I focus quite a bit on employment numbers. This is not a coincidence. I view jobs—and whether there is real job growth—as foundational to this nation’s economic well being. It is my studied opinion that we cannot be prosperous as a nation if we are not putting people to work, if we are not growing the demand for labor.

But there is more to economic data than just jobs numbers, and more to economic growth than just employment. There is consumption. There are measures of industrial production without regard to employment. There are measures of industrial capacity utilization.

It is intuitively obvious that rising retail sales—rising consumption—is a sign the economy is expanding.

It is equally intuitively obvious that rising industrial production is a positive sign. To borrow from the late H. Ross Perot, we need to be making more “things”.

For the same reason, we are doing better the more of the nation’s industrial capacity is being put to work.

With the political primaries largely over and done, and the several states heading into the general election in November, it is worthwhile to look beyond jobs and prices, to gauge how the broader health of the US economy, which is sure to be part of the political debate as the fall election season heats up.

With the US also moving from war to a problematic peace with Iran, the next few months could easily prove to be a pivotal time for the US economy. Assessing the state of the US economy now might be helpful in assessing how well the US moves forward now that the war with Iran is arguably over.

It is particularly worthwhile at the moment, because the data shows the economy is doing fairly well. The data leans into the job growth narrative from the May Employment Situation Summary and tells us that the job growth in May was more real than not.

PMI Data Shows Growth Trend

The most positive notes come from the independent Purchasing Managers Index1, or PMI, surveys.

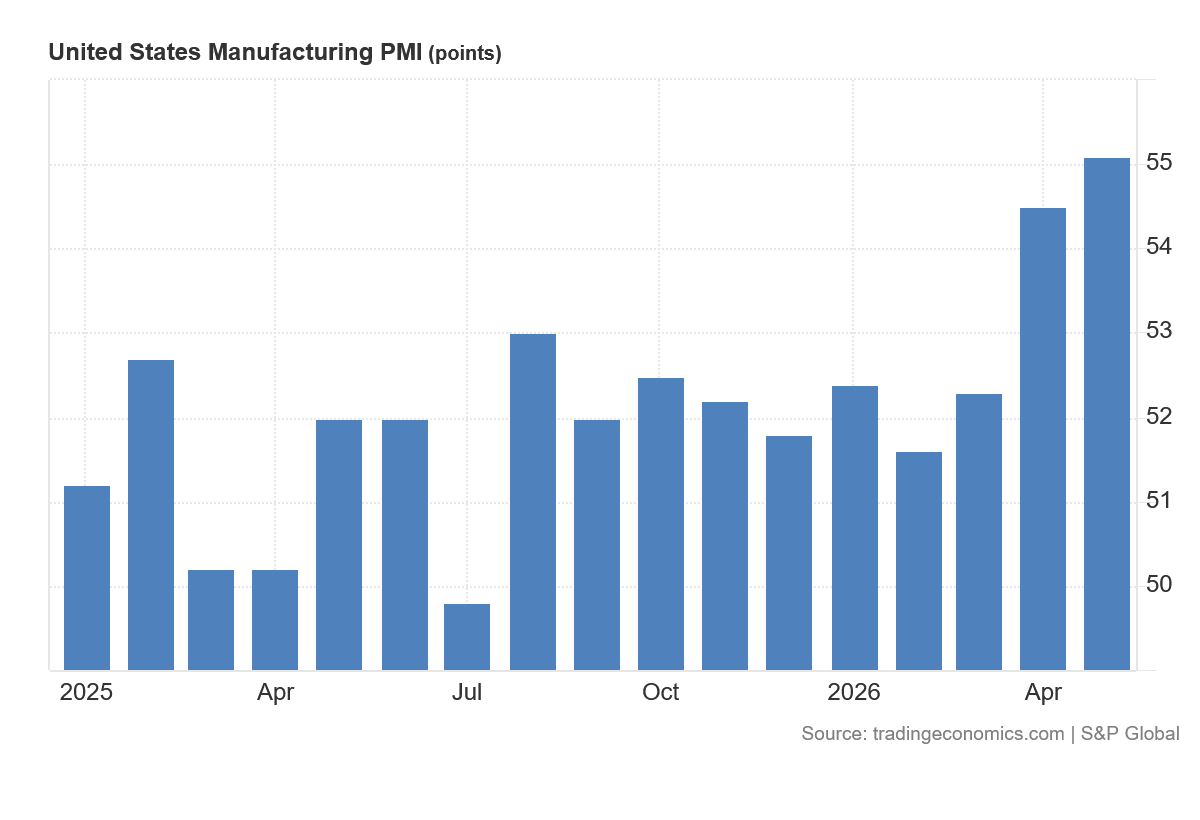

The May Manufacturing PMI from S&P Global is the third consecutive month of increasing expansion.

