March JOLTS Report: The End Of The Jobs Recession?

Strong Net Hiring Across All Sectors Is Good Reason For Hope

When the March Employment Situation Summary report came out, the obvious question was if the numbers were too good to be true. Now that the March Job Openings and Labor Turnover Summary report is out, we have a report that says perhaps the jobs numbers might actually be legitimate.

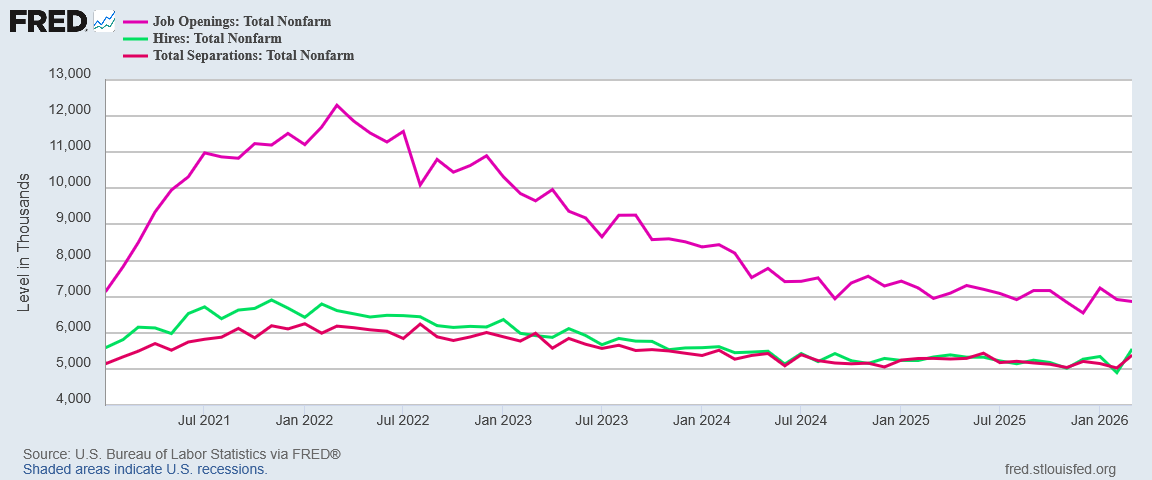

The number of job openings was unchanged at 6.9 million in March, the U.S. Bureau of Labor Statistics reported today. Over the month, hires increased to 5.6 million while total separations changed little at 5.4 million. Within separations, both quits (3.2 million) and layoffs and discharges (1.9 million) were little changed.

Corporate media was typically chagrined that the much-touted and supremely meaningless job openings number had actually slipped a little. The metric that does have meaning, however, is the hiring numbers.

Hiring rose significantly, and even though separations rose as well, overall net hiring rose at a pace in keeping with the jobs numbers from the Employment Situation Summary.

Does a strong net hiring number indicate the jobs recession has reached a bottom? Is a turnaround and actual growth in net hiring in the very near future?

With strong net hiring across all sectors, the March JOLTS report gives us good reason to hope so.

Openings Fell, But Hiring Surged

Corporate media much prefers to see large inflated job openings numbers. It’s not a rational fixation, since roughly half of those so-called job openings are not being filled by anyone. With that fixation, outlets such as Bloomberg were not happy that job openings ticked down slightly in March.

Available positions fell slightly to 6.87 million from a revised 6.92 million in February, according to Bureau of Labor Statistics data released Tuesday.

We can easily see that the emphasis on job openings is exaggerated, just by looking at the JOLTS data from 2021 onward.

Since the COVID Pandemic Panic, job openings have been consistently overstated. At its 2022 peak, the fictitious job openings were more than double actual hiring.

While job openings moved down slightly, when we look at the data since 2021, there is a distinct “bottoming out” of the job openings curve. Hiring and separations also are near the levels they were at in January 2025: 5-5.5 million hires and 5-5.5 million separations.

Job openings, hires, and separations have all trended down since 2022. Through 2025 into 2026, that trend has flattened out considerably, consistent with the data finally having established a floor. The March hiring data is an increase off that floor level.

That is the sort of trend turnaround that would signal the jobs recession that has bedeviled US labor markets since 2023 is at last coming to an end.

