Is it time to call it a jobs recovery rather than jobs recession?

For nearly three years, the labor market has looked weaker than the headline numbers suggested. Now we have a string of jobs reports indicating the reverse is now true.

Most recently we had the May ADP National Employment Report indicating the US economy is shifting from jobs recession to jobs recovery. That was a marked improvement over the April Employment Situation Summary, which indicated the jobs recession is showing signs of ending, but there are several stagflation indicators on the horizon.

Now comes the May Employment Situation Summary, which makes a very strong case for declaring a jobs recovery underway.

Total nonfarm payroll employment increased by 172,000 in May, and the unemployment rate was unchanged at 4.3 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in leisure and hospitality, local government, and health care. Employment in financial activities declined.

This was not merely a strong jobs report. Total nonfarm payroll employment printed at double Wall Street’s projections, and nearly 70% above the more optimistic Trading Economics Forecast.

It is not a perfect jobs report, and we should not look for a perfect jobs report. Even so, the May jobs report carries much of what I have said would indicate a jobs recovery:

Job growth was still broadly based (although not as broad as April’s).

Wage growth does not appear to have lost ground to inflation (yet—we won’t have the May Consumer Price Index data until later this week).

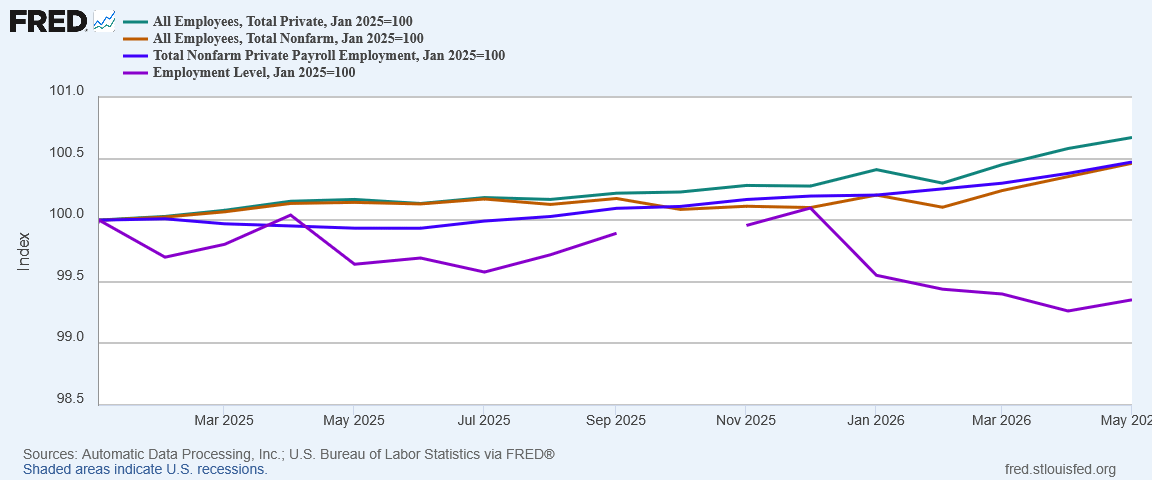

The overall employment level rose for the first time in months.

There are still caveats. Real unemployment did rise slightly, although the increase in the number of individuals not in the labor force who want a job now was very nearly offset by the decrease in official U-3 unemployment.

Yet even when we drill down into the details of the May jobs report, the data points more towards jobs recovery than jobs recession.

Is a jobs recovery underway? The data has been suggesting that for some time, now, and it is increasingly difficult to deny.

Lou Costello Labor Math?

As always, we begin by assessing the extent to which the jobs numbers are reliable. We must always take the data with a grain of salt, in part because we know there will be revisions.

We also have to reconcile the data from the two independent surveys within the Employment Situation Summary: The Current Population Survey (Household Survey) and the Current Employment Statistics (Establishment Survey).

In recent months, the Household Survey’s Employment Level has diverged substantially from the Establishment Survey All Employees data, suggesting the evils of Lou Costello Labor Math are lurking beneath the surface of the jobs report. Yet the May movements for both data sets were strikingly similar, with both showing job growth.

One month of synchronized movements does not mean the taint of Lou Costello Labor Math has been completely banished from the jobs data, but it does give an additional degree of confidence in the May data.

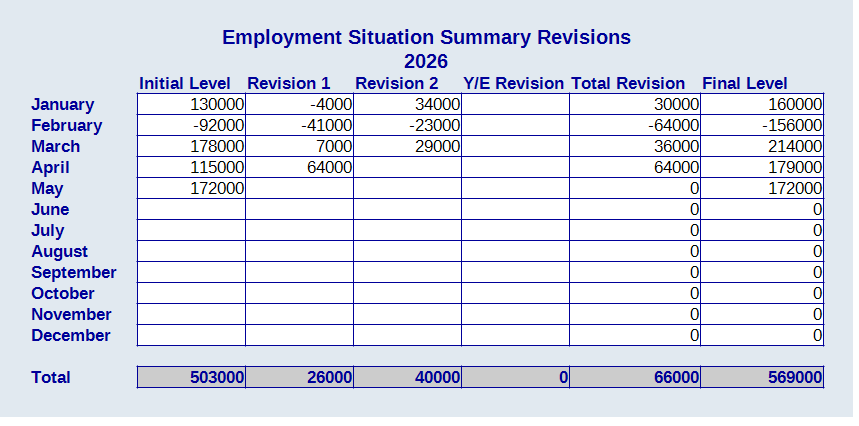

Even more remarkable are the revisions to the March and April data sets. The revisions were not just positive, they were extremely positive (emphasis mine).