Not only does the PMI data show manufacturing concerns in this country to be expanding, the amount of that expansion is increasing.

An important caveat: we must be cautious with the PMI data. At the end of the analysis the PMI data is an industry survey, and therefore all the possibilities for error we see within BLS data on jobs can happen with the PMI data. Always take PMI stats with a grain of salt.

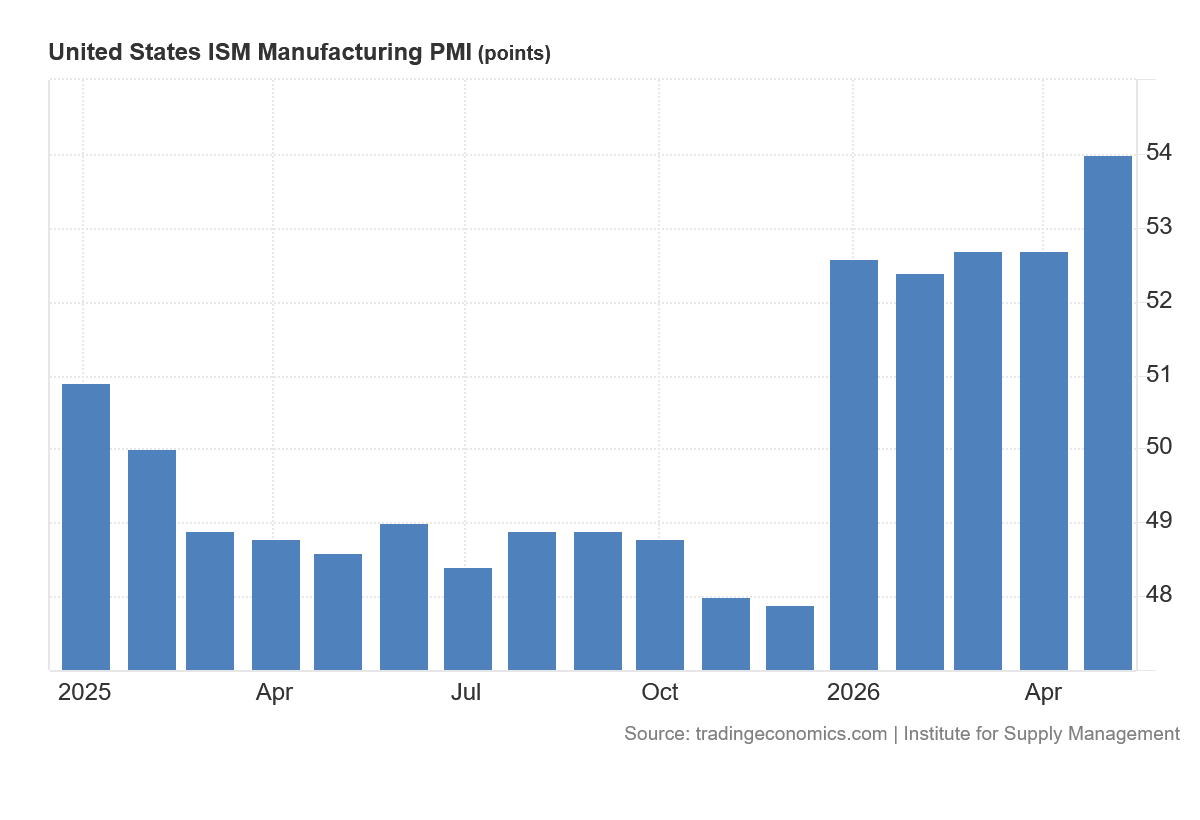

However, the Institute for Supply Management maintains its own PMI data and conducts its own surveys. When the ISM PMI data shows the same trend as S&P Global, that is a confirmation we should not be quick to overlook.

What both manufacturing PMI data sets show is that, beginning in January, US economic activity has been expanding.

