The irony in the March Personal Income and Outlays report was that the energy price shock it disclosed was not at all shocking—that there would be energy price inflation has been known for weeks, and the BEA’s data showed few surprises in that regard.

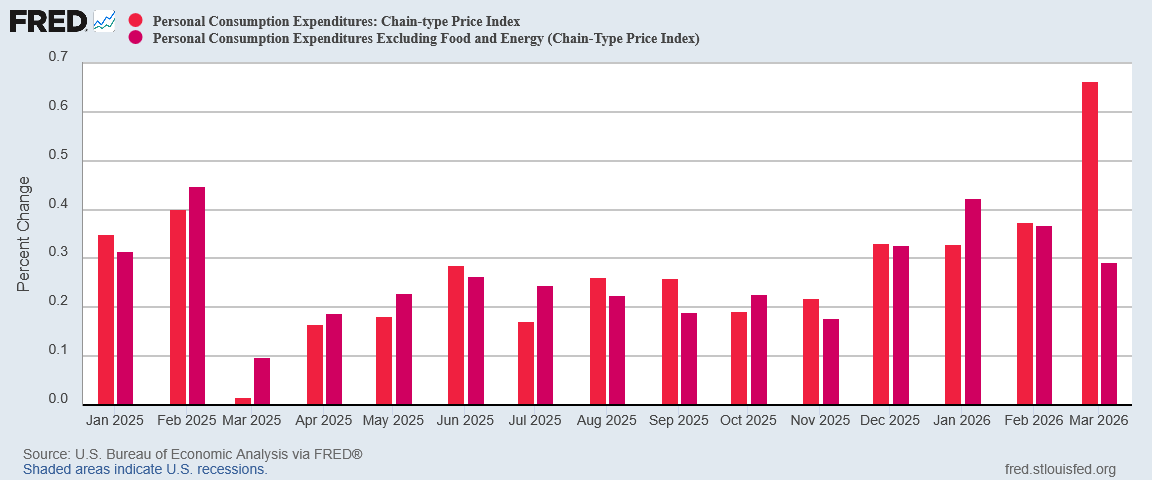

From the preceding month, the PCE price index for March increased 0.7 percent. Excluding food and energy, the PCE price index increased 0.3 percent.

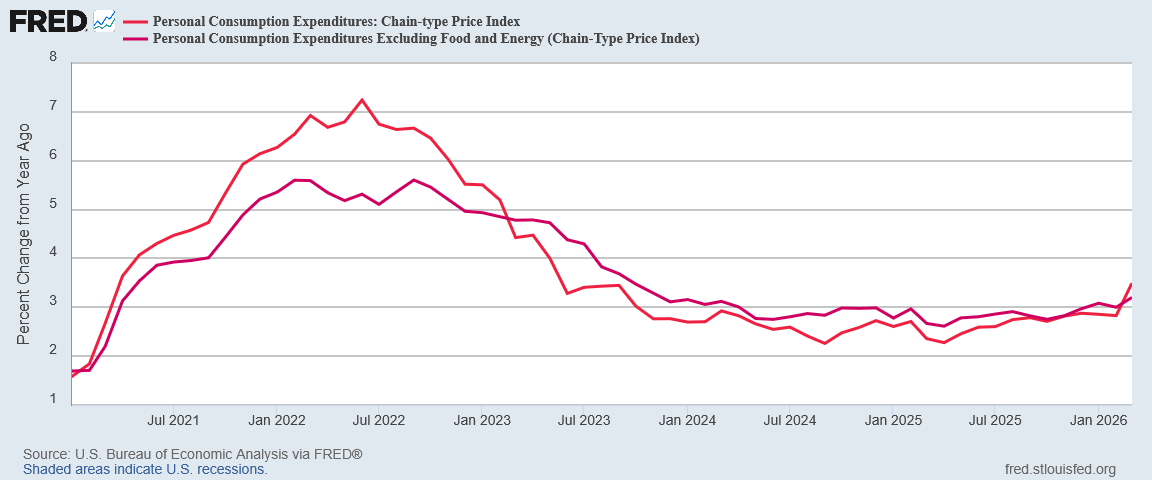

From the same month one year ago, the PCE price index for March increased 3.5 percent. Excluding food and energy, the PCE price index increased 3.2 percent from one year ago.

Everyone who was not comatose was already aware that energy prices were soaring and knew the reason why—Iran disrupting Persian Gulf oil flows by closing the Strait of Hormuz. The US war with Iran is the reason Wall Street projected year on year inflation per the PCEPI would be 3.5%, and for once Wall Street was spot on.

