My one hard and fast rule when it comes to analyzing events is simply this: always follow the data. Never assume the narrative is correct or complete, but always realize that the facts will always be the facts. When the narrative does not reconcile with the facts, rely on the facts and adjust the narrative accordingly.

Like so many of the world’s “experts” these days, Federal Reserve Chairman Jay Powell does not share a similar respect for the facts, preferring the narrative above all else. How else to explain his dogged insistence that the US economy is strong while simultaneously arguing that the US economy must be fixed as justification for hiking interest rates in an effort to combat inflation?

This paradoxical rationale was present in his Jackson Hole speech last month:

The U.S. economy is clearly slowing from the historically high growth rates of 2021, which reflected the reopening of the economy following the pandemic recession. While the latest economic data have been mixed, in my view our economy continues to show strong underlying momentum. The labor market is particularly strong, but it is clearly out of balance, with demand for workers substantially exceeding the supply of available workers. Inflation is running well above 2 percent, and high inflation has continued to spread through the economy. While the lower inflation readings for July are welcome, a single month's improvement falls far short of what the Committee will need to see before we are confident that inflation is moving down.

This paradoxical rationale was present in Jay Powell’s interview last week at the Cato Institute:

“We think we can avoid the very high social costs that Paul Volcker and the Fed had to bring into play to get inflation back down,” Powell said in an interview at the Cato Institute, referring to the Fed chair in the early 1980s who sent short-term borrowing rates to roughly 19% to throttle punishingly high inflation.

Against the “economy is strong” narrative, however, stand a few data points in stark contradiction:

“Core” consumer price inflation (CPI inflation less food and energy) rose to 6.3% Year on Year in August.

Labor force participation declined in August before seasonal adjustments showed an increase.

Retailers are experiencing recession-like accumulations of inventory, despite strong nominal sales gains.

At a minimum, the “economy is strong” narrative needs a bit of nuance to explain these divergent data points. At a maximum, the “economy is strong” is simply wrong and needs to be discarded.

Can data tell us which one it is?

Retail Sales Stagnating

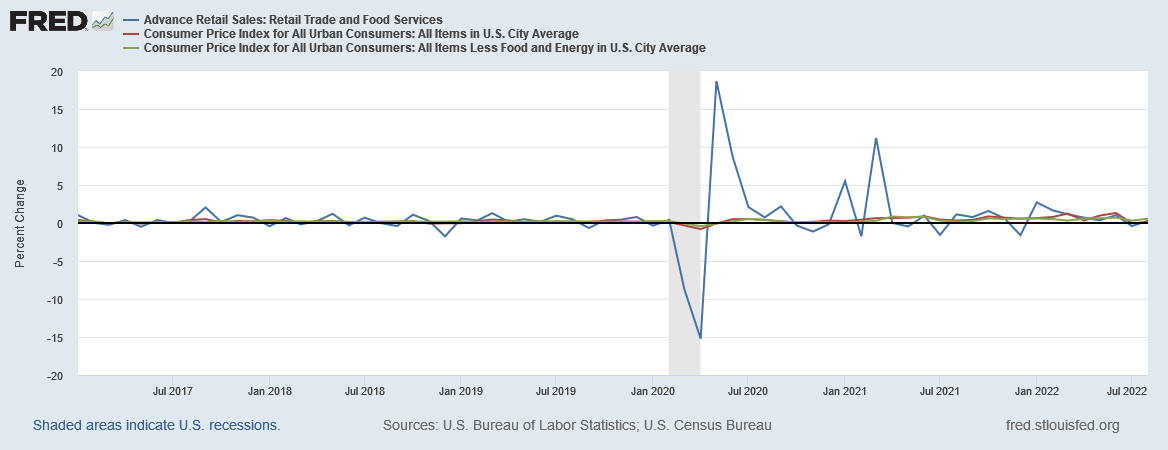

One data set that at first glance appears to suggest strength within the US economy is retail sales. Not only are they rising, but they appear to be rising at a faster rate than before the 2020 lockdowns.

