employment sectors over manufacturing employment sectors is not one on a track to become, in Donald Trump’s words, “a manufacturing superpower.”

The PMI data leaves open the possibility for improvement in jobs overall for July, but if the disparity between manufacturing and services extends past the PMI, the end result will not be good for workers, and in particular manufacturing workers.

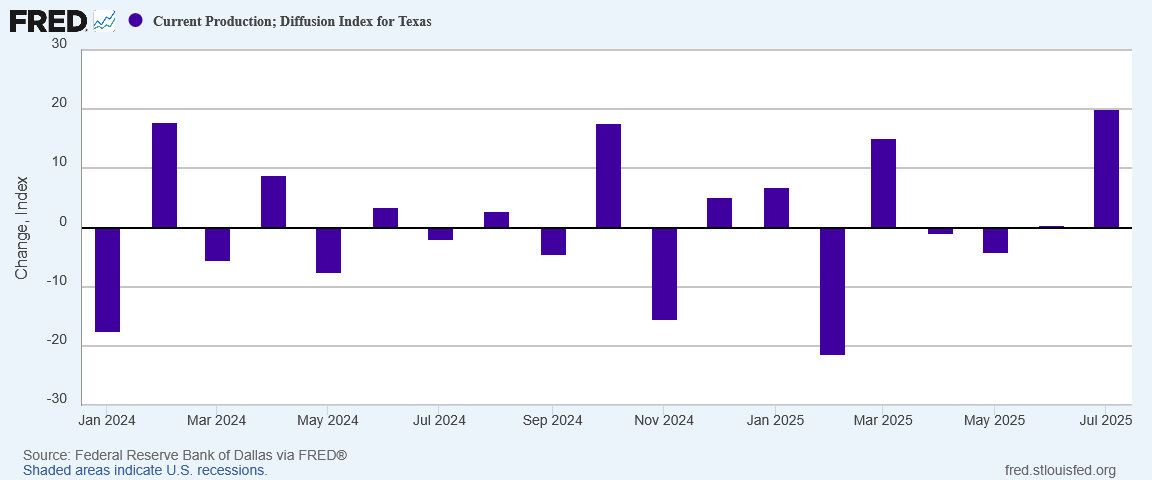

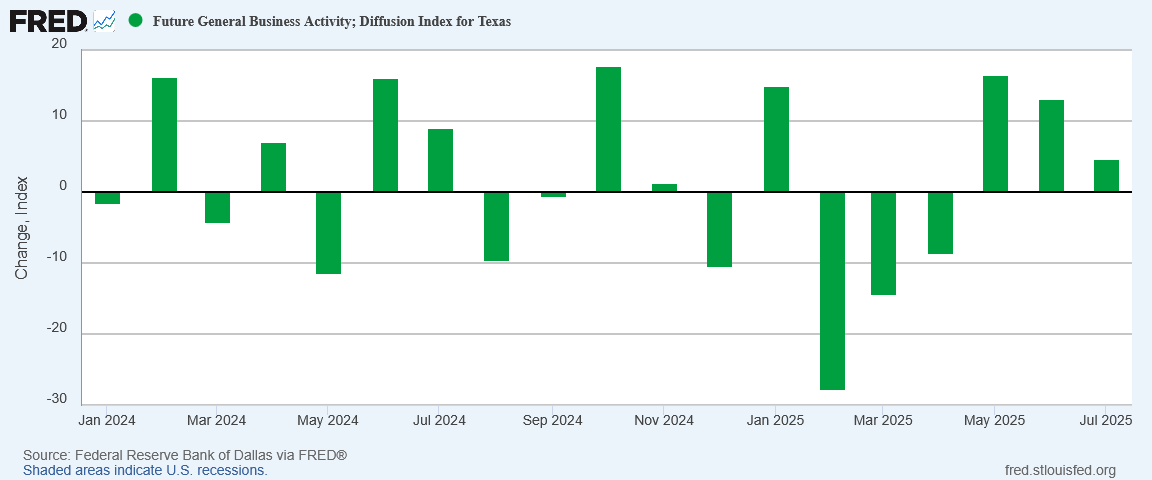

We do well to note that the PMI data is a nationwide survey. At a state and regional level, there are indications the manufacturing outlook is improving in some areas, especially in Texas. According to the Dallas Federal Reserve, Texas is experiencing a resurgence in manufacturing.