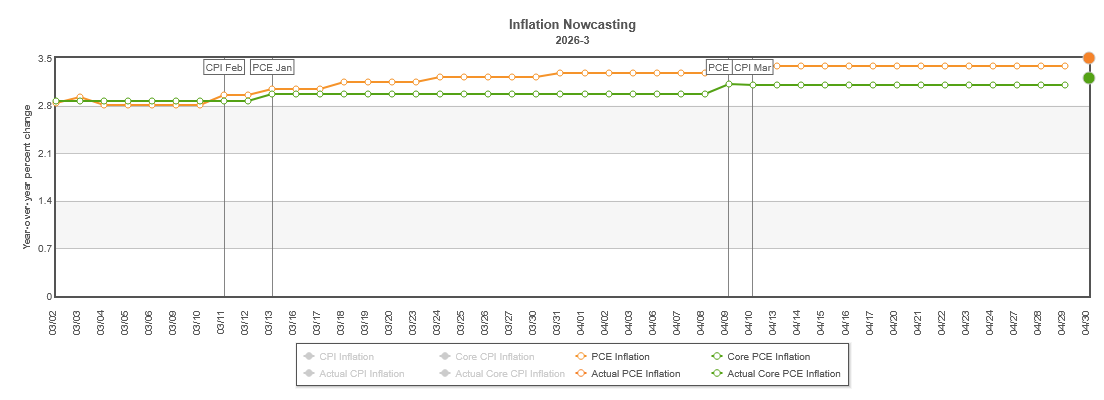

The suddenness of the war and of Iran’s strategic response to close the Strait of Hormuz left the usually highly accurate Cleveland Fed’s inflation nowcast a few steps behind the curve, with its projections for both headline and core year on year inflation 0.1pp below the actual print.

Like the earlier CPI report, the PCE data confirmed that inflation has returned to the US economy.

Yet the data was not without a few bits of silver lining. While energy price inflation surged, prices in other areas rose substantially less, or even declined.

Energy price inflation is real. Other inflation…not so much.

Not Quite The End Of “More Of The Same”

The Personal Income and Outlays report runs nearly a full month behind, so by the time we had the February data Operation Epic Fury had been headline news for nearly a month. The news from the Middle East made it clear that there was going to be a significant energy price shock in the March data. The news from the Middle East was why my assessment last month was that the February PCE data marked the end of “more of the same.”

Even when I first read the BEA’s report yesterday morning, that assessment appeared to be confirmed. However, that assessment was not entirely true.

Driven by energy prices, headline inflation did rise year on year, which was completely expected.

Core inflation also rose year on year, but the trend line was in keeping with prior months. Operation Epic Fury did not add new inflation pressures to core inflation.

One “more of the same” aspect of the March data was that core inflation actually eased month on month in March.

While consumer price inflation has been trending up year on year for both the headline and core metrics in the PCEPI, since January core inflation month on month has gotten cooler, dropping from 0.42% in January to 0.29% in March.

Not only did Operation Epic Fury not add new inflation pressures, it also did not sustain some of the inflation pressures already present.

As it turned out, past energy prices, the PCE data actually does contain “more of the same”, with several previous months’ trends being continued.