Certainly, that is the hope of Navy Federal Credit Union Chief Economist Heather Long.

“Is the hiring recession finally over? There are encouraging signs,” Heather Long, chief economist at Navy Federal Credit Union, wrote in an e-mail.

“The big concern is the war in Iran could halt that much needed progress in the labor market,” she wrote.

What is clear from the data is that net hiring in March was consistent with the growth in payrolls per the Employment Situation Summary.

Given that both reports are produced by the Bureau of Labor Statistics, we should expect some convergence, and might even view that convergence as an indication of statistical bias. At the same time, during last summer the two reports varied significantly, demonstrating that convergence was not a given.

For the past few months, however, the JOLTS and ESS reports have printed very similar results.

Sectors Advanced In March

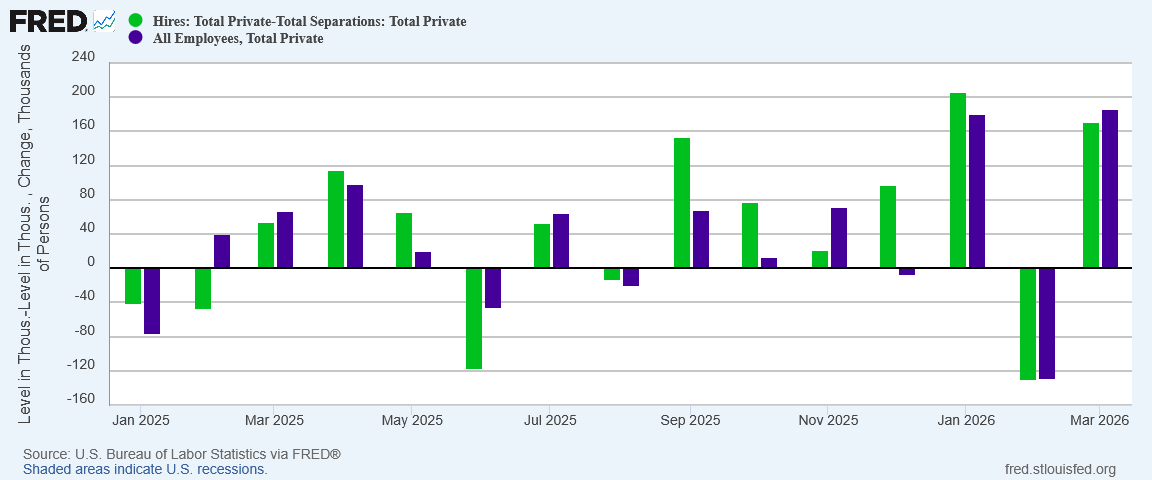

Even more encouraging than corporate media and Wall Street “experts” belatedly conceding that the jobs recession has been real is the broad base for the net hiring surge.