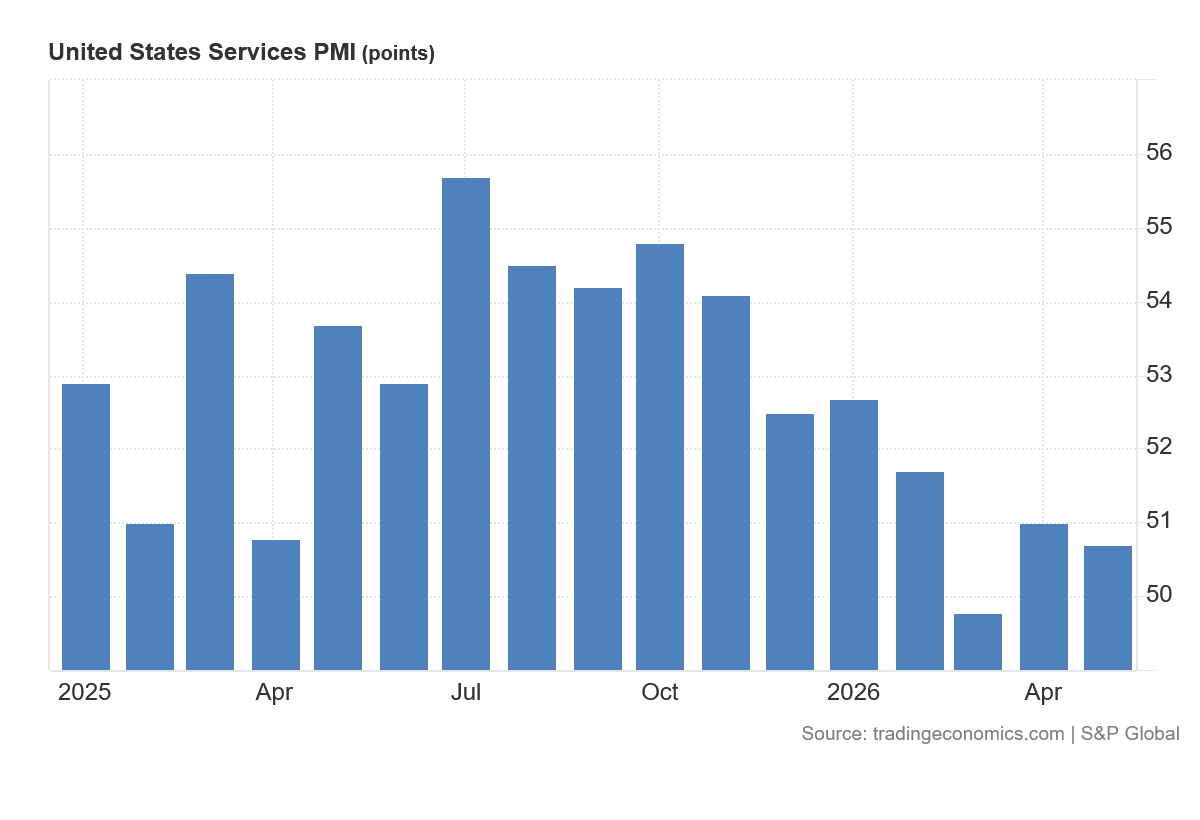

The S&P Global services PMI data for May showed expansion, but also indicated the growth was potentially fragile and not at all assured.