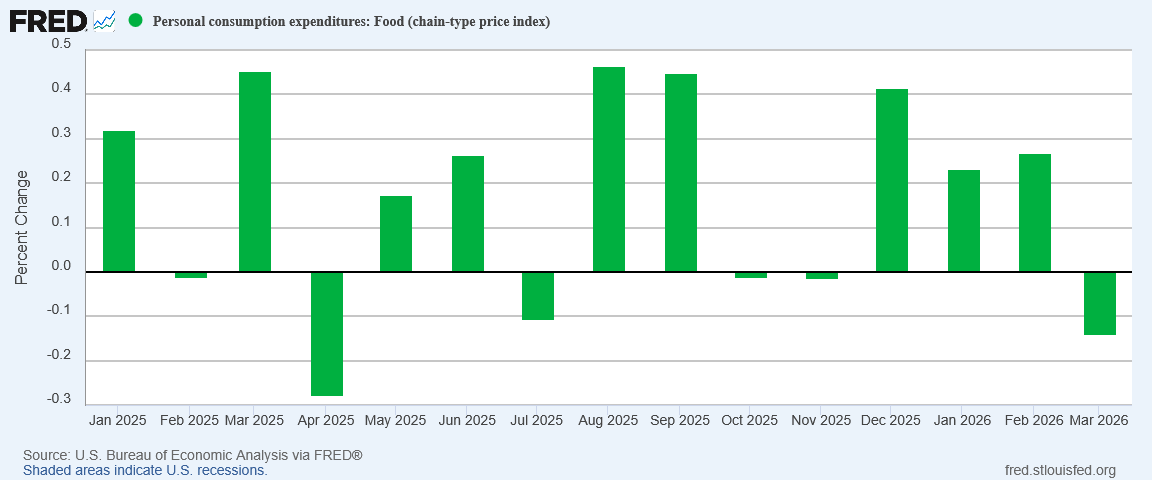

Energy Rose, But Food Fell

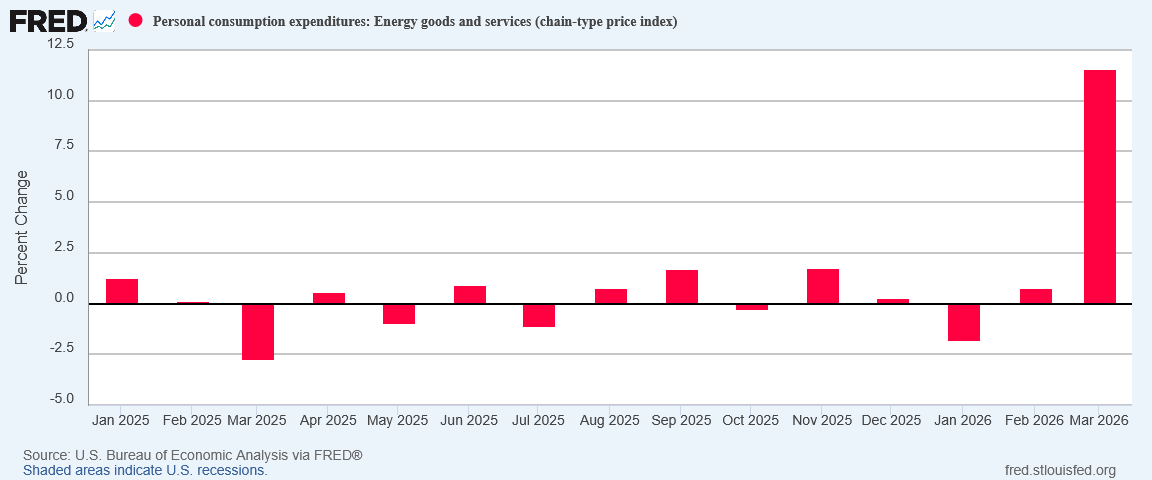

Headline inflation surged in March because energy price inflation surged—that much is obvious.

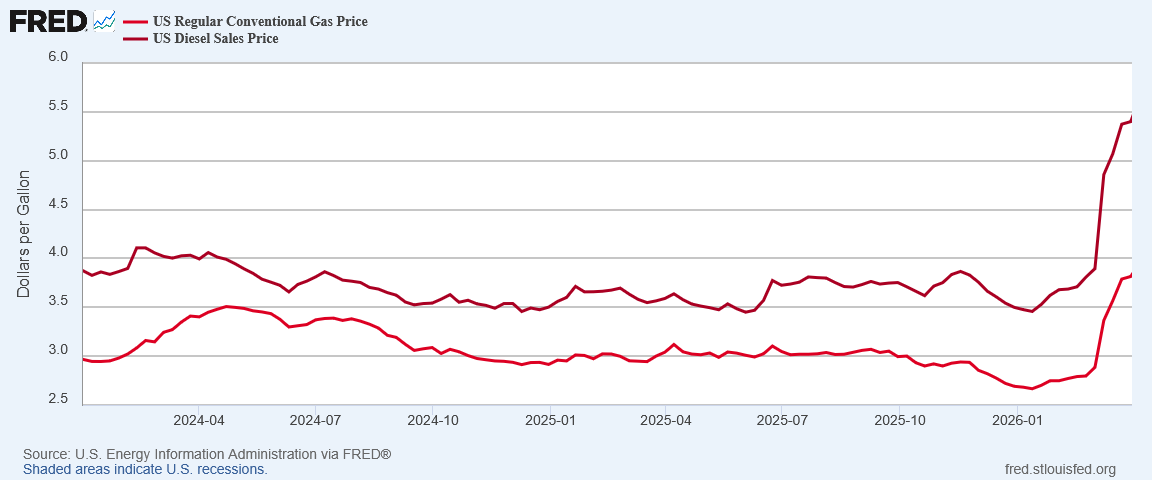

With oil prices up 33% on the month, how could energy prices not surge?

The surge was helped along by both gasoline and diesel retail prices having a violent trend reversal to also rise 36% and 42% on the month.

What did not help headline inflation move skyward were food prices. Food prices printed deflation month on month in March.

With food prices having shown inflation through the winter months, seeing the food subindex decline is a welcome change.

Even though energy prices have a tendency to permeate all other prices, food prices are the first indication that the inflationary pressures brought on by Iran mining the Strait of Hormuz have not moved beyond energy prices…yet