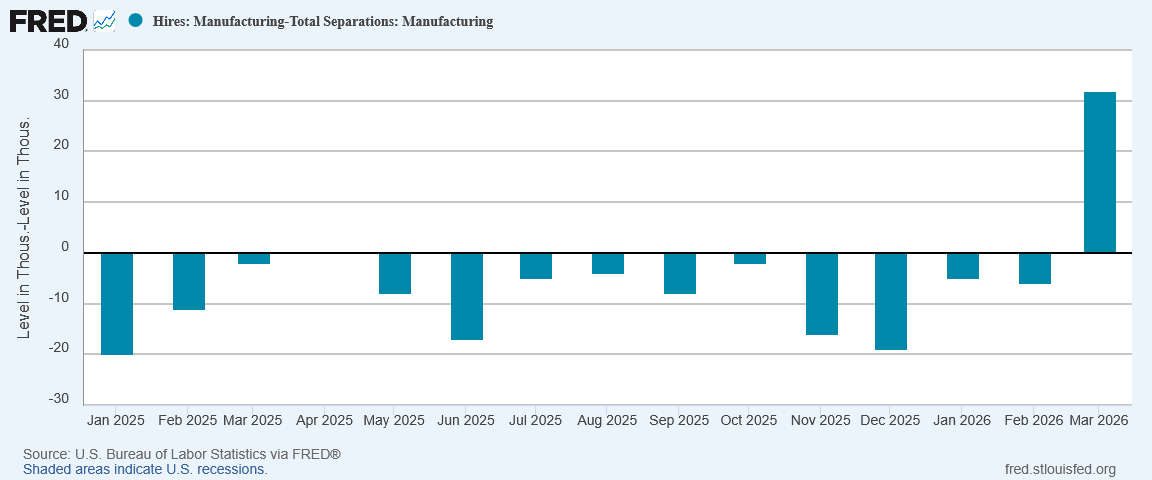

Manufacturing, which has been hemorrhaging jobs for over two years, saw a jump in net hiring.

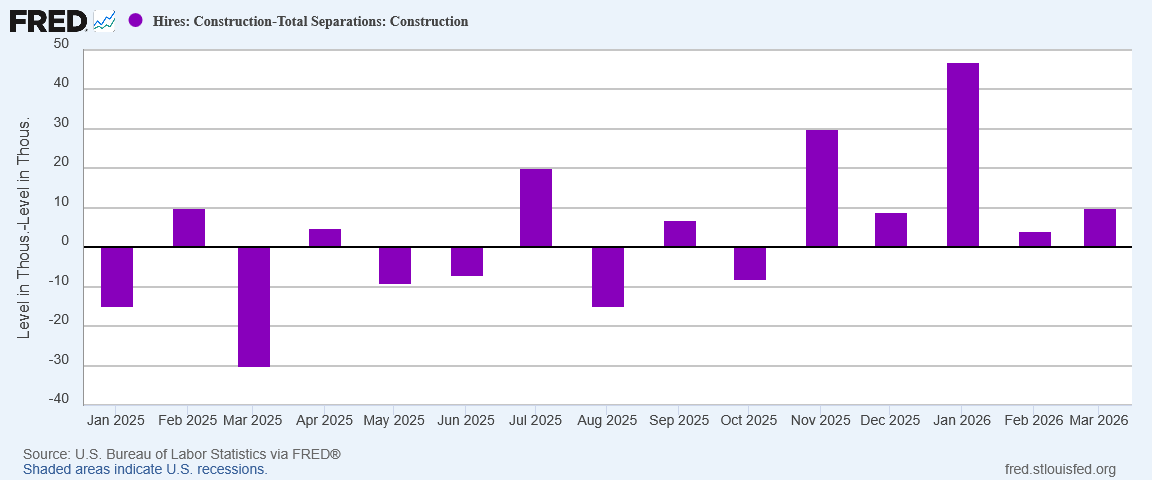

Construction, while printing cooler net hiring than in February, still turned in a fifth straight month of positive net hiring—the first time since October 2024 that has happened.

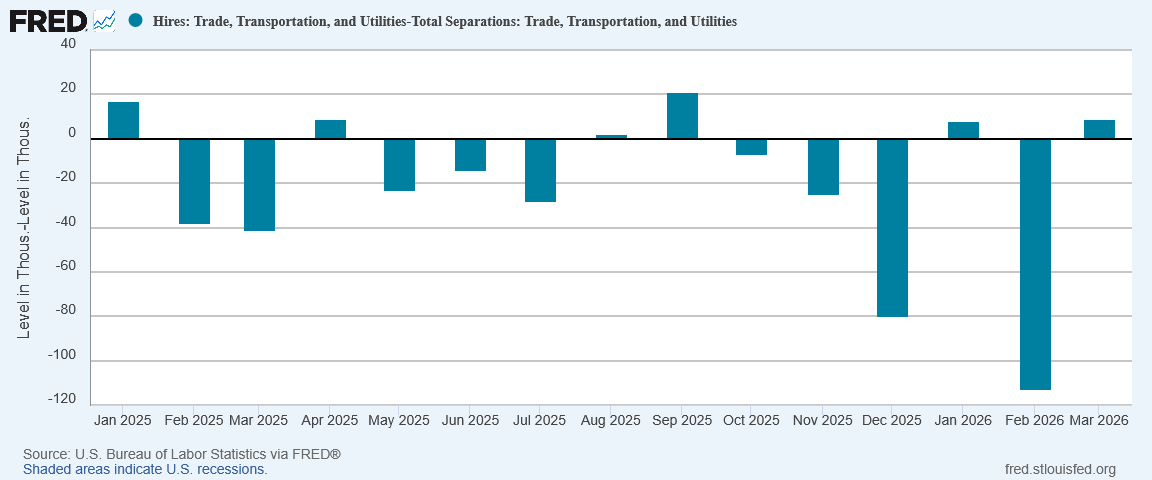

Trade, Transportation, and Utilities, a major service sector, rebounded from February’s job losses to show net hiring gains.