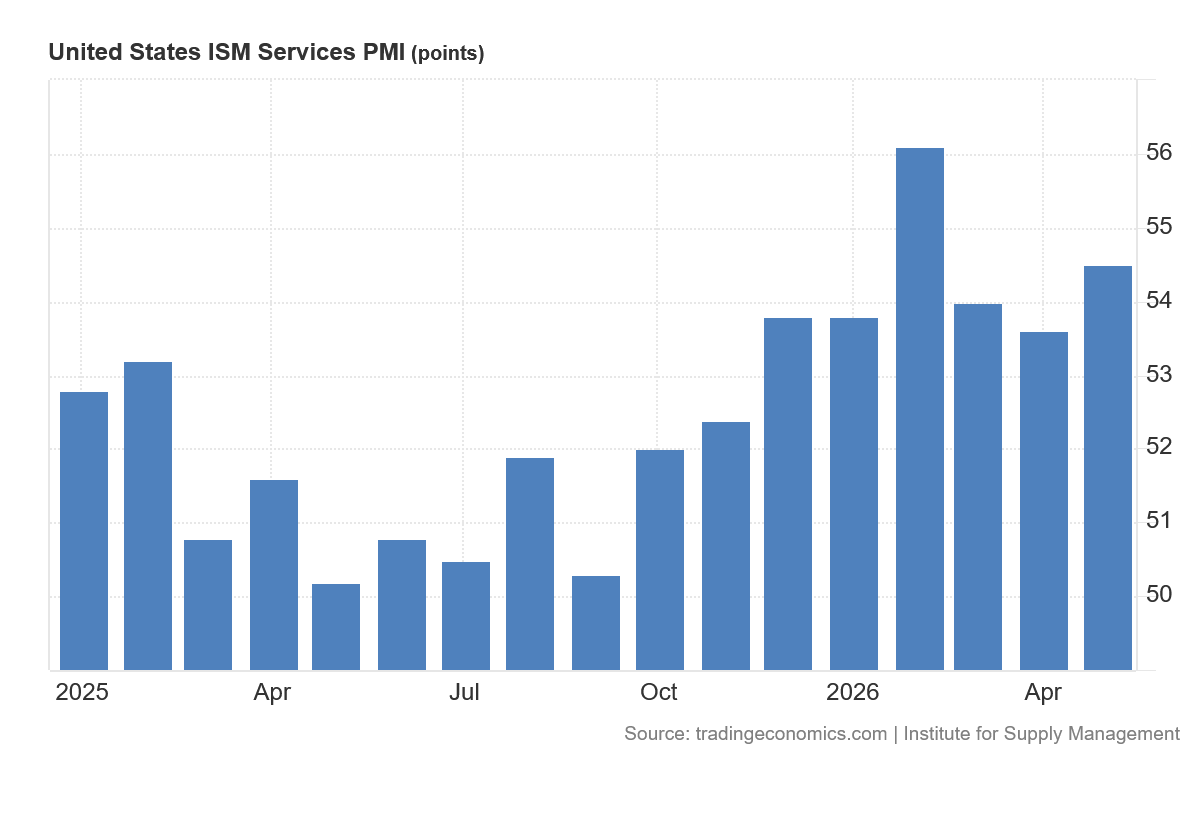

The ISM Services PMI data for May shows a stronger expansion, one that goes back potentially back to before the start of Donald Trump’s second term in the Oval Office.

The S&P Global and ISM surveys are conducted independent of each other. While as surveys we need to be cautious about how much significance to place on them, that both survey sets show expansion for both manufacturing and service industries makes the data difficult to dismiss.

The PMI data across the board shows the US economy is expanding right now.