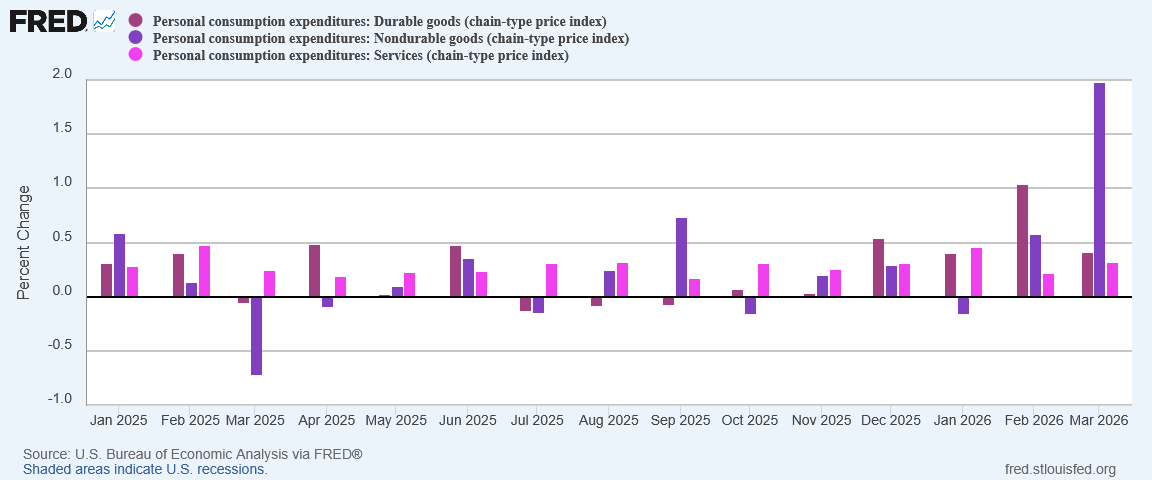

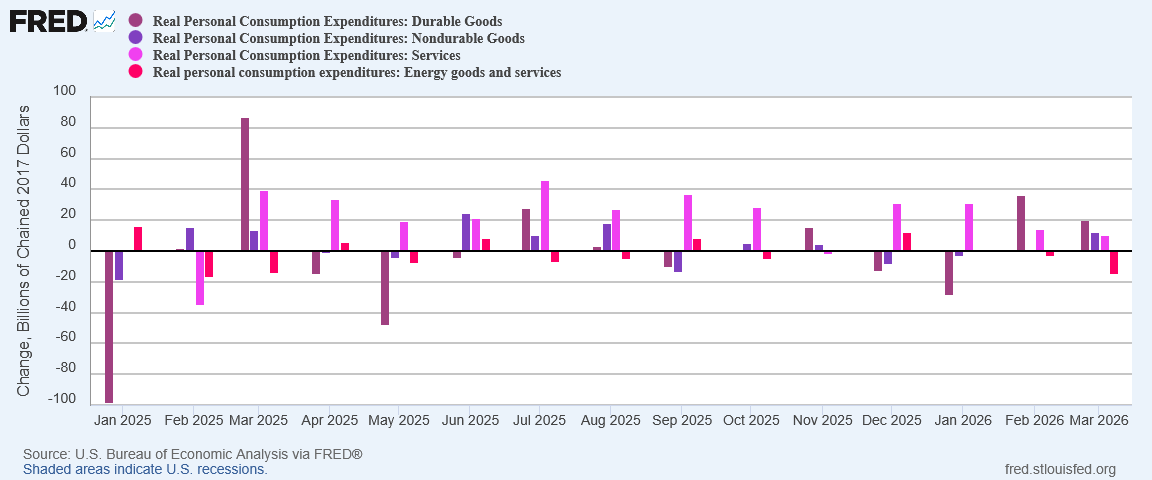

March Was Nondurable Goods’ Month To Rise

In the February data, looking past the headline numbers we saw that durable goods surged significantly. In March, it was non-durable goods’ turn to take off.

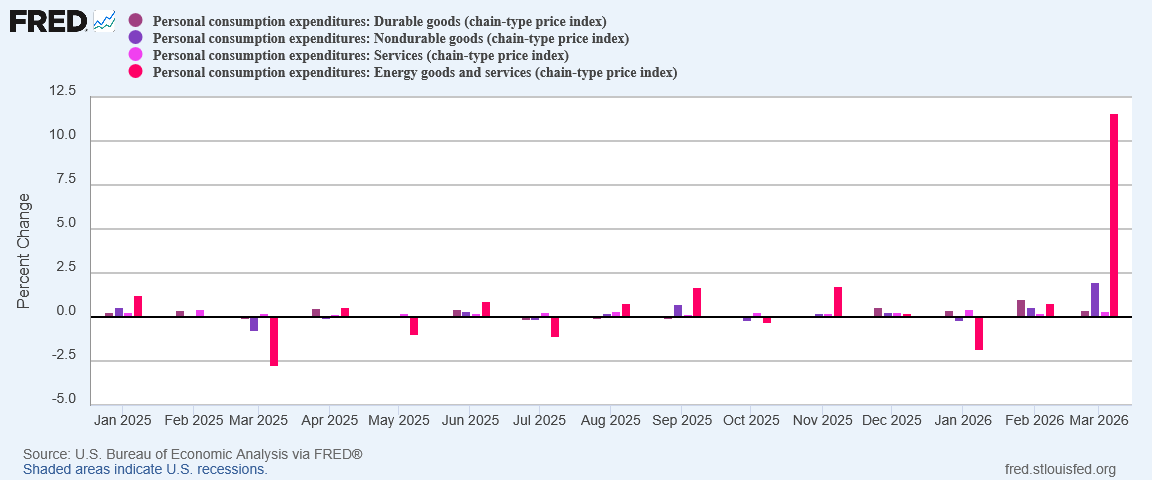

However, there is little doubt that energy goods drove most if not all of that increase.