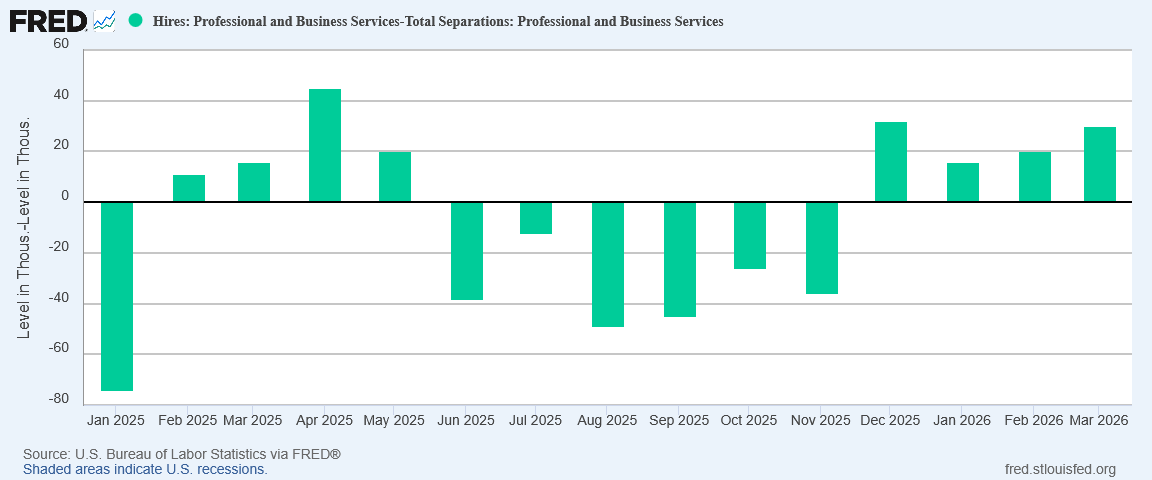

Professional and Business Services showed continued recovery, printing a fourth consecutive month of positive net hiring.

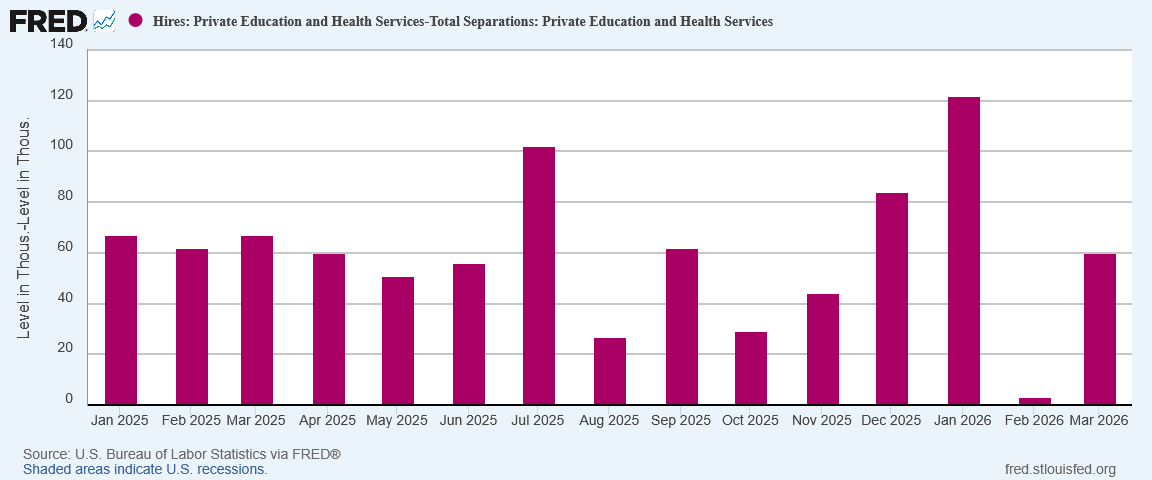

Healthcare, which has carried more than a few jobs reports, rebounded from a weak February to have a strong March.