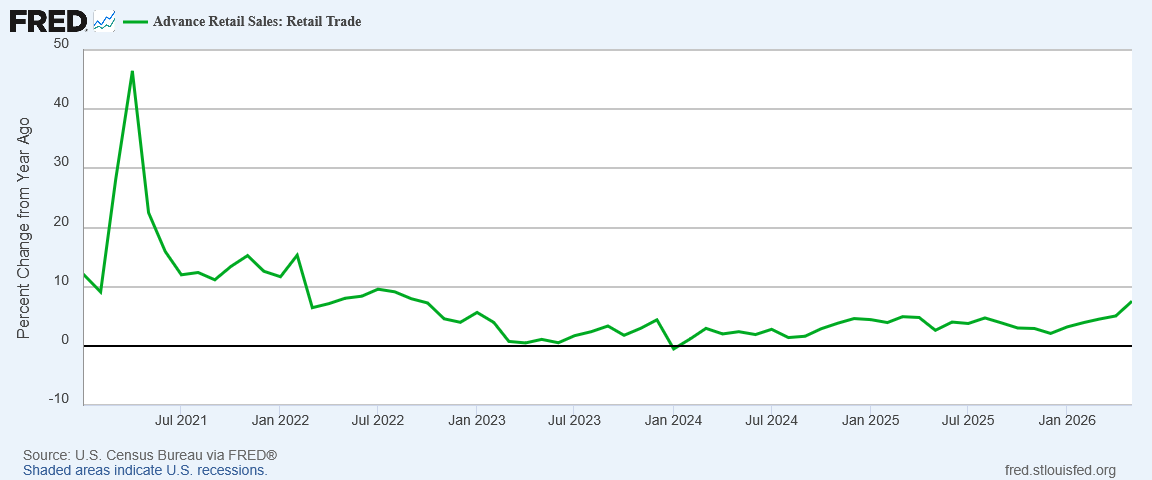

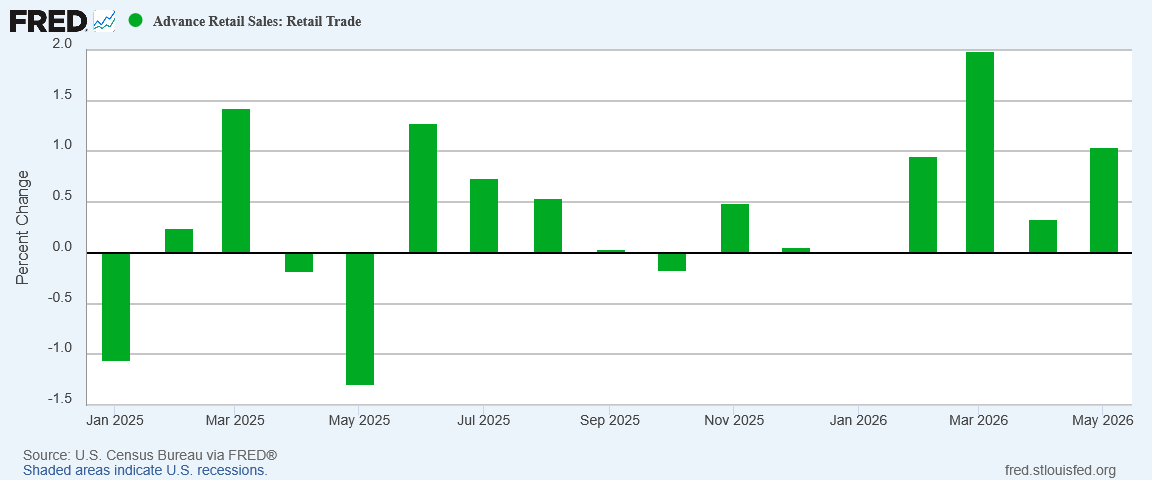

Retail Sales Are Increasing

The U.S. Census Bureau gives another positive growth signal with its measurements of retail sales.

As of May, 2026, the Advanced Retail Sales estimate shows year on year sales growth of 7.5%.

Month on Month, Advanced Retail Sales grew by 1% in May.

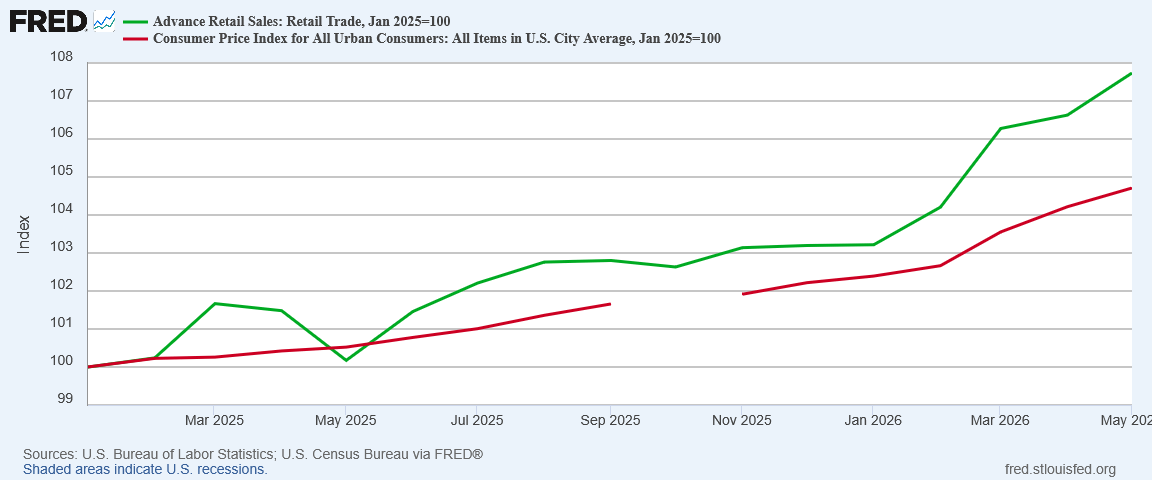

More importantly, retail sales—which are measured in nominal dollars—are growing faster than the Consumer Price Index. Sales growth is greater than inflation, which means there is real growth in consumption.