However, the retail sales data is gathered in nominal current-dollar terms. Inflation has not been incorporated into the data. When we look at the percentage year-on-year growth in retail sales, and overlay year-on-year inflation percentages, we see a completely different perspective on the data.

Prior to 2020, retail sales largely kept pace with inflation. During the 2020 lockdown-induced recession, retail sales dropped significantly, and during 2021 retail sales grew at a rate greater than that of inflation. However, that growth ended earlier this year, and now retail sales are once again back to just keeping pace with inflation.

This trend is confirmed when we look at the month-on-month percentage change in retail sales, and overlay monthly consumer price inflation numbers.

After an initial post-recession surge, retail sales in the US have largely kept pace with inflation and that’s it.

Keeping pace with inflation is a break-even position. Retail sales has had strong periods since the 2020 lockdowns, but overall the sector has been going sideways in real terms—it is stagnating, not growing.

Labor Markets Have Been Turning Toxic For Years

Perhaps the hardest data to assess fully is the labor data generated by the Bureau of Labor Statistics. This is due in no small part to the chicanery and fudging of the numbers that goes on within the BLS when they publish their monthly Employment Situation reports—what I have come to call Lou Costello Labor Math.

However, when we look at the broad demographic numbers surrounding employment, a few key trends do appear that speak directly to the notion of economic strength vs weakness.

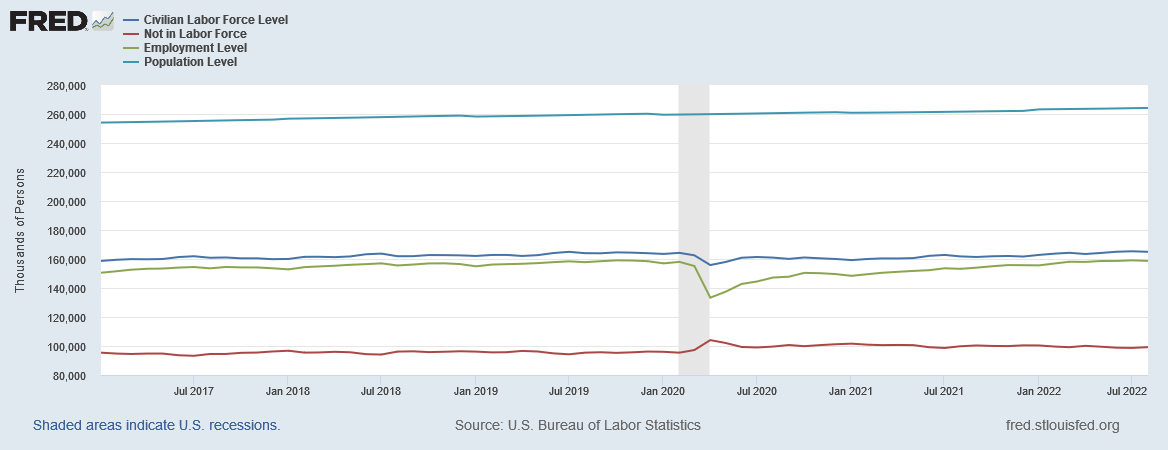

One thing that shows up is the consistency of the size of the labor force and even of those not in the labor force.

We also see something that lends support to the notion of labor markets as “tight”—the thinning gap between the civilian labor force overall and the number of people actually employed in this country. That gap has narrowed considerably since the aftermath of the 2020 recession.

However, what has also not changed much overall has been the number of people not in the labor force.