The prognosis for future business activity has slowed considerably, but is still managing to stay positive.

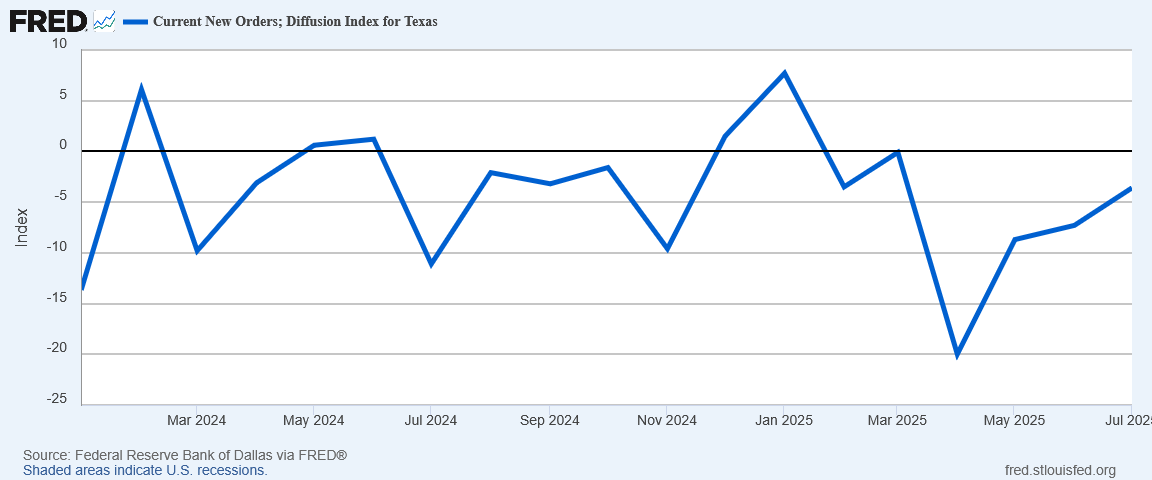

At the same time, the Dallas Fed projects the decline in Current New Orders for the Lone Star State to have slowed significantly since April’s plunge.

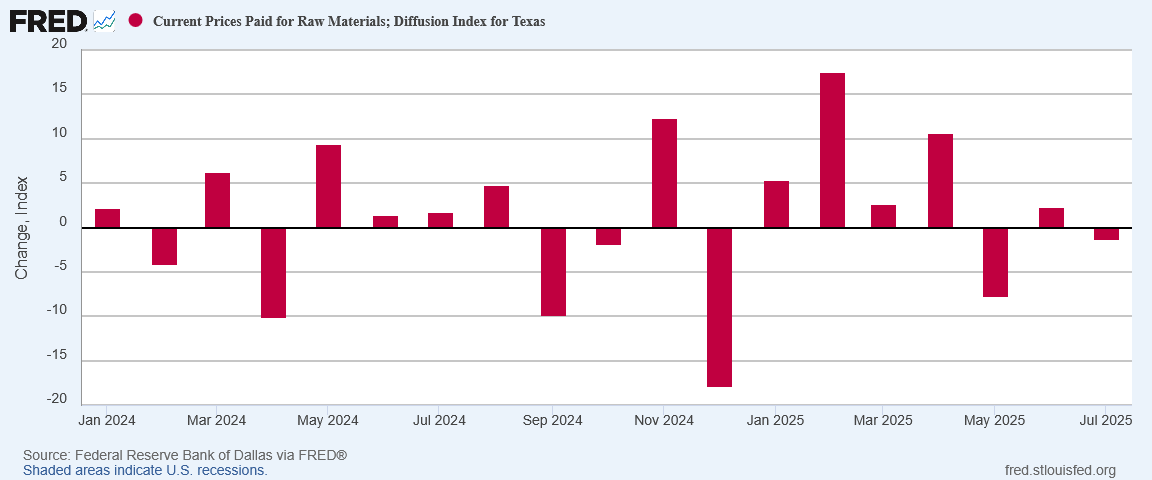

What is most encouraging is that, despite months of corporate media histrionics about how tariffs will cause rampant inflation, the Dallas Fed found Texas producers have lower raw materials prices.