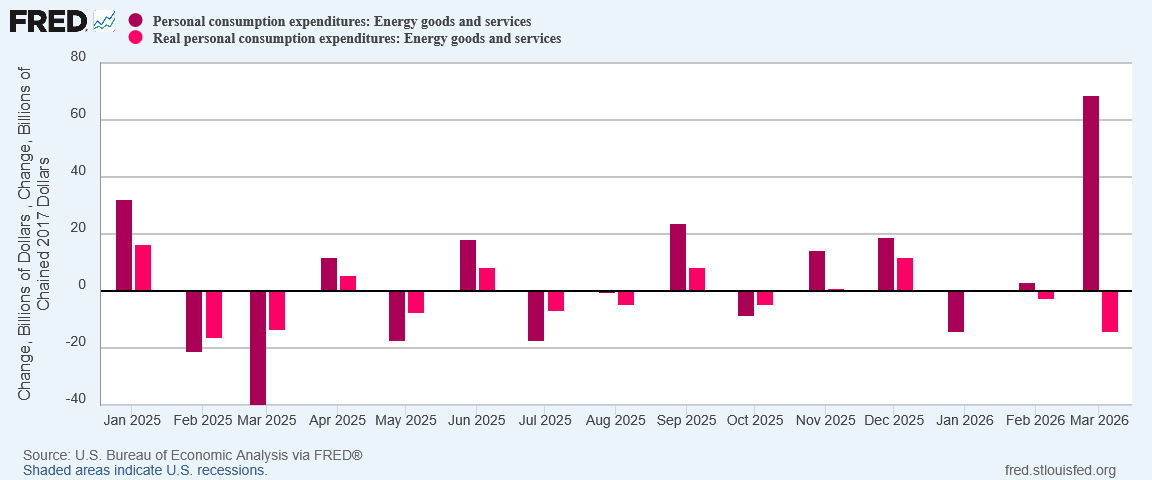

That is what an 11.6% rise in energy goods and service prices will do to the PCEPI subindices.

That extreme surge in energy pricing also highlights a point of particular concern. Either despite a nearly 12% rise in energy goods and services pricing or because of it, real expenditures on energy goods and services declined in March.

People spent more on gas at the pump in March, but in real terms they bought less gas. While this is a somewhat predictable consequence of a price shock, this is also illustrates how sudden price shocks can lead to stagflation: instead of the rising prices being the consequence of rising consumption, rising gasoline prices have produced decreasing consumption. What normally acts as a brake on consumption for March energy prices acted as a suppressant instead, preventing rather than limiting consumption growth.

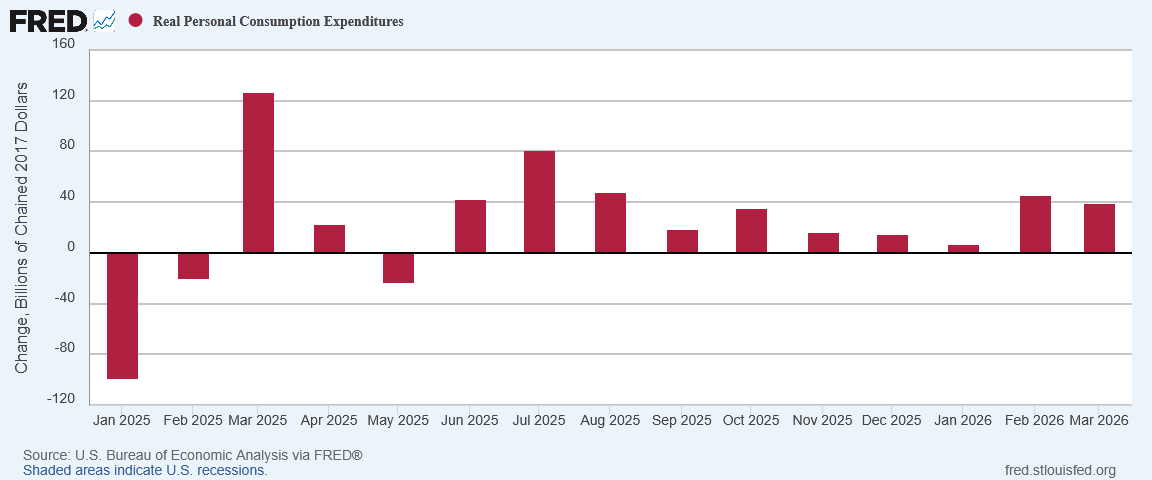

We see further evidence of this in the cooling of growth month on month in real personal consumption expenditures for March.