Leisure rounded out the service sector also by showing a rebound from a horrible February, with its third best net hiring gains since the start of Trump Administration 2.0.

Every sector of private employment showed some measure of improvement in March. Such breadth in job growth is another reason to consider the possibility the jobs recession is ending. Broad job growth is an actual indicator of robust jobs markets, where hiring is strong everywhere rather than being concentrated in one or two industries.

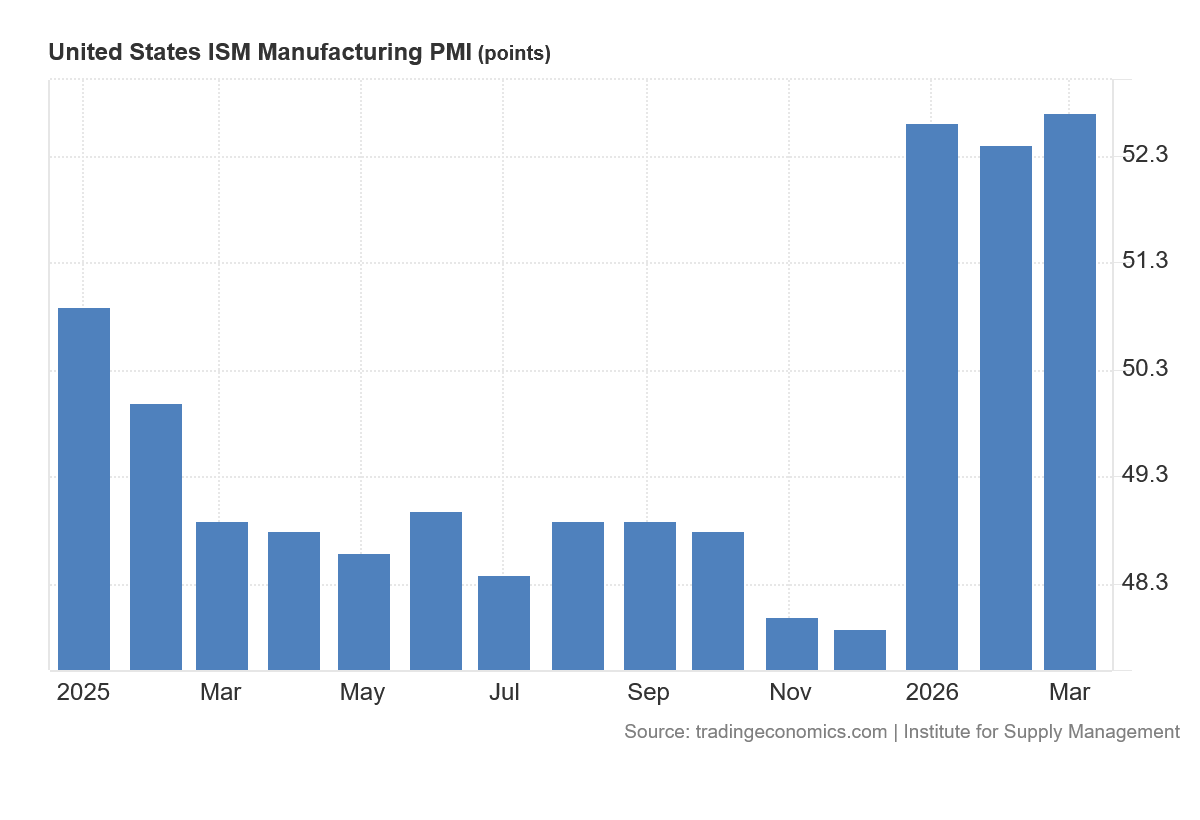

PMIs Show Strength In Manufacturing

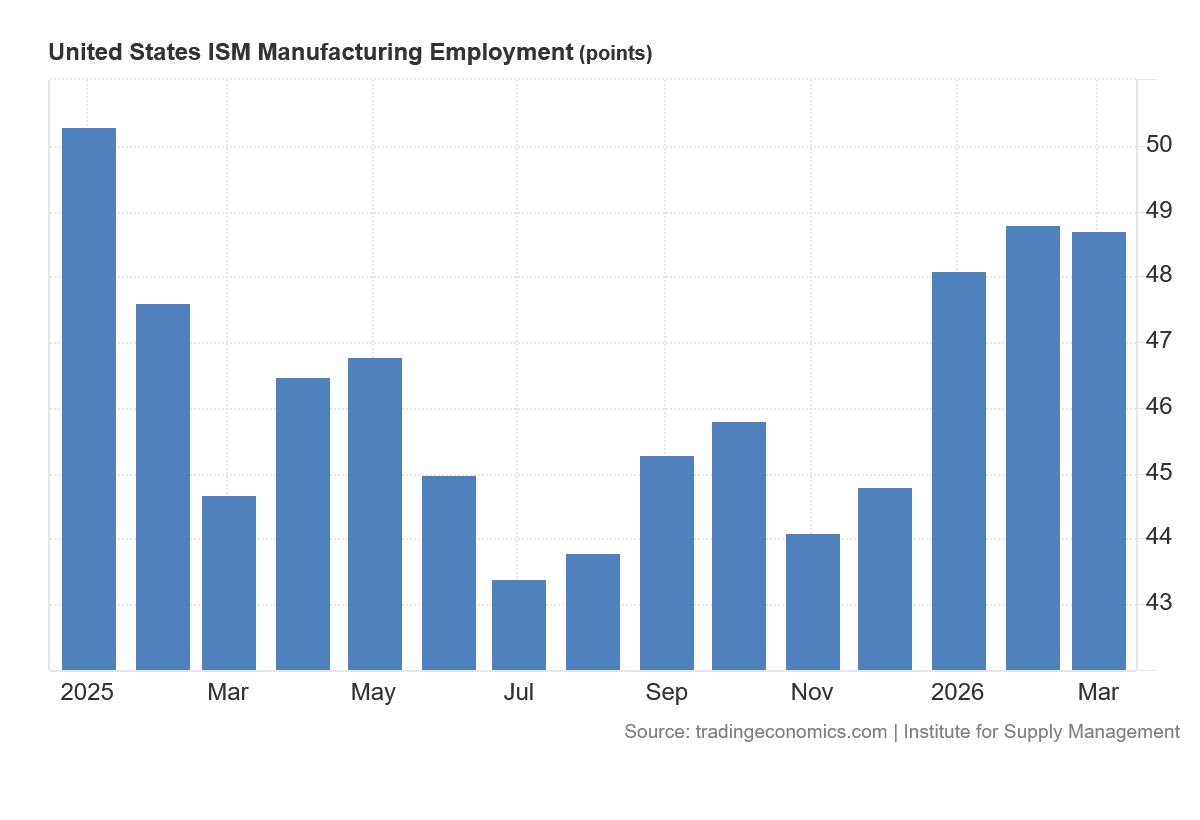

The JOLTS data paints an optimistic picture, and some might say too optimistic. The growth in manufacturing jobs, for example, is at odds with the Manufacturing Employment PMI data from the Institute for Supply Management, which shows the sector still contracting on jobs.

However, the overall Manufacturing PMI from ISM has been strongly in expansion territory since the beginning of 2026.