Worried that tariffs are bringing on inflation? The Dallas Fed’s data is the latest data set showing that such fears belong firmly in the “not yet, possibly not ever” column. Despite all the corporate media pearl clutching and FOMC prevaricating over tariffs, inflation remains ridiculously absent from the economic landscape.

While Texas is only one state, and thus we should not read too much into the Dallas Fed’s data on Texas manufacturing, the data is quite clear that, in most respects, Texas manufacturing is improving.

However, given the anemic outlook nationally from the PMI data, the strong Texas numbers serves to underscore how uneven the state of the manufacturing economy is across the United States. If manufacturing is contracting nationally but expanding in Texas, elsewhere in the US manufacturing is doing particularly badly.

That uneven state forces us to confront yet again the reality of the ongoing jobs recession in this country. However well the other aspects of the US economy might be doing, job creation has not been anywhere close to where it needs to be. While increases in manufacturing output are an indisputable economic good, what every country needs to grow its prosperity is jobs, and for quite some time the US has not been generating anywhere near what it needs.

However well the other aspects of the US economy might be doing, full employment remains a distant hope and not a near-term goal. Despite what the “experts” on Wall Street and at the Federal Reserve might think, the US is not at all where it should be in terms of jobs to be considered at “full employment”.

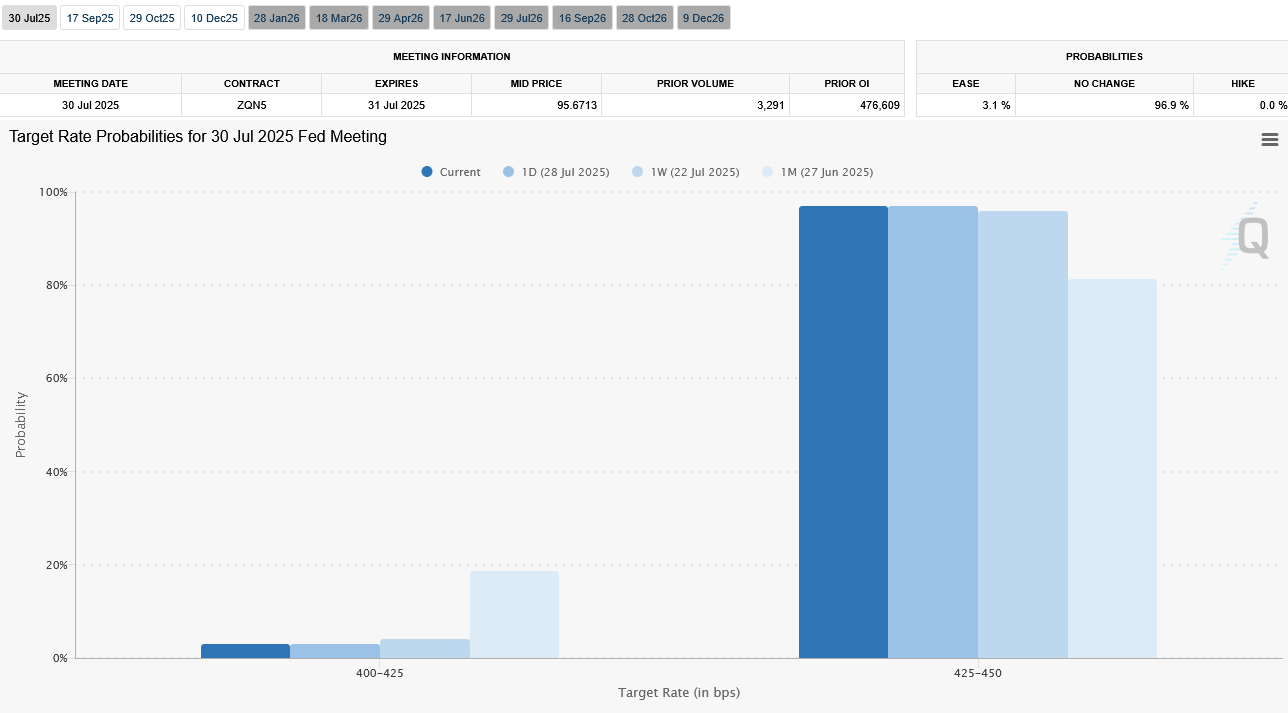

That makes the weak JOLTS data for June particularly galling because, despite a series of weak job reports, Jay Powell and the Federal Reserve are all but certain to leave the federal funds rate where it is yet again when they announce their rate decision later today. They should have trimmed the federal funds rate back in May at the very latest, but Powell simply refuses to do so.