The change in total nonfarm payroll employment for March was revised up by 29,000, from +185,000 to +214,000, and the change for April was revised up by 64,000, from +115,000 to +179,000. With these revisions, employment in March and April combined is 93,000 higher than previously reported.

We are presented with an additional 93,000 jobs for 2026 than we have had reported previously. To put that in perspective, the largest job growth number for 2025 was the April 2025 jobs report, which had a revised figure of 108,000 jobs. The revisions on the May 2026 report is on par with receiving an entire extra month of job growth.

Even more significantly, those revisions mean that the revised job totals for 2026 to date are 66,000 jobs higher than the initial reports.

Time is making the BLS data look better and not worse. We have not seen this for several years, and it is a welcome change.

Are the jobs numbers completely trustworthy? The answer is always going to be “of course not,” but between the two surveys showing similar job growth trends and the revisions trending positive rather than negative, we have reasons to be more optimistic about the May jobs data than has historically been the case.

We still need to take the data with a grain of salt, but this month’s grain is quite a bit smaller than it has been.

That bodes well for a jobs recovery narrative.

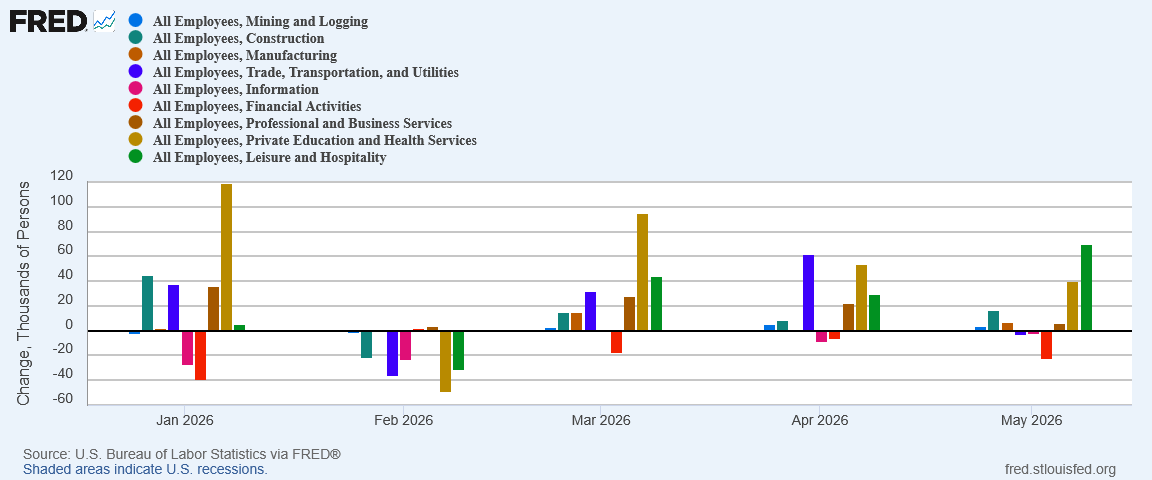

Broad Job Growth, Especially In Goods Producing Jobs

A key indicator of a jobs recovery is that the job growth itself is fairly broad, encompassing most job sectors. The broader the job growth more indicative it is of broad increases in labor demand, which in turn drives real wage growth, which in turn powers real consumption growth and real economic growth.

While more sectors reported job loss in May than in April, job growth for May was still fairly broadly based, and broadly based for the third month in a row.

When job growth is thus both broad and deep speaking of a jobs recession quickly loses credibility.

This is one aspect of the job revisions that is especially significant. When we examined the April jobs report, job growth was not nearly as broadly based as April is printing now.

The April revisions in particular resulted in a much healthier jobs growth outlook.