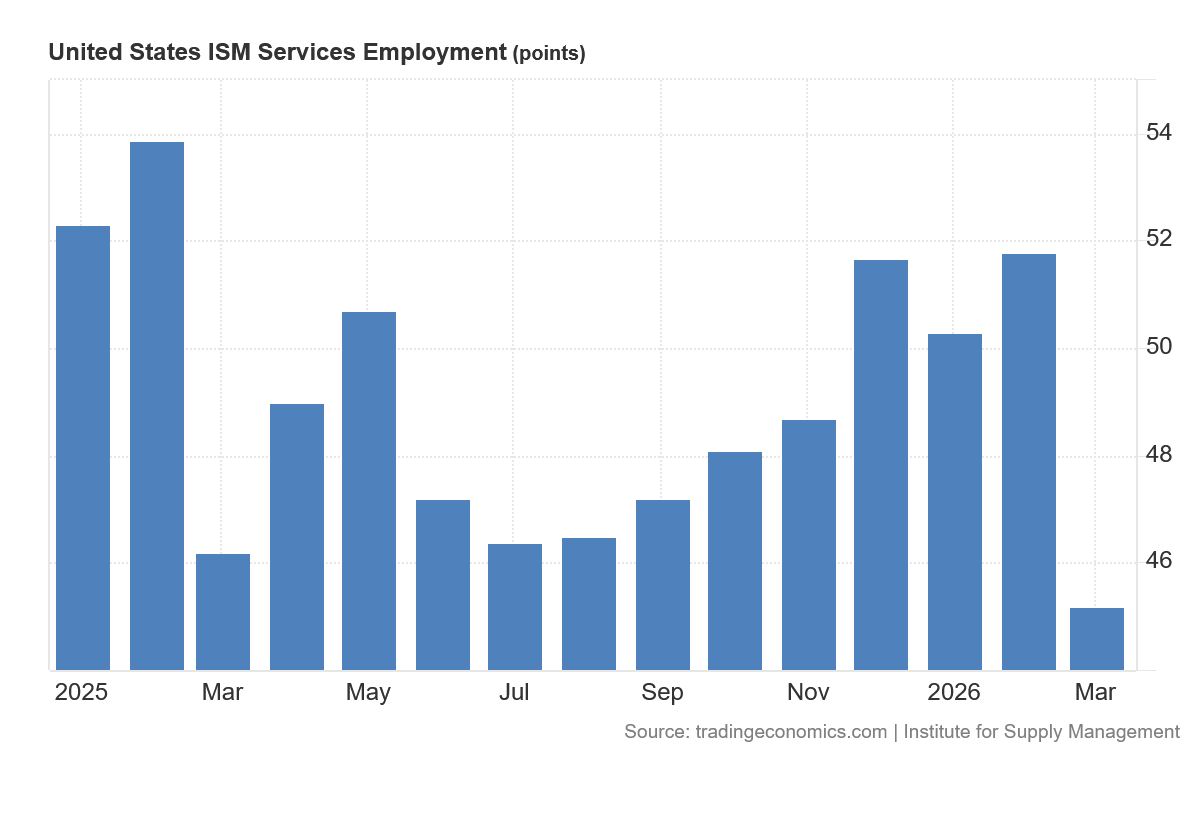

However, we should also note that the ISM Services Employment PMI also prints worse than the overall Services PMI.