Consumption—by far the largest component of the US economy—is demonstrably robust, and has been almost since the start of President Trump’s second term.

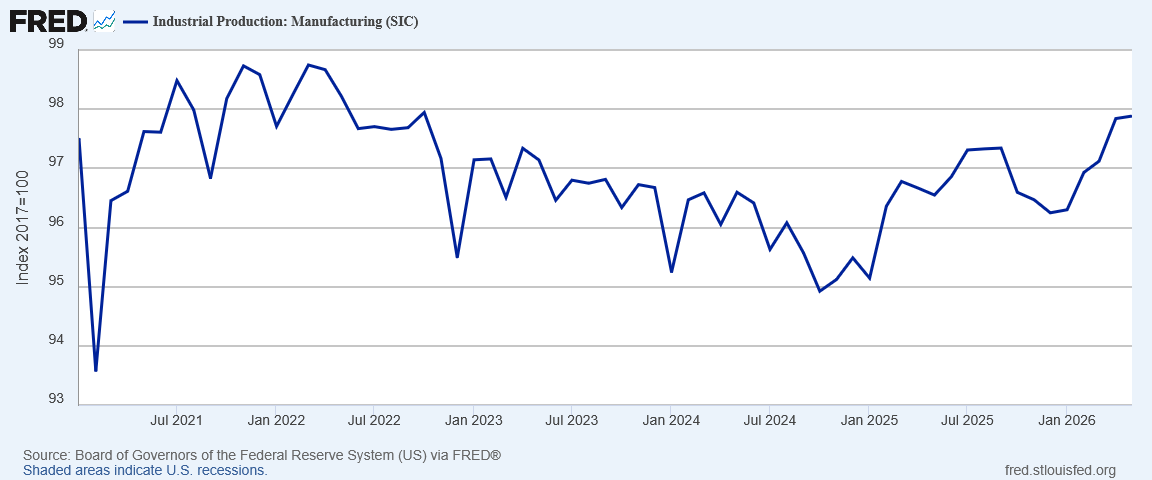

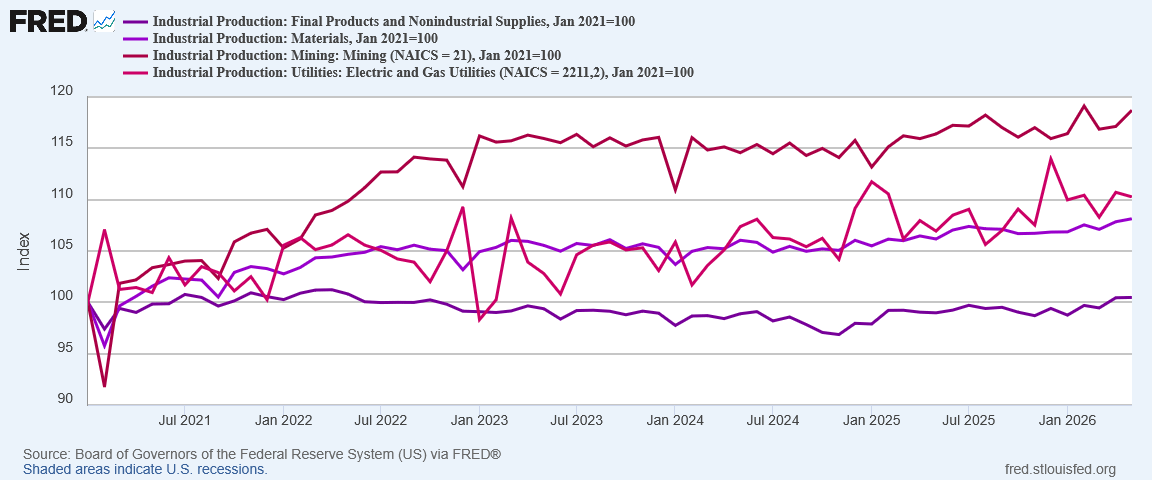

Industrial Production Is Increasing

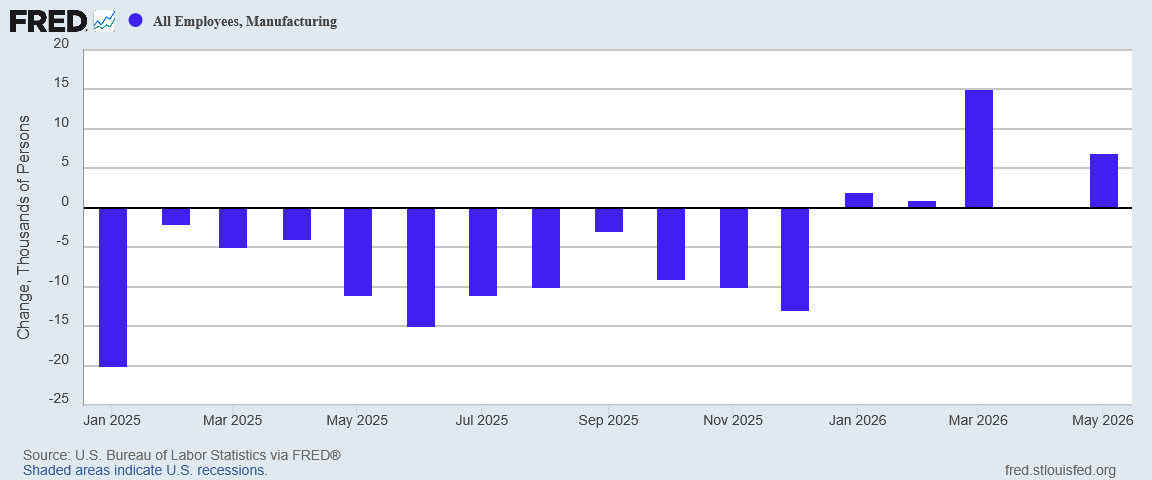

America’s performance in manufacturing is an especially important consideration. Not only do manufacturing jobs generally command higher wages than most service jobs, but a major campaign promise made by President Trump in 2024 was to turn the United States into a “manufacturing superpower”.