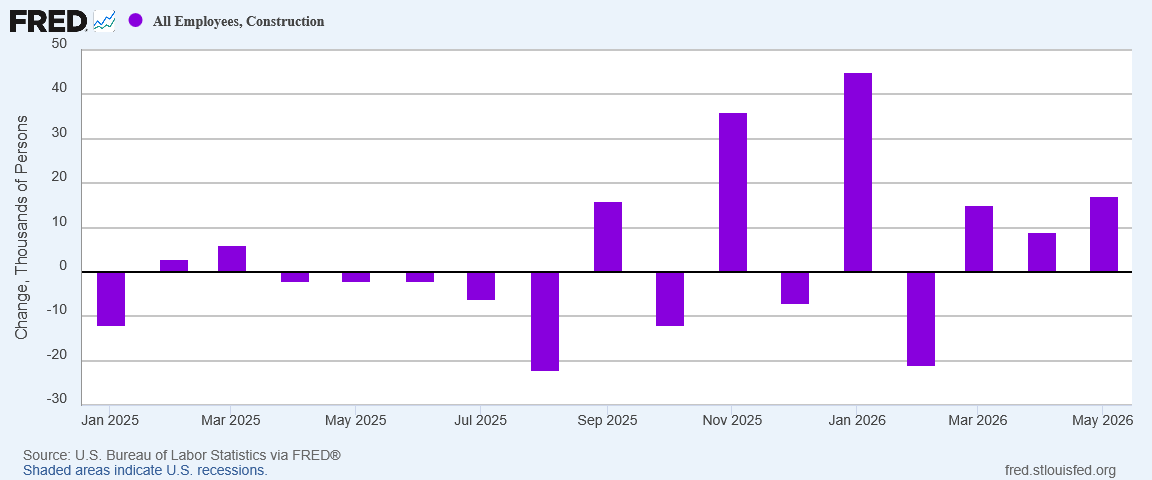

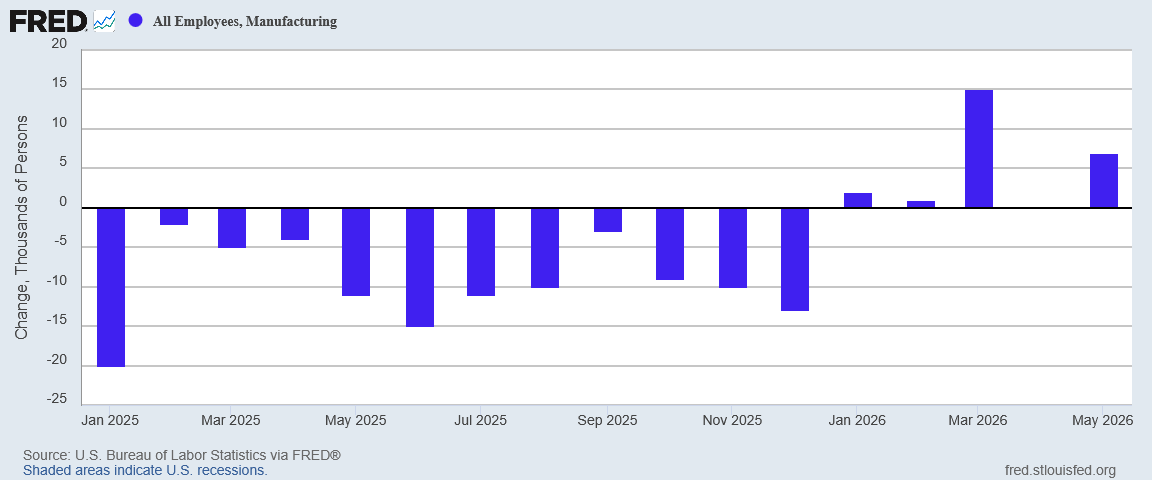

Particularly encouraging is that the past three months have seen job growth across the three main goods producing sectors: Mining, Construction, and Manufacturing.

Given the 2025 had been a bloodbath for Manufacturing jobs, with Construction and Mining jobs scarcely any better, there is no denying that the Employment Situation Summary has been showing a decided trend reversal for goods producing job growth.

As I have said multiple times before, Manufacturing job growth is key to President Trump realizing his Agenda 47 objective of making the United States a manufacturing superpower, the 2026 jobs data shows we may be finally seeing the Manufacturing jobs growth needed for that goal to eventually be met.

