Anyone expecting the Consumer Price Index Summary Report to deliver a strong confirmation that the US economy is in overall good health was disappointed yesterday, as the CPI printed hotter than expected both in the year on year change and the month on month change.

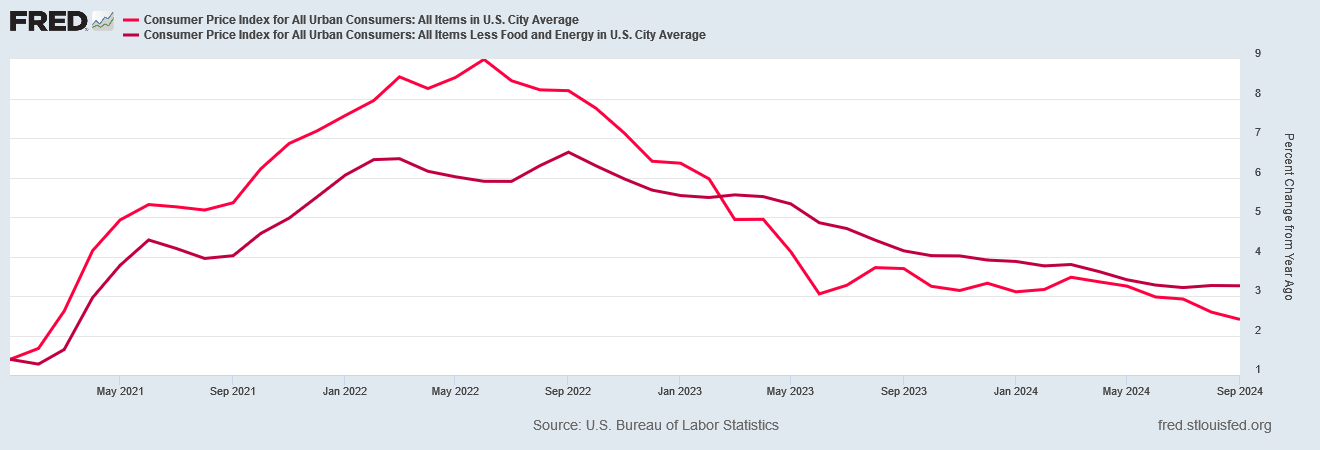

The Consumer Price Index rose 2.4% versus a year ago in September — above the 2.3% increase economists had expected, the Labor Department said on Thursday.

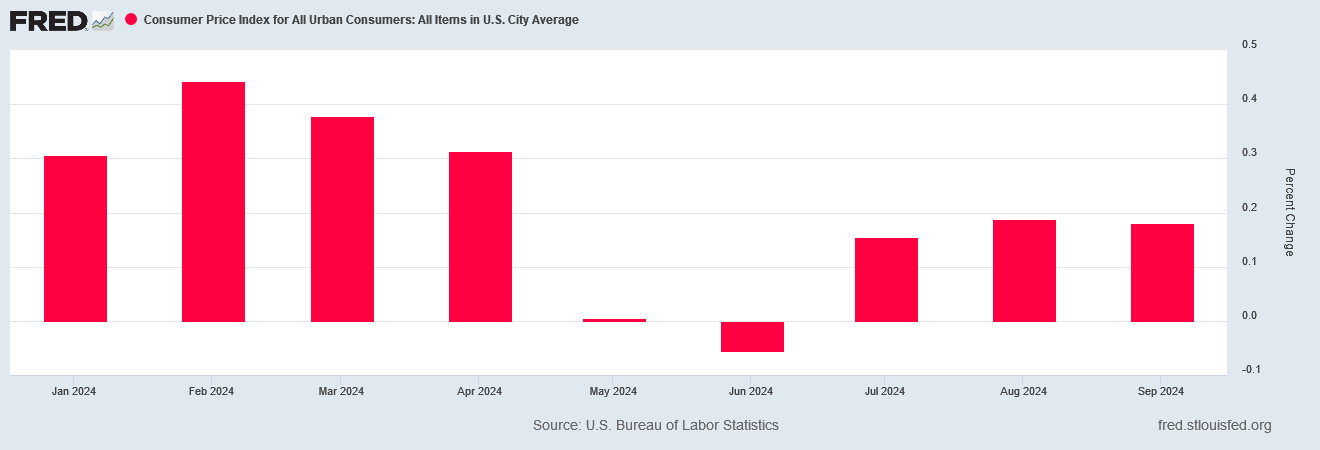

Month-over-month, the CPI rose 0.2% — steeper than the 0.1% increase economists had expected but even with the 0.2% number from August.

“Core” inflation — a metric closely watched by economists that excludes the volatile costs of food and energy, rose 3.3% versus a year ago, also ahead of economists’ prediction for a 3.2% year-over-year increase.