Overall, industrial production has been strengthening in this country since Donald Trump took office at the start of 2025.

Even sectors that started out well under Joe Biden have been picking up under President Trump.

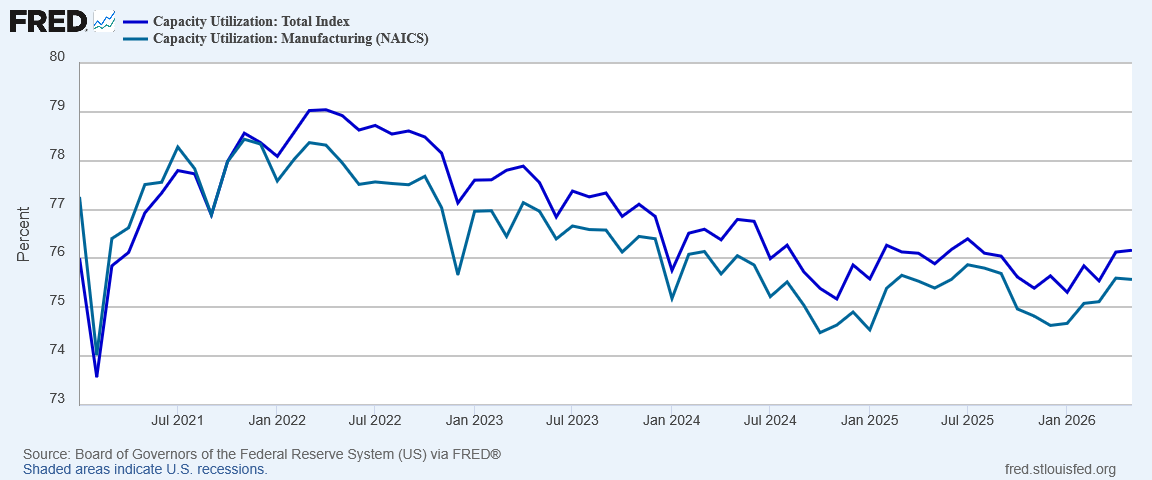

Additionally, US capacity utilization has been increasing steadily under Donald Trump, which is a clear reversal from the long decline under Joe Biden.

These growth metrics, assessed independently of manufacturing jobs, resonate well with the manufacturing sector’s recent return to job growth.