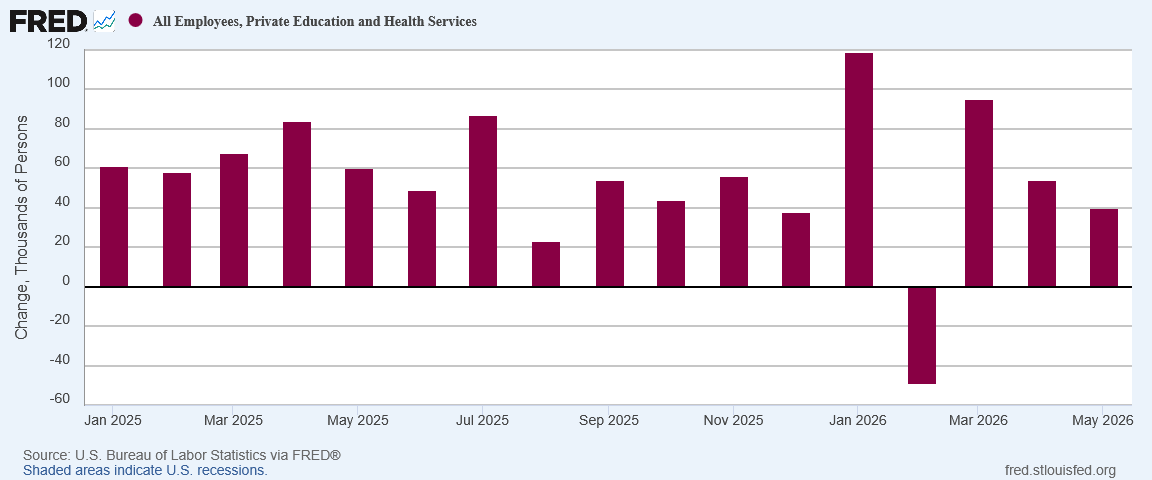

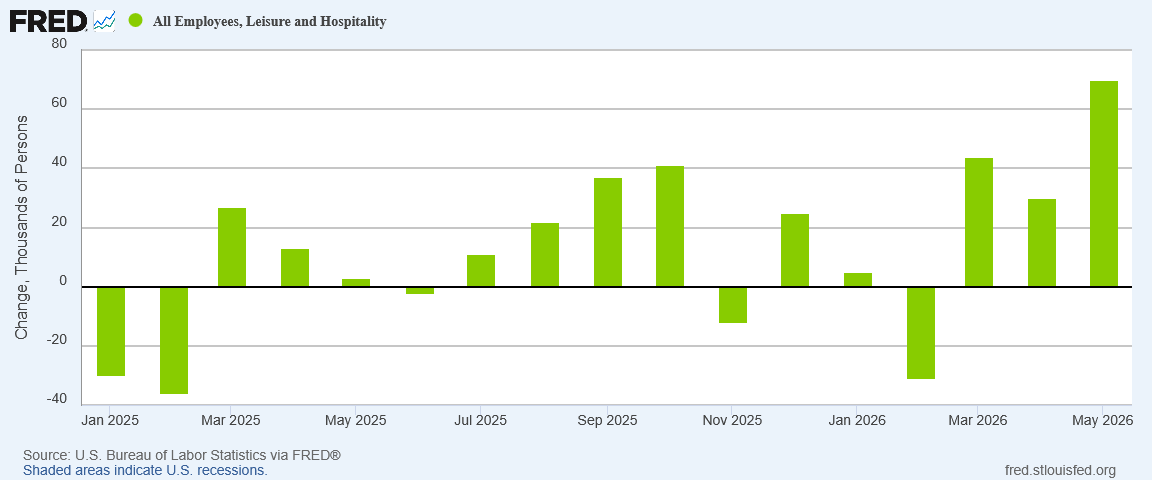

While job growth across goods producing sectors was positive, job growth in service jobs was heavily concentrated in Healthcare and Leisure.

Healthcare has been a mainstay of job growth in this country since before the start of the second Trump Administration, and it is continuing to be a mainstay of job growth.

Leisure has been somewhat weaker in job growth over the past two years, but it has been getting stronger. This is why we look for broad job growth as a sign of jobs recovery—we want to see additional sectors pick up employment momentum without pulling it away from other sectors.

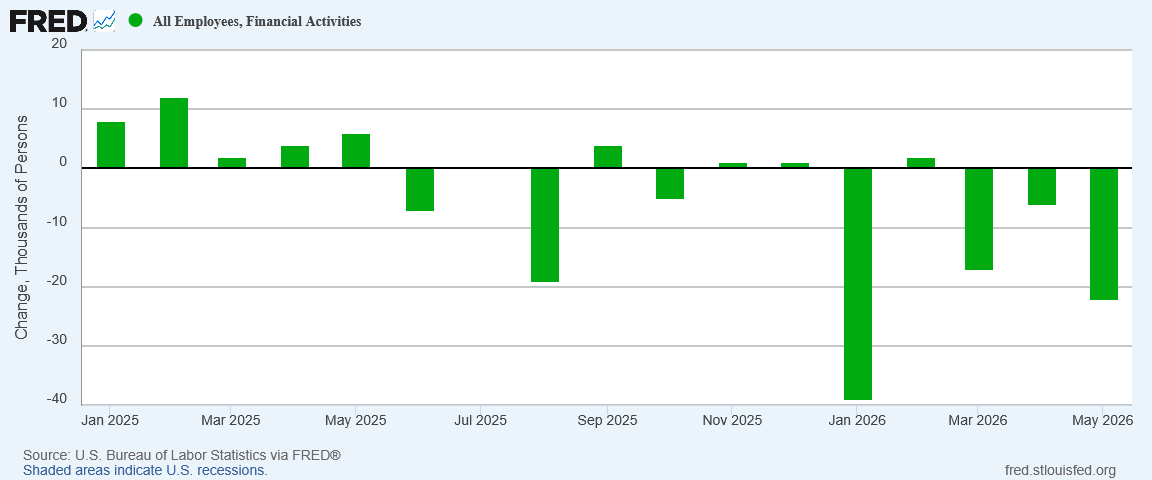

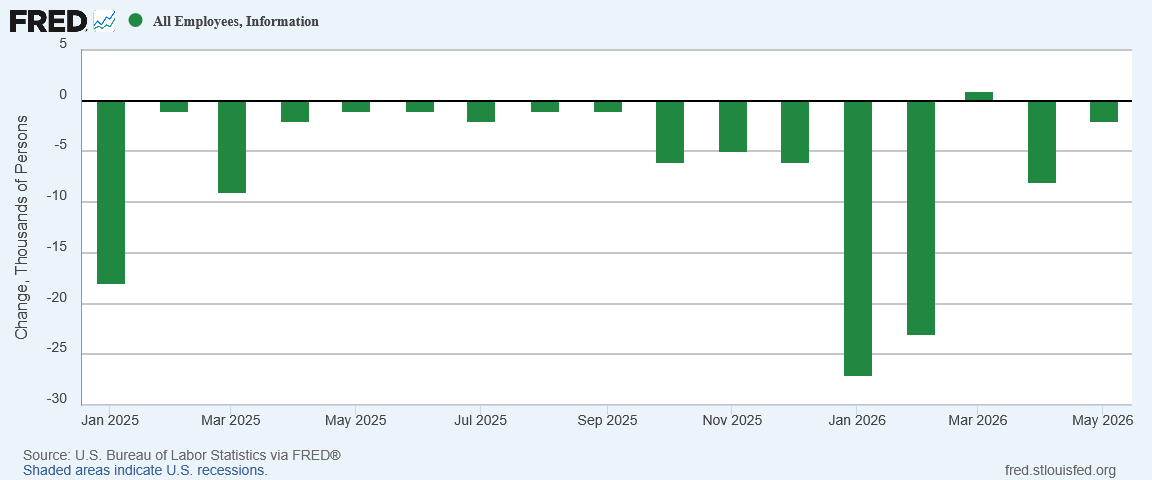

Of the three service sectors which lost jobs, Finance and Information have been losing jobs for months.