Corporate media will, of course, only very reluctantly admit what consumers know just by inflation’s impact on the average wallet: consumer price inflation is heating up again, and in many respects has never actually left.

All Facts Matter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

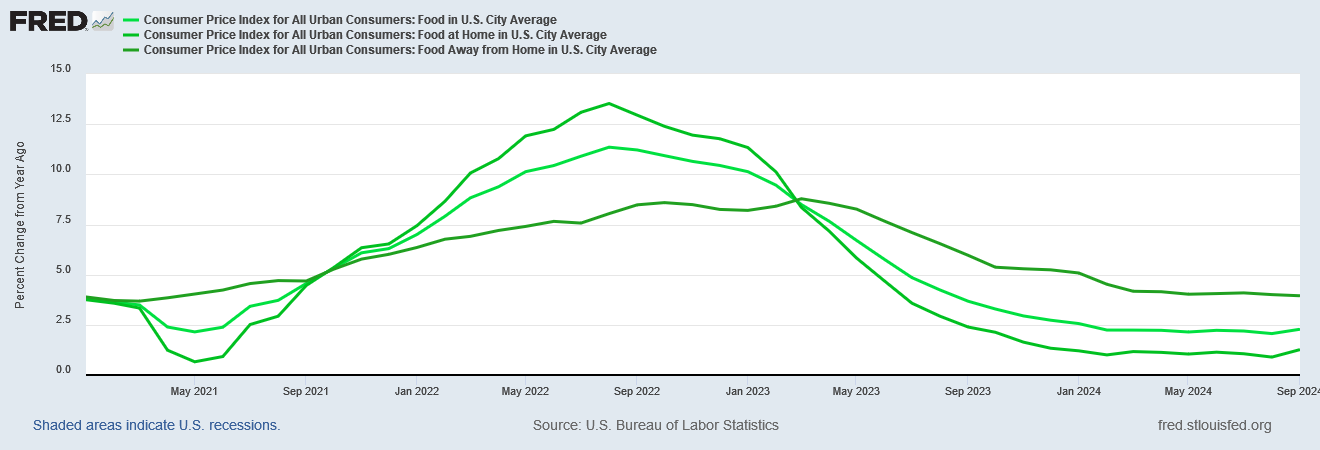

The all items index rose 2.4 percent for the 12 months ending September, the smallest 12-month increase since February 2021. The all items less food and energy index rose 3.3 percent over the last 12 months. The energy index decreased 6.8 percent for the 12 months ending September. The food index increased 2.3 percent over the last year.

Certainly having the lowest year on year rise in prices is a sign things are moving in the right direction…doesn’t it?

That the energy price subindex retreated 1.8% for the month is a testament to how steep the initial price retreat at the beginning of September was. We must remember that crude oil prices have been rising since approximately September 10—yet indeed crude oil prices did fall over the full month span around 1.8%.

While the retail gas prices are more volatile than the weekly averages maintained by the US Energy Information Administration, that data also shows gas prices levelling off in the last half of the month.

However, the most significant aspect of the clear deflationary signals for energy prices we saw in September (and which, we should note, we are not likely to see in October), is that, for all of this downward price pressure, energy’s overall impact on the headline consumer price inflation metric was fairly muted.

A significant decrease in energy prices that fails to produce significant disinflation at least at the headline consumer price level can only mean that core inflation and/or food price inflation is heating up, and upward price pressures there are countering the previously influential downward pressures from energy prices.