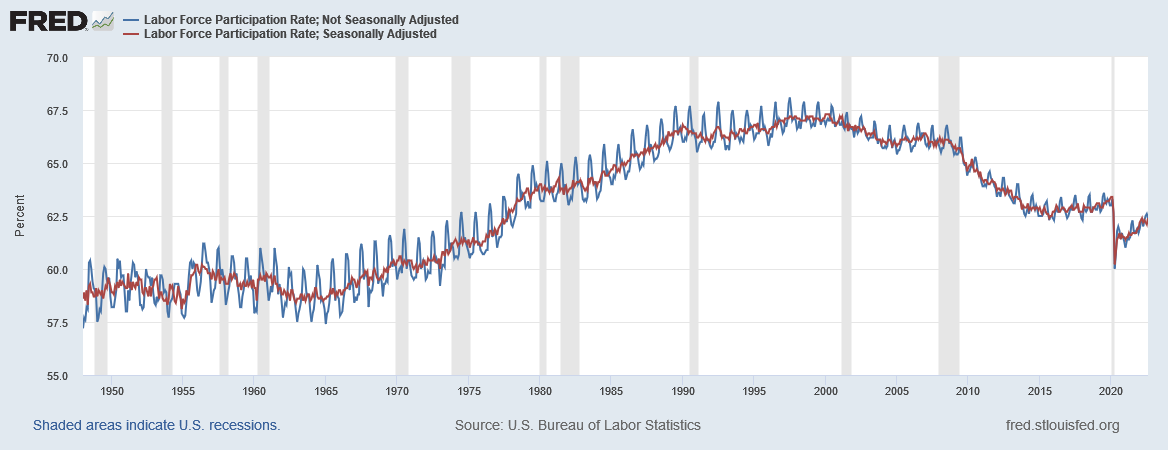

This is an important cautionary, because we do well to remember what the historical levels of labor force participation were even when the economy was “booming”—throughout the postwar period, labor force participation has never exceeded 67.5%.

While labor force participation rates are well below the 67.5% peak of the mid 1990s, the data does show them to be rising again after the lockdown/recession dislocation.

However, when we index the labor force, those not in the labor force, those who are employed, and the entire civilian non-institutional population, and compare their growth trends, we begin to see how job growth has taken place over time in this country.

If we index these demographics to 1975 (the earliest year those not in the labor force were recorded), we see that the labor force and employment grew at a faster rate than the overall population, while those not in the labor force grew at a slower rate.

It’s also worth noting that over this same long time frame employment grew faster than the overall labor force up until the 2007-2009 recession. Employment growth slowed down and those not in the labor force began growing faster.

If we index these same demographics to the start of that recession, the growth rates are reversed: those not in the labor force are growing faster than the overall population, while the labor force and employed demographics are growing slower.

This is consistent with the declining labor force participation rates that have been the broad demographic norm since the 2007-2009 recession.

As these indexed trends illustrate, even though the unemployment numbers are low, they are low only because most who are in the labor force are employed, not most of the overall population. What that focus misses is that the number of employed as a percentage of the overall population dropped after the 2007-2009 recession and again after the 2020 pandemic recession.

The employment-population ration is even today a full percentage point lower than it was in February 2020, right before the lockdowns and the recession.

Unhealthy Trends

These are not healthy trends. When retail sales only keep pace with inflation people are not gaining wealth or increasing their overall prosperity. At most they are breaking even. Aside from recovery-induce retail sales growth after the 2020 lockdowns and recession, retail sales have been essentially stagnant. This is definitely not a sign of a strong economy.

When the labor force and employment demographics grow slower than the overall population, productivity gains overall become far more difficult to achieve, if not impossible. Declining labor force participation, and even decelerating labor force growth in the face of accelerating growth for those not in the labor force, means an increasing proportion of the population is not gainfully employed. This is not a sign of a strong economy, but an increasingly sclerotic and sickly one.

Only when one looks at narrowly defined numbers does the US economy appear to be healthy. However, an economy—much like a human body—has to be healthy throughout, not just in select areas. Labor force participation needs to be increasing, not decreasing, while retail sales need to do more than just keep pace with inflation. These things are not happening in the US.

Jay Powell and the government economic “experts” seem oblivious to the reality of these unhealthy trends in the economy. They are willingly confining their attention to narrow statistics that paint the rosiest picture possible, and are ignoring the broader trends that are far less optimistic.

To fully understand the state of the economy, however, one has to follow all the data. One has to look at all the trends, not just the ones that show good news. The US economy is not completely decrepit, but it is absolutely not the strong vibrant engine of growth and prosperity the “experts” have claimed it to be repeatedly.

Always follow the data. If you’re Jay Powell, start following the data.

Well said, an extremely clear explanation!

The news from the CEO of Federal Express should rattle even Jay Powell.