May is simply the latest in a long downward trend of job loss for both sectors.

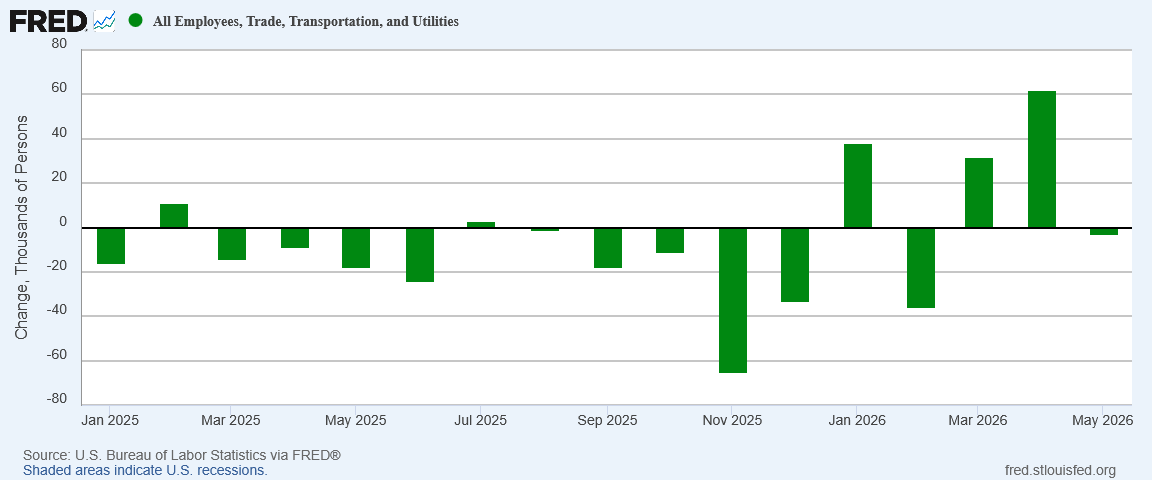

The third sector which lost jobs was Trade, Transportation, and Utilities (TTU).

TTU jobs had been declining throughout 2025, although 2026 has been showing signs of a reversal there as well. Whether the marginal loss of TTU jobs in May marks the end of sector-level strengthening is not something we will be able to see for a couple of months yet.

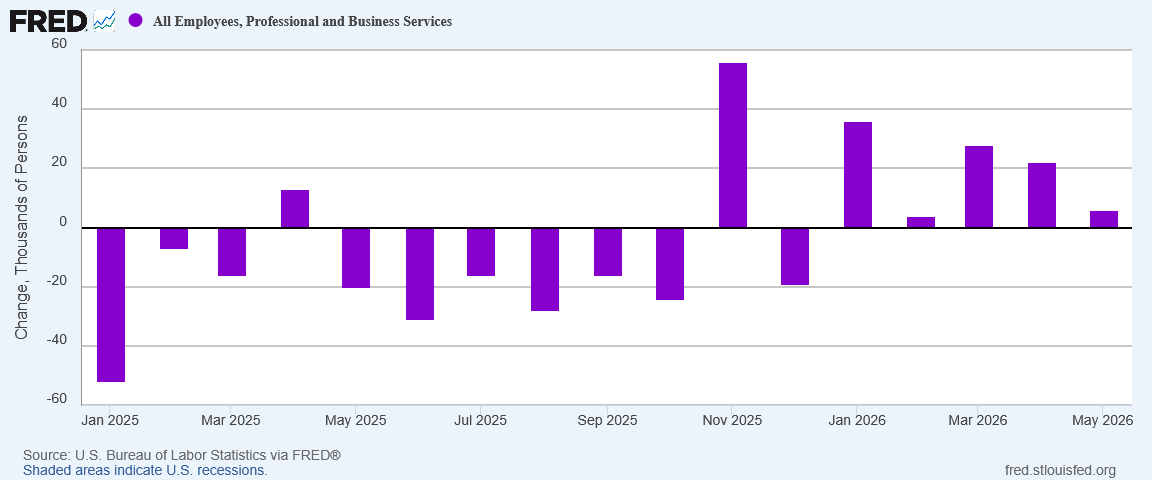

The final major service sector, Professional and Business Services, is something of a cautionary note, for although the job growth is still positive, the level of growth has been diminishing in recent months.

Is the sector about to slip back into the negative, where it was for most of 2025? The trend certainly suggests that it could.

While job growth is far from perfect across the board, most job sectors are showing job growth not just for May but for most if not all of 2026 to date.

That definitely bodes well for a jobs recovery narrative.