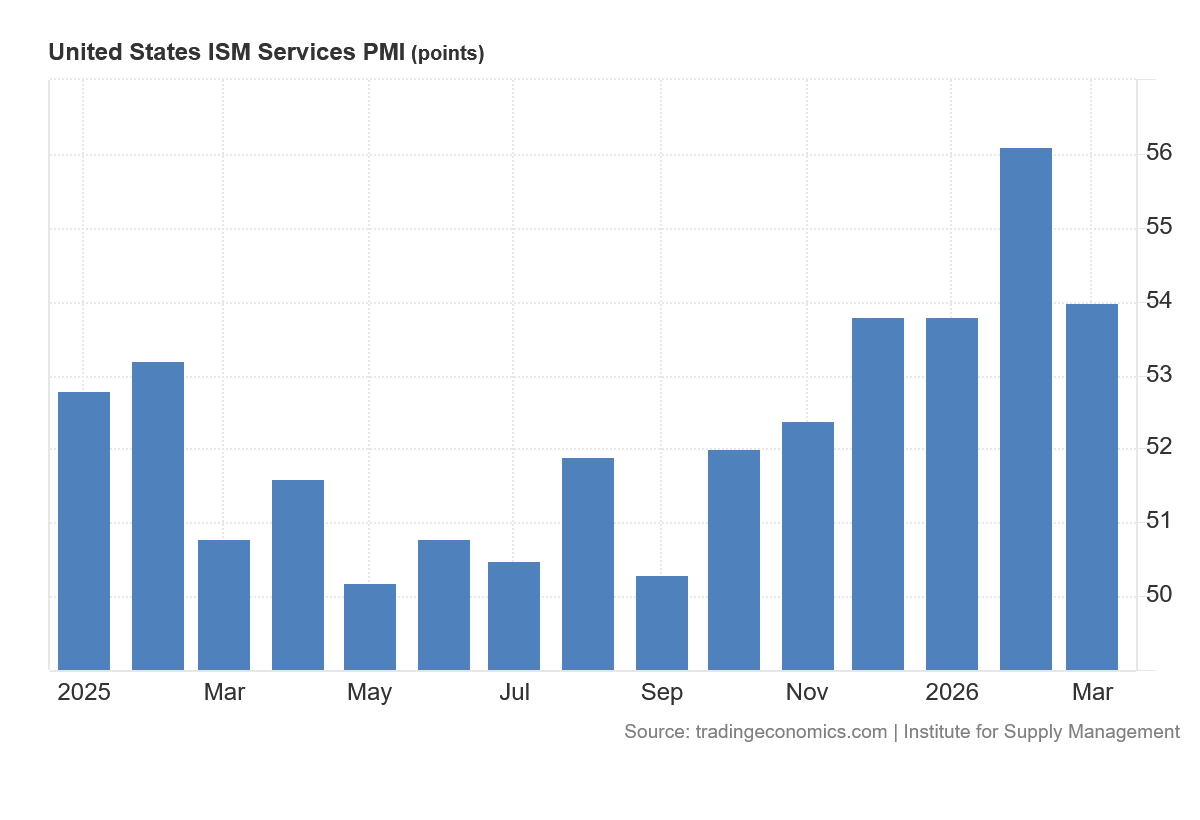

The overall Services PMI, however, shows consistent expansion in services since the start of 2025.

The employment components of the ISM PMI data gives us reason to doubt the JOLTS report, but the overall PMI shows industries expanding, a condition consistent as well as necessary for expanded net hiring.

The PMIs give us reason to be skeptical, but also reason to hope that jobs markets are starting to improve at long last.

The End Of The Jobs Recession?

One month does not make a trend, and we should take care not to read too much into the strong JOLTS data for March.

We should acknowledge, however, that the JOLTS data for March is strong.

The JOLTS data for March is strong across the board, a rising job tide that is legitimately lifting all job ships.

Strong job growth—strong actual hiring and not merely a tantalizing promise of a job “opening”—is an indication labor demand picked up in March.

Growing labor demand is essential to having improved gains in wages and earnings. The greater the actual pace of hiring, the greater the real demand is for workers, and the greater the pressure to bid up wages across the board. Just as scarce supply increases prices for goods and raw materials, scarce labor supply increases wages.

With hiring having trended down since 2022 before showing signs of bottoming out during 2025, we have not seen strong labor demand, meaning we have not seen strong wage pressures, and so we have not seen the level of robust wage gains many sectors need to see to finally catch up to the effects of the 2022 hyperinflation cycle.

With March data looking strong, the next question naturally turns to the upcoming April jobs numbers. Will the second month of war with Iran show continued job growth?

Will the dislocations and price shocks from Iran illegally closing the Strait of Hormuz and disrupting 20% of global oil supply show their full effect by suppressing job growth, choking off the potential jobs recovery even before it has a chance to get started?

The war with Iran made its presence felt in March, with pronounced energy price shocks driving both consumer price inflation and factory gate inflation. Those shocks did not make their presence known in the March jobs data.

Is April the month where the dislocations reverberating out of the Persian Gulf start to impact employment here in the US? Or is a jobs recovery underway capable of powering past those dislocations?

March was a strong month for jobs in this country. If April is even close to the same despite the headwinds of war, we may plausibly begin to consider the jobs recession coming to an end at long last.

Not convinced yet Peter. jobs aren't the only sign. Too many articles I'm reading and linking today in my Economic News section @https://nothingnewunderthesun2016.com/ are still painting a pretty bleak picture, but then again I could be slanted towards those type of articles. But I like to look at all sides. Linking you article today as usual!!

I was not expecting such good economic news - this makes my day!

Now, If Trump can quickly win the war, gas prices will come down, optimism will prevail, and the MAGA agenda will continue - right on through the midterm elections!