It is darkly amusing to note that if Powell did announce a rate cut it would put Wall Street into cardiac arrest, as investors are all in on Powell punting yet again.

As much as businesses need a more growth-friendly environment, one which facilitates expansion of manufacturing plant infrastructure and other capital investment, Wall Street, historically the great investment engine which has facilitated much business expansion in the US, has accepted and priced in a conviction that Jay Powell will not do the right thing and lower rates.

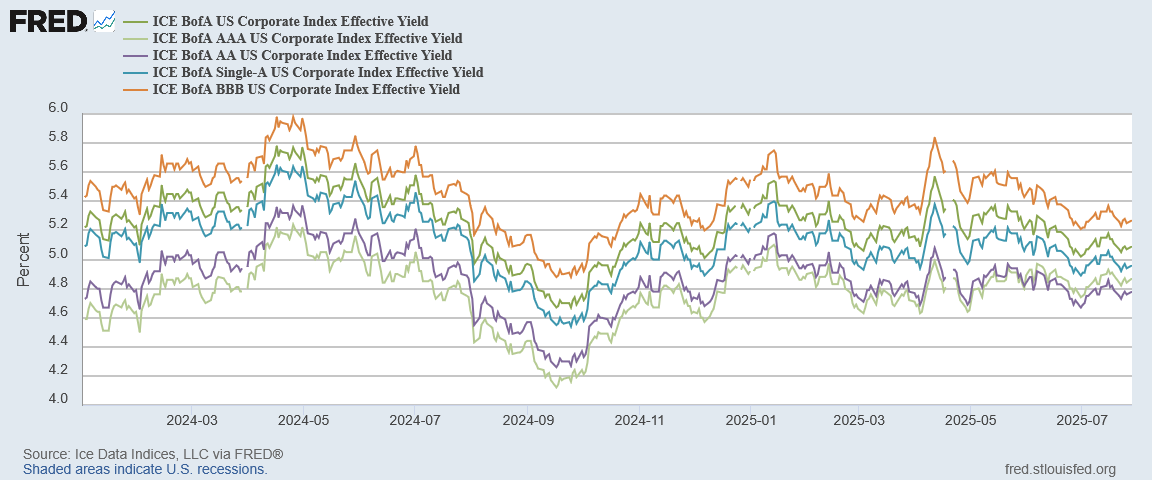

This despite the fact that corporate yields have more or less hit a floor for the past several months, with no real market move down.

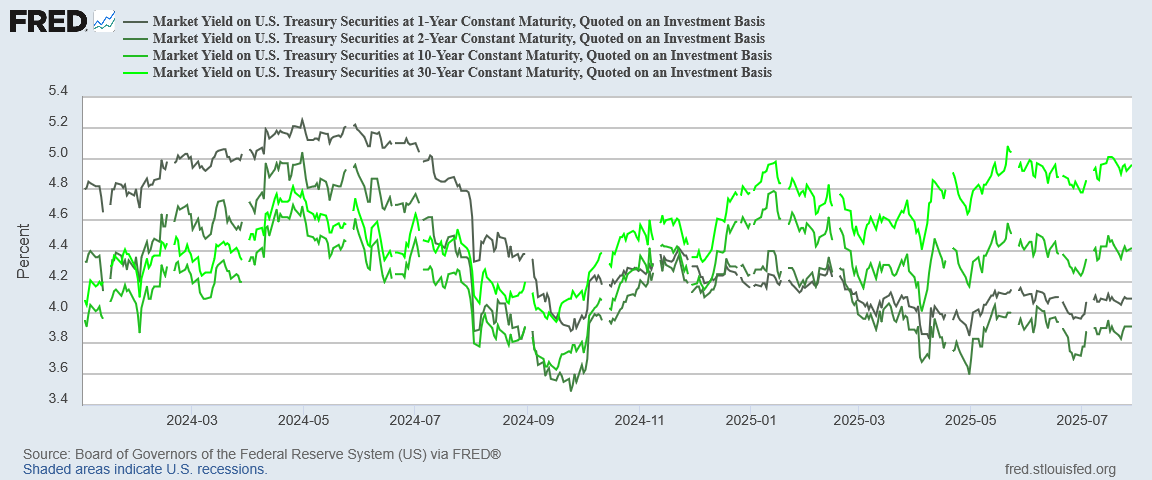

Treasury yields have not done any better, and the far end of the yield curve has even risen somewhat.