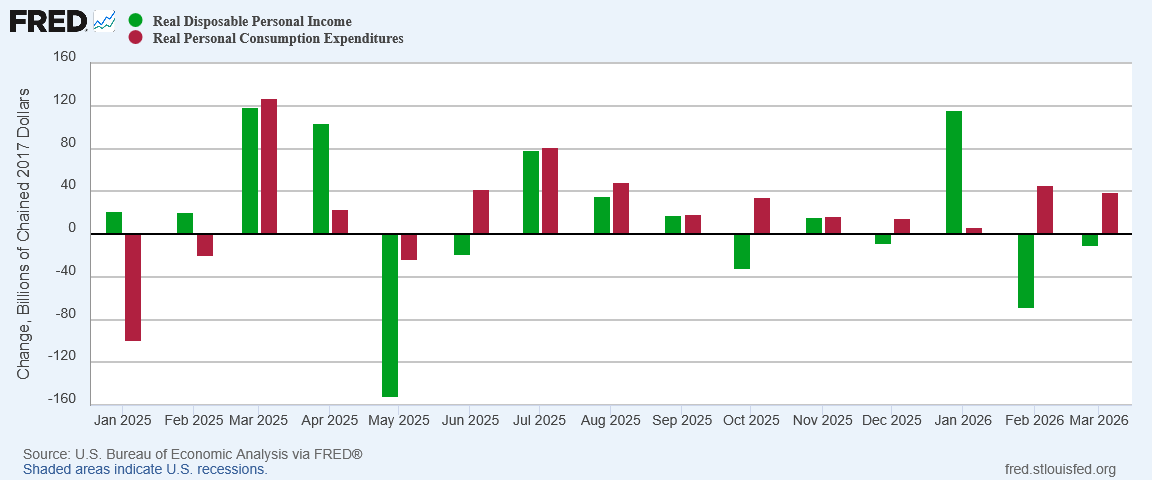

That real disposable personal income declined again in March does not help further any narrative of substantive economic growth.

When there is no growth in real disposable personal income, there are not going to be many prospects for sustained consumption growth. Consumption growth without income growth invariably hits a wall.

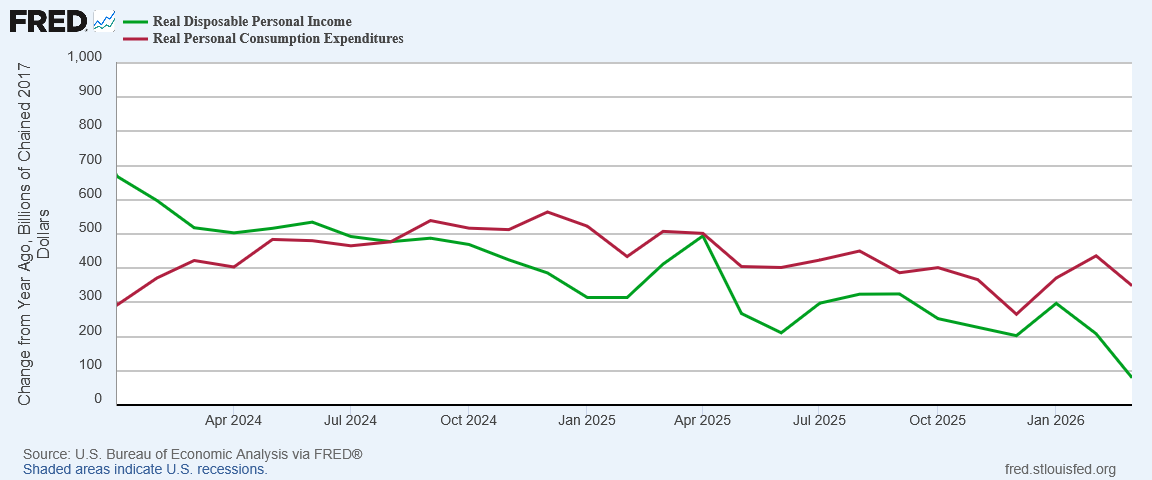

One data point that unfortunately is very much “more of the same” is the continued long-term decline of real disposable personal income year on year, which is accompanied by a somewhat more problematic downward trend in real personal consumption expenditures.

It is trends such as these that force us to mention “stagflation” with regards to the energy price shocks from the war with Iran. These are trends which suggest consumption growth is weakening in this country, and a sudden surge in energy prices can very easily suppress growth further.

When inflation is the proximate cause of absolute demand destruction, that is when we are starting to see stagflation.

Powell Remains Clueless About The Data

These key trends in real disposable personal income and real personal consumption expenditures also serve as yet another rebuttal to outgoing Federal Reserve Chairman Jerome “Too Late” Powell’s stubborn silliness in refusing to understand the data he pretends to study, as we saw from his final question during Wednesday’s post-FOMC press-conference.

Thank you, Chair Powell. Richard Escobito with CBS News.We’ve talked a lot about gasoline prices and even you mentioned airline ticket prices, both of which are up dramatically because of the war in Iran. And so I wonder, are you seeing that way down consumer spending in other parts of the economy and if so how worried are you that that will be a drag on growth.

Chairman Powell: you don’t see you don’t see it in spending yet you really don’t I mean as one of your colleagues said the economy has been resilient it really has not just this time but it’s been remarkably resilient for some years now. The U.S. economy has just powered through shock after shock, and consumers are still spending. And that’s what the banks will tell you, credit card companies will tell you, the retail sales numbers that we got most recently. People are still spending. And, you know, how long can that go on in a world where, if gas prices were to go up a bunch more, that’s taking otherwise spendable money out of people’s pockets, but right now we don’t actually see much slowdown yet—certainly none from this—but you think logically you will, because people have a certain amount of money they’re spending. If they’re spending 25% more in gas or something like that, then you know that’s going to come out of other spending. But again, we don’t see it yet.