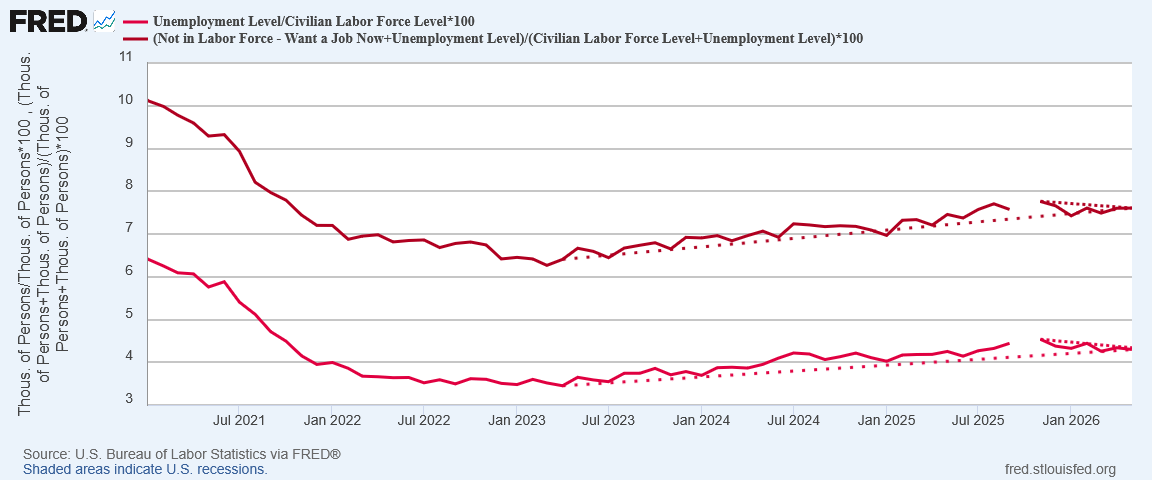

Joblessness Falling? Or Rising Still?

One part of the jobs recovery narrative that is still not certain is whether joblessness is rising or falling in this country.

The unemployment data from the Household Survey is a little contradictory on this point.

The official U-3 Unemployment Level declined 66,000 in May, but the overall number of real unemployed (official unemployment count plus the number of individuals not in the labor force but who want a job now) increased by 76,000. The net increase in joblessness was 10,000, which amounts to less than a 0.01pp increase in the real unemployment rate.

To make sure the unemployment waters are even muddier, we have growing evidence of a trend reversal since November of last year, with both official and real unemployment rates declining, even though the longer term trend since 2023 is still that of rising joblessness.

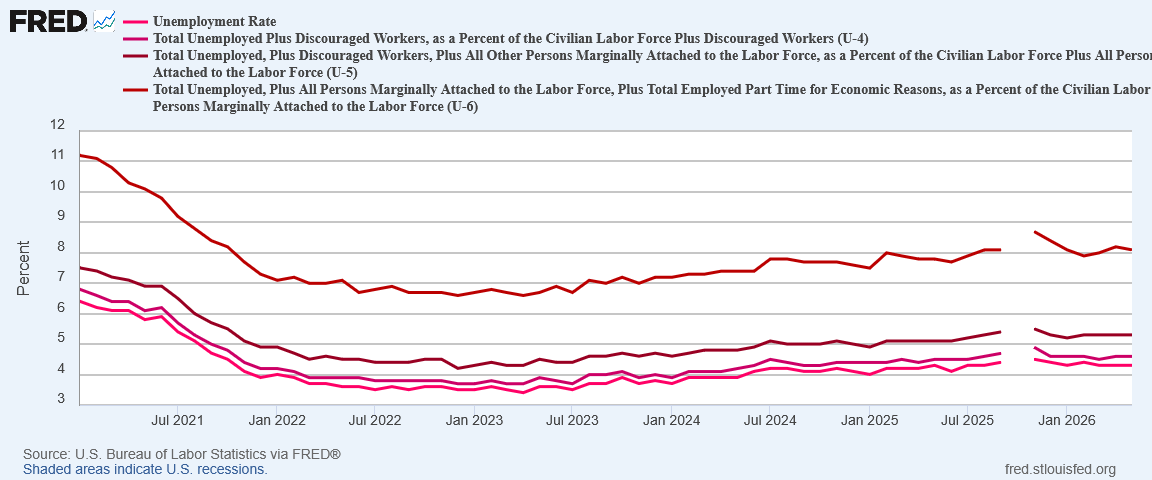

We see the same divergent long-term and near-term trends across the alternative “official” unemployment data.

Has a trend reversal taken place, such that joblessness is now on the decline in this country?

The evidence of that is accumulating, and that evidence augurs very well for a jobs recovery narrative.

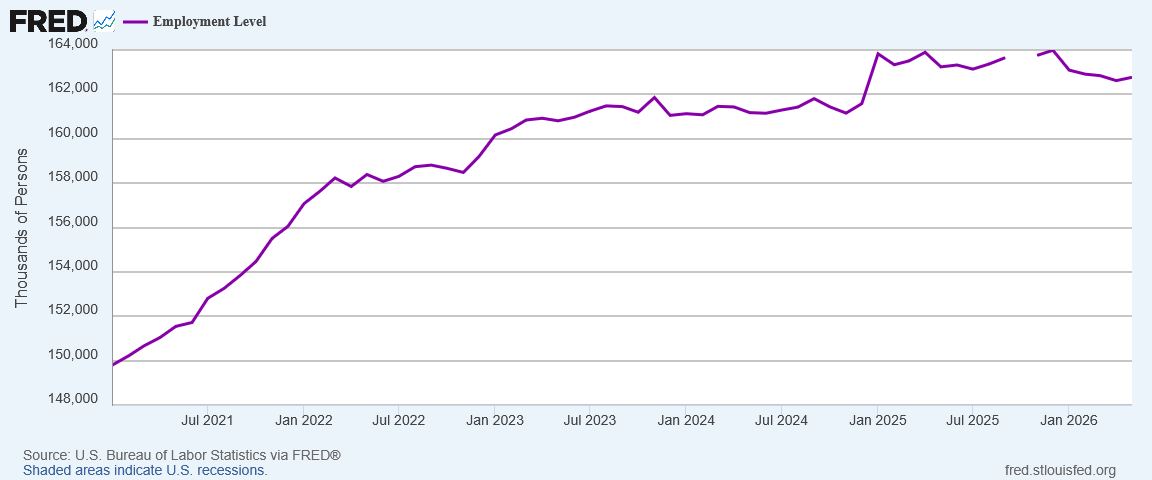

Employment Level Rose In May

Amplifying the improvement in the unemployment data is the increase in overall employment per the Household Survey.