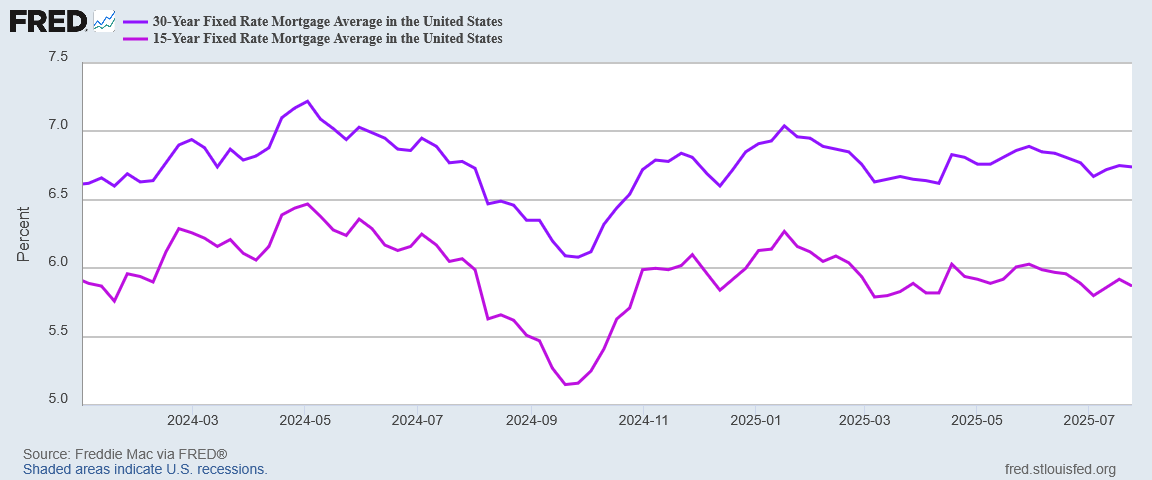

Mortgage rates are similarly stubborn, refusing to come down.

This is a macro-economic environment that demands a reduction in the federal funds rate. Interest rates need a catalyst to move lower, which a reduction in the federal funds rate would provide.

Despite this, Jay Powell is sure to remain completely inflexible where interest rates are concerned. That has been his pattern thus far in 2025, and there has been no indication that it will change.

Make no mistake: Powell’s strained logic that tariffs might someday in the far off distant future cause a price to rise somewhere even remotely credible. June’s inflation increase was the result of numerous factors, none of which were tariffs.

The Federal Reserve has a mandate to pursue full employment for the US economy. The June JOLTS data is but the latest data set to show conclusively that the US economy is nowhere near full employment, and that much more job growth is needed.

Within the Federal Reserve’s thesis regarding the linkage between job growth and interest rates, facilitating job growth under these conditions demands a rate cut. The very thing Powell needs to do—the very thing Powell’s job requires him to do—is the one thing Powell refuses to do. Powell has drawn his line in the sand, choosing anemic job growth and manufacturing job loss for the US economy in the name of preventing potential future inflation (because we all know that an “independent” Federal Reserve would never keep interest rates arbitrarily high just to annoy President Trump, who has been calling for a rate cut for months).

Jay Powell, along with the rest of the Federal Reserve, still believes the American worker should suffer the severest consequences from the 2022 hyperinflation cycle. This comes as no great shock, as it has been the Fed’s explicit policy since the start of the 2022 hyperinflation cycle that workers and consumer should suffer the most from the Fed’s inflation-fighting strategy.

Jay Powell could make Wall Street, Main Street, and Donald Trump all very happy if he surprised everyone by announcing a 50bps rate cut later today. Once the shock wore off all the pundits would praise him. Even Donald Trump might have a nice thing or two to say about him.

Wall Street, however, has zero expectation that Powell will do that. Unfortunately, so do I.

Does anyone else have a problem with one, unelected guy determining interest rates for the entire US, and really, the world? It’s utterly ridiculous that this is how it works.

I heard part of the Powell news conference today. He asserted the labor market was “in balance” it immediately made me think of your prior analyses on the “jobs recession”