Richard Escobito: One last thing. You mentioned those economies in Southeast Asia that are particularly dependent on petroleum, they make a lot of the stuff that American consumers buy. So was there any discussion today about whether or not those costs getting passed along to consumers is a real concern, and whether or not that might push up inflation?

Chair Powell: So all of those things are in or are in the models that, that we use to calculate inflation. So, you know, they’re, they’re just parts. You can ask about anything like that, and they are. They have a place, the staff has a place where they’re looking at that and pricing in, what will happen with higher prices and that kind of thing. So it’s there. The effects are not that big yet. You know, we’re a huge economy. The import sector is only 10% of the economy. So we’re not like a European country where 50% of the external—of GDP—is in the external sector. We’re also, you know, as I mentioned, we’re an oil exporter. So we’re not feeling the same kind of pain and we’re not likely to feel the same kind of pain that economies in Western Europe and certainly in Asia are feeling.

What Powell conflated in his word salad answers was nominal vs. real spending. Even looking at just energy goods and services, while in Powell’s world people are “still spending”—meaning they are spending more money on energy—in the real world they are buying less energy.

As consumers know only too well, inflation means you pay more but consume less.

Will the exposure of Southeast Asian manufacturers to energy price and supply shocks have a secondary effect on the US economy? That is a very real possibility. With regards to China it may even be a probability, as the data shows that China is already being hit hard with multiple materials pricing shocks across the whole of its manufacturing sector.

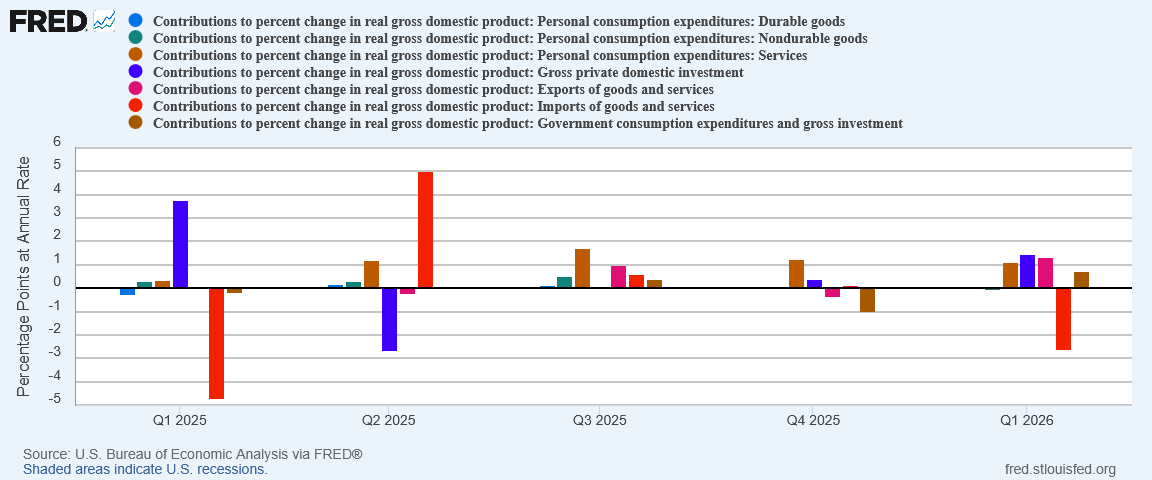

Arguably, we are already seeing the consequence of Asian producers passing on increased costs to American consumers, as imports were an outsized drag on GDP for the first quarter.

Imports are treated as a reduction in GDP, so an increase in imports—specifically, an increase in the dollar value of those imports—is a decrease in GDP.

Did higher producer prices push the dollar value of imports up in March? The broad GDP data does not let us answer that question definitively, but it is a question, and one that is likely to gain considerable relevance for April and beyond.

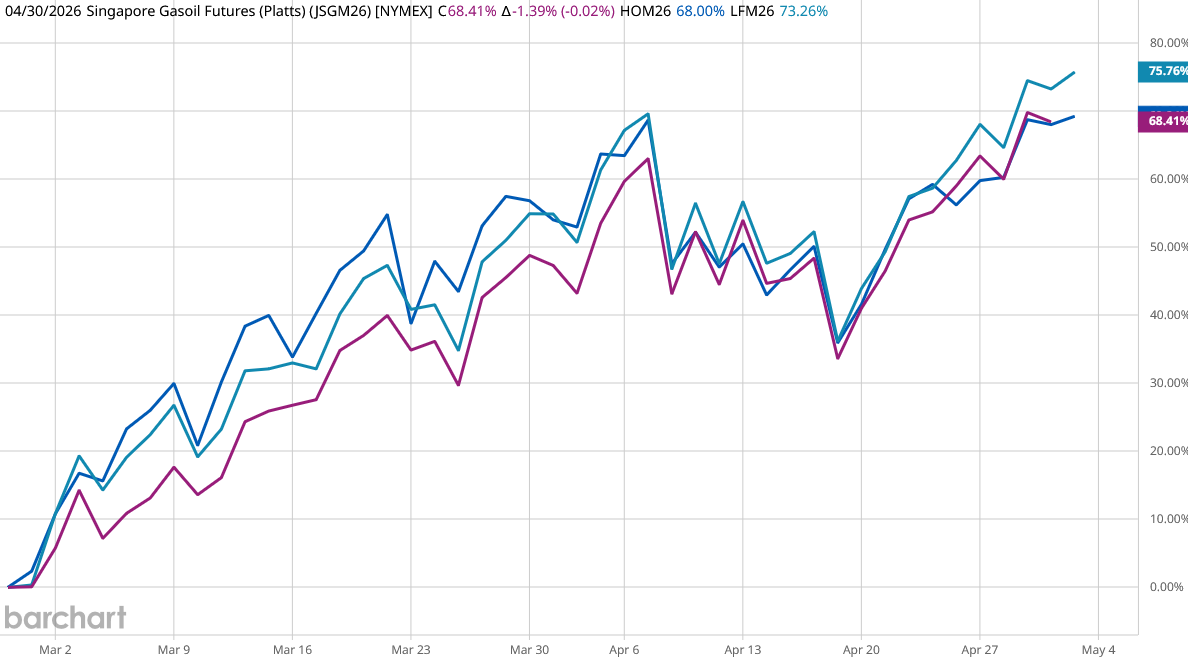

Powell did get one thing right: The US is better positioned than other countries to grapple with energy price shocks. We can see evidence of that just in the movements of diesel prices in Europe, Asia, and the United States.

Energy prices are up everywhere, but they are up more particularly in Europe.

Will importers pass along higher prices? Given the magnitude of price increase for a number of inputs, as well as for transportation both of people and cargo, we must assume that, unless oil prices return quickly to pre-war levels, all importers eventually will pass along at least some of their cost increases.

As we’ve seen just with energy goods and services, when prices are passed along, part of the consumer response is to buy less.

Stagflation A Rising Risk

While Jay Powell dismisses the potentials for a stagflation crisis within the US economy, the data has shown there have been significant potentials, needing only an inflationary shock to activate them.

Stagflation has quickly become a global concern in the wake of Iran’s closure of the Strait of Hormuz.

The war in the Middle East will likely affect the global economy and the United States, whether it continues for a short or long term, because of disruptions in the oil market that could trigger inflation and spur a recession, warn experts, economists and the International Monetary Fund.

Widespread stagflation could be the result of the war because of the long-term closure of the Strait of Hormuz, said Mohammad N. Elahee, a professor of international business at Quinnipiac University in Hamden, Connecticut.

It quite likely is a present crisis in China.

At present, the impacts to the United States from the closure of the Strait of Hormuz are still mostly limited to energy prices. We do not see significant price rises from non-energy goods and services—yet.

That word “yet” is going to be the watchword for how inflation and the overall economy evolve over the next few months. Whatever impacts we do not see right now, we may very well see next month or the month after.

Because we do not see all the impacts just yet, we should be cautious about assuming there will be no impacts, or less impact. We should be equally cautious about assuming the impacts will simply be price rises.

Proper understanding of the data in light of the war with Iran hinges on remembering that the stagflation phenomenon occurs when sudden price shocks collide with weak economic growth. Because price shocks are driven by the supply side rather than the demand side, the resulting inflation compels reduced consumption and economic contraction to bring supply and demand back into approximate equilibrium. When inflation is driven by demand side pressures, the result is constrained consumption and economic restraint.

If we see job markets soften, if real personal expenditures for any goods and services decline, we are entering the beginning stages of a stagflation crisis.

Will we enter those beginning stages? We won’t know the answer to that until it happens. That much of my assessment of the February PCE data remains very much on the table:

If the war with Iran continues to drag on, and especially if the recently and still quite fragile ceasefire fails to hold, we might see inflation and unemployment combinations that look distressingly stagflationary. The inflation data from both January and February leave that possibility very much on the table.

The key word in that assessment, of course, is “if”.

The March Personal Income and Outlays report confirmed what we saw in the March Consumer Price Index report: we have energy price inflation and lots of it. We do not have much inflation in other parts of the economy right now.

We are going to see elevated energy prices again in April. How much we see either inflationary impacts or stagflationary impacts beyond energy prices remains to be seen.

Beyond energy price inflation, the fog of war still surrounds the economics of wartime.

Peter, You can see the rise in the gas pumps weekly and sometimes sooner than that. And not to put a damper on your article, but the FRED chart shows 9 months of increases to 6 months of decreases and the increases make substantially higher percentage moves than the decreases. Sometimes 3X as much. It will take several months of continued decreases to even get close to what we were paying on food. I'll wait and see what the next couple of months bring, Thanks for keeping us informed.

Food prices are in deflation - excellent! My guess is that Wall Street has been dealing fairly well with the war situation because, aside from energy prices, things aren’t as bad as some feared. Once the war ends, energy prices will drop. The effects of several of Trump’s policies - such as domestic job growth resulting from tariffs - will start to manifest.

Peter, you’ve shown us that stagflation is a worrisome possibility. If gas prices drop by, say, a dollar per gallon, do you still see enough job-market softness, etc. for stagflation to occur?