The Employment Level had been declining in this country (which immediately challenges other job growth narratives), but in May it printed an increase of 149,000 workers.

One month does not make for a trend reversal, but with the Employment Level well below where it was when President Trump took office, any sign of improvement is going to be welcome. If the Establishment Survey figures of job growth withstand scrutiny, we should expect to see the Employment level trending up again in the near future.

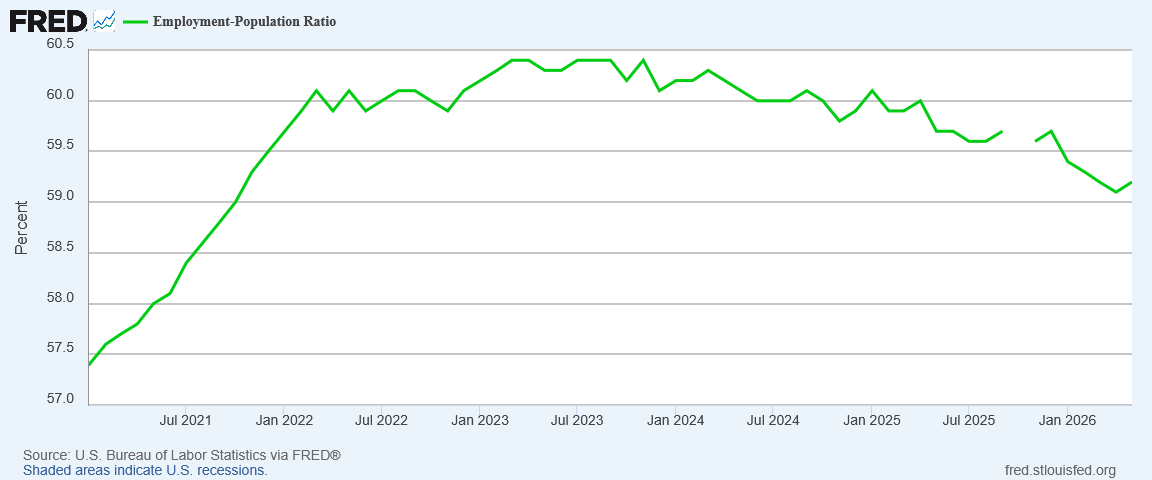

Naturally, the Employment-Population Ratio also increased in May, and was likewise a welcome change from a steady rate of decline.

With any luck, the marginal increases for both numbers will continue. Rising employment levels and a sustained but increasing Employment-Population Ratio would be an extremely prominent pair of jobs recovery signals.

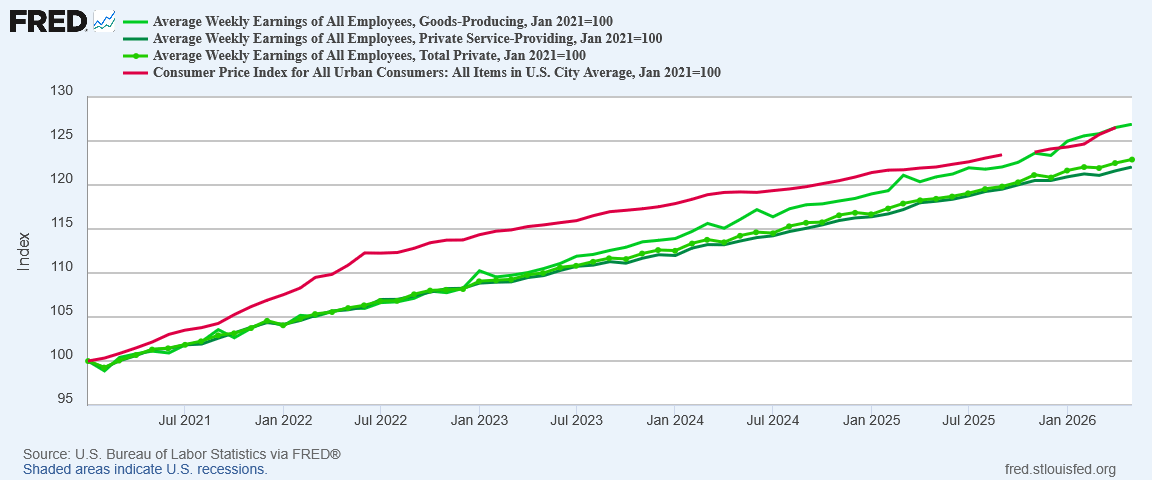

Wage Growth Still Not Quite There

Nominally, wages rose across all job sectors in May. Whether wages rose enough to keep pace with resurgent inflation remains an open question for May.

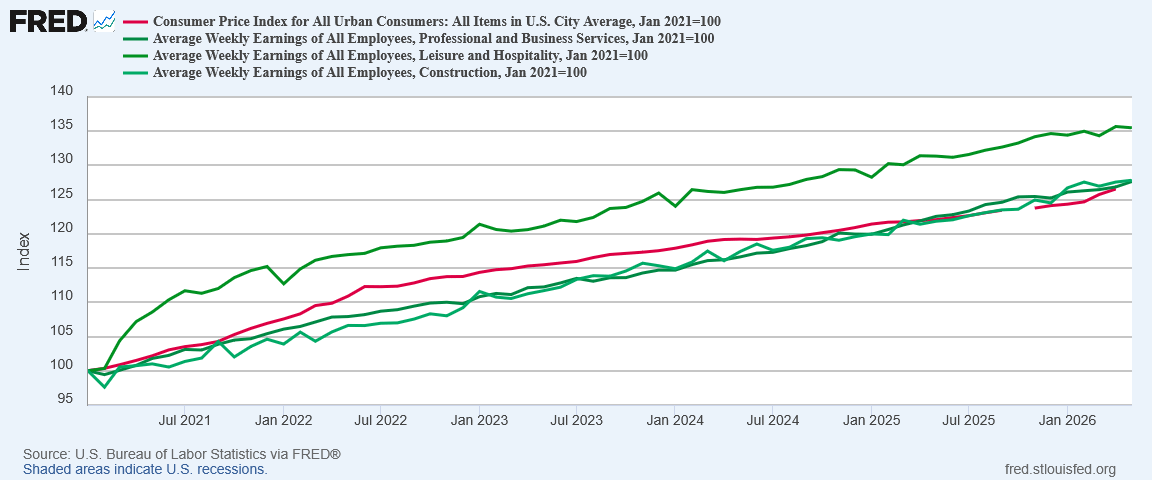

While wage growth has done better in recent years, most sectors still have not seen enough wage growth to overcome the income reduction effects of the 2022 hyperinflation cycle. Goods producing jobs did largely recover from the 2022 cycle, but consumer price inflation’s recent uptick as a result of Iran illegally closing the Strait of Hormuz is threatening could pose another setback.

Wage growth will be a problematic data point for some time, as there have been only three job sectors where weekly earning have overcome the effects of the 2022 hyperinflation cycle: Leisure, Professional Services, and Construction.

Of those, only Leisure has printed strong enough wage growth to plausibly weather currently resurgent inflation. The wage recovery within Construction and Professional Services is marginal enough that any significant increase in consumer price inflation will eliminate those sectors’ real wage gains.

While oil prices have moderated as of late, we should continue to anticipate ongoing energy price inflation and a still-reverberating energy price shock.

Depending on whether inflation prints hotter or cooler for May will determine whether wages kept pace with current inflation or lost ground to rising inflation.

But for the energy price shock and resulting energy price inflation, wage growth in this country arguably would look much better relative to inflation than is does at present. Of course, we do have energy price inflation and that does diminish real wage growth overall.

Even so, until we see the May consumer price index data, we do not see inflation having discernible impact on real wages—not yet.

Wage growth provides the weakest and most problematic support for a jobs recovery narrative. Perhaps the most balanced assessment of the wage data within the jobs report is that May wage growth does not undermine a jobs recovery narrative, even if it does not necessarily provide clear support for that narrative.

Stagflation Signals Status?

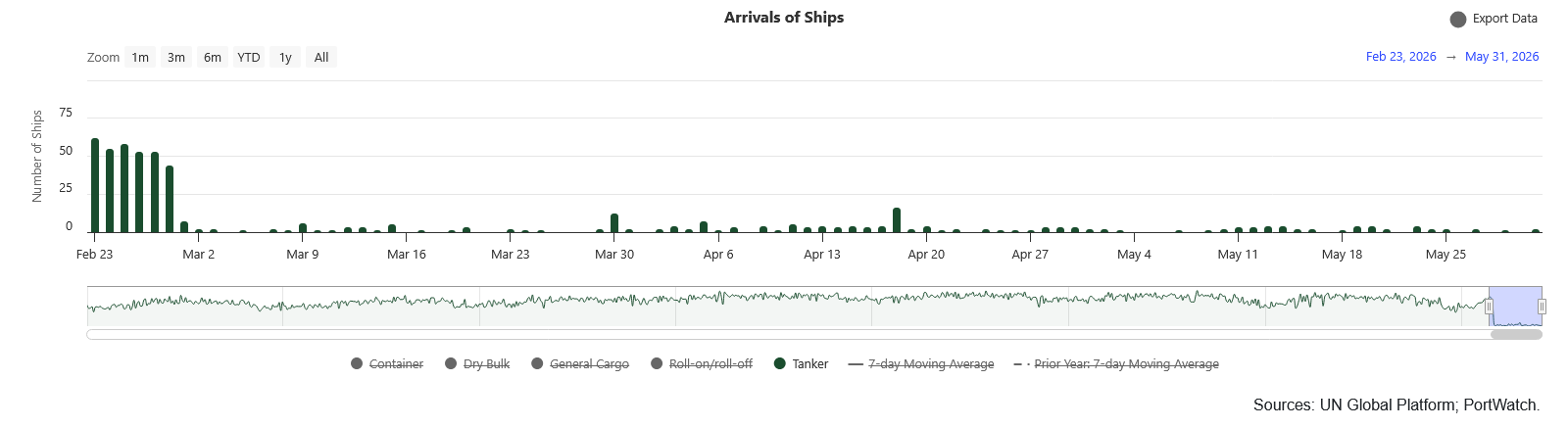