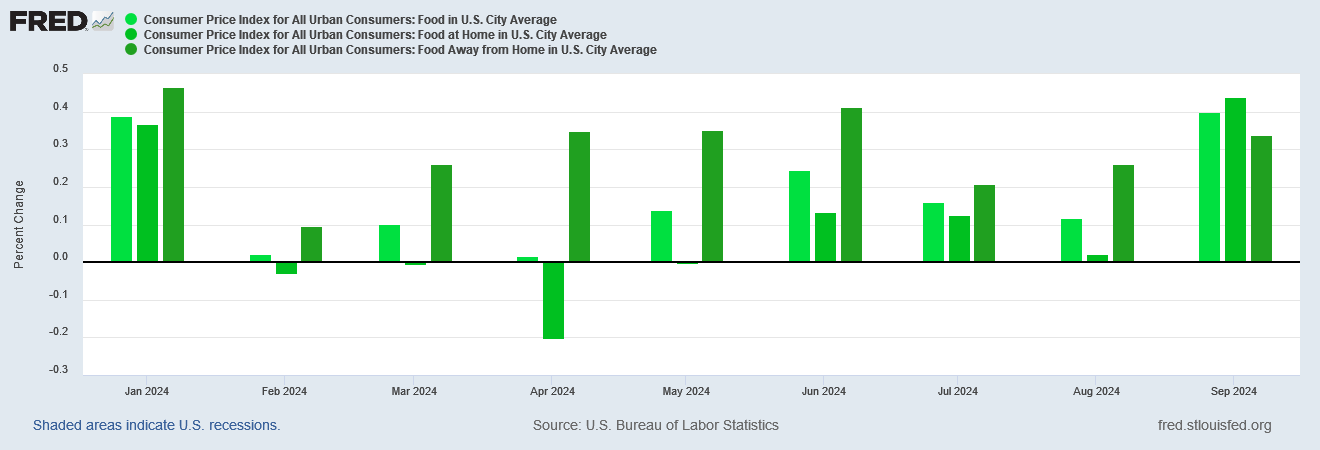

Indeed, when we look at food prices we see that food price inflation is heading up again.

Perhaps even more disconcerting is that food prices for foods prepared at home printed the largest month on month increase. Also, the increase was sufficient to push up the year on year inflation measure as well.

But the resurgence in inflation is not limited to food prices. Core inflation—consumer price inflation less food and energy prices—also heated up month on month.

Core inflation has been printing hotter since June, and is now reaching a level where its upward price pressures are starting to overpower the previously domineering influence of energy prices.

Within that core inflation metric, the upward price pressures in September come from both sides—both goods and services saw inflation heating up. Durable goods in particular jumped in September, flipping from deflation of 0.4% month on month in August to 1% in September.

It is a testament to the dogged insistence of corporate media about sticking to their preferred narratives that the “consensus” forecasts of what the inflation metrics would be for September were overly optimistic across the board. Seemingly every economist polled by corporate media expected the inflation metrics to be a good 0.1% lower than they were.

Yet the signals have been there. Service price inflation in particular has been readily apparent to any who cared to peel back the data layers to look at what lies underneath.

Year on year, service prices have been rising between 3.7% and 4.2% since the beginning of the 2024, even as goods prices have been falling as much as 1% year on year during that same period.

While the “experts” might have been caught off guard by the hotter-than-expected inflation print, that is merely a testament to how little research they are doing before making their pronouncements. They are not assessing the trends underneath.

What is the ultimate takeaway from the September Consumer Price Index Summary report? That inflation is heating up in earnest, and with energy price inflation returning in a major way for October, consumer price inflation at all levels is also likely to return. Inflation never really left for services, and only partially for food, but as energy prices move higher, and as they push production costs higher, there will be increasing upward price pressures throughout the consumer price index and an acceleration in the inflation metrics.

The downward price pressures that have produced the disinflationary trends we have seen since the end of hyperinflation in late 2022 are by now largely a spent force. We are at or very close to the bottom of the disinflation/deflation trend. Once that bottom is reached—assuming it has not already been reached—prices will move in only one direction: up.

Resurgent inflation is what lies on the other side of that bottom. Resurgent inflation is what we are likely to see starting this month, and running at least through the end of the year.

Jay Powell will not be happy with resurgent inflation. Consumers especially will not be happy with resurgent inflation. Christmas shopping is going to get more expensive for everyone.

Corporate media needs to say the quiet part out loud: headline consumer price inflation is returning. Consumers would do well to realize that what is driving that headline consumer price inflation is the goods and services inflation that, ultimately, never really left.

All Facts Matter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

My decent olive oil that was 9.98 last year is now $18.00. At Walmart. A small basket of our usual purchases went from $20.00 or such to $45.00 or more. This is at my granular level of spending. Airline tickets to a family member we always take are now double or more. If we go 7 miles we can get gas in Wisconsin for 40 to 60 cents cheaper a gallon. (Taxes less). We are relieved we are not raising a family now. My grandsons college fees are eye watering. A state university. That’s on the parents. Hopefully his degree (if he finishes) will support him but I doubt it.

I really believe this is the plan. The FED likes inflation. Prices can’t go down because the economy is too dependent on high prices, right? But you’re way smarter than me so please tell us what would happen if prices for food and housing and energy were to drop substantially. Isn’t this the new normal and wages just have to catch up ?

My decent olive oil that was 9.98 last year is now $18.00. At Walmart. A small basket of our usual purchases went from $20.00 or such to $45.00 or more. This is at my granular level of spending. Airline tickets to a family member we always take are now double or more. If we go 7 miles we can get gas in Wisconsin for 40 to 60 cents cheaper a gallon. (Taxes less). We are relieved we are not raising a family now. My grandsons college fees are eye watering. A state university. That’s on the parents. Hopefully his degree (if he finishes) will support him but I doubt it.

I really believe this is the plan. The FED likes inflation. Prices can’t go down because the economy is too dependent on high prices, right? But you’re way smarter than me so please tell us what would happen if prices for food and housing and energy were to drop substantially. Isn’t this the new normal and wages just have to catch up ?