When we see independent data sets supporting the same broad narrative, we necessarily have greater confidence in that narrative. With industrial production growth, capacity utilization growth, and finally manufacturing job growth, a narrative that the manufacturing sectors of the US economy are growing is difficult to refute.

America is making more things, and America is putting more people to work making more things. These are exactly the sort of economic outcomes we need to see if Donald Trump’s pledge to make the US a “manufacturing superpower” is to be realized.

At the moment, the data says Donald Trump’s pledge is being realized.

Staving off Stagflation?

The economic growth outlook has taken on added importance because of the war with Iran, and Iran’s subsequent illegal closure of the Strait of Hormuz, slapping an oil price and supply shock on the world’s economies by effectively bottling up 20% of total global oil supply.

When the war had largely turned into an attritional stalemate over the Strait, with Iran blocking oil shipments from its Arab neighbors and the US blockading Iranian shipping in return, the prevailing assessments indicated that the situation was sending the worlds’ economies into a stagflation crisis, as the sudden loss of global oil supply was setting the stage for global demand destruction.

We do well to remember that signature aspect of supply shocks and the stagflation they can produce. When physical supply is abruptly diminished, physical demand must also be diminished to restore overall economic equilibrium. If the physical supply of widgets goes from 100 down to 80, the physical demand for widgets must also go down to 80, for the simple reason that 80 widgets are all that is available. There cannot be any demand for goods (or quantities) which do not exist.

When an economy is already in the doldrums, such as when job growth is weak or when overall economic growth is weak, a supply shock is particularly thorny, as the demand destruction will push a moribund economy into outright recession.

When Operation Epic Fury began, then-Fed Chair Jay Powell was dismissive of stagflation concerns, when the data clearly showed there was significant risk of stagflation emerging from the Strait of Hormuz closure.

No, we are not seeing stagflation at present, except in the most incremental and technical fashion. The oppositional forces are present and discernible, but they are not (yet) at a 1970s level of severity.

We are, however, seeing several indicators that a stagflation scenario is a real risk to the economy. A significant inflation shock coupled with the soft labor markets the United States has endured for the past few years could very easily translate into a stagflation scenario.

What has changed since then for the US economy has been the transition from jobs recession to jobs recovery. With multiple consecutive months of robust job growth as of the most recent Employment Situation Summary report, the US economy is in a stronger position now than it was just a few months ago.

A broader sweep of economic data indicates that economic strength has some depth to it. The stronger and more robust the US economy is, the better it will be able to withstand the pricing pressures which will linger for a time from the oil shock.

We are already seeing some indication of the benefits of a stronger economy. While the Federal Reserve saw fit to stand pat on the federal funds rate, the European Central Bank is raising interest rates to combat a worsening stagflation crisis on the continent.

Will the US avoid a stagflation scenario altogether? That is highly unlikely. The energy price shock itself has already made itself known. The real misery index—the combination of real unemployment and year on year consumer price inflation—is rising. To a degree, the stagflation scenario has already begun for the United States.

If the US continues to show strong increases in industrial production, capacity utilization, and manufacturing job growth, we may see the misery index rise less sharply than would otherwise have been the case. We may see less overall demand destruction and greater tolerance for consumer price inflation at least in the short term.

If the peace deal is proven to be substantive and real, and brings meaningful change to the Persian Gulf states, a strong US economy would potentially position the US well to reap tangible benefits from that change. It is far too soon to know if the US will “win the peace” with Iran, but a stronger US economy is surely a better position from which that can happen.

Between the upcoming mid-term elections and the unfolding peace with Iran, right now is an important economic moment for the United States. Fortunately, at this moment, a substantial number of economic signals are showing the US economy is growing.

That’s a nice piece of good news.

The Purchasing Managers’ Index is a survey of supply chain managers assessing expectations regarding current and future business. If the Index prints above 50 it is reporting expansion, If the index prints below 50 it shows contraction.

The media has been buzzing about Elon Musk becoming the world’s first trillionaire, but I’ve seen little discussion on the economic effect from this. I’d like to think that all of the people who bought stock in Space X’s IPO, and others who have benefitted from the markets’ rise, feel wealthy enough now to buy some luxury goods, add a second story onto their houses, and take splurgy vacations. But maybe it’s more of an asset bubble that will just sit there, translating into little retail effect. What do you expect, Peter?

Would the increase in the use of artificial intelligence have any effect on the economy, considering the displacement of employees because of the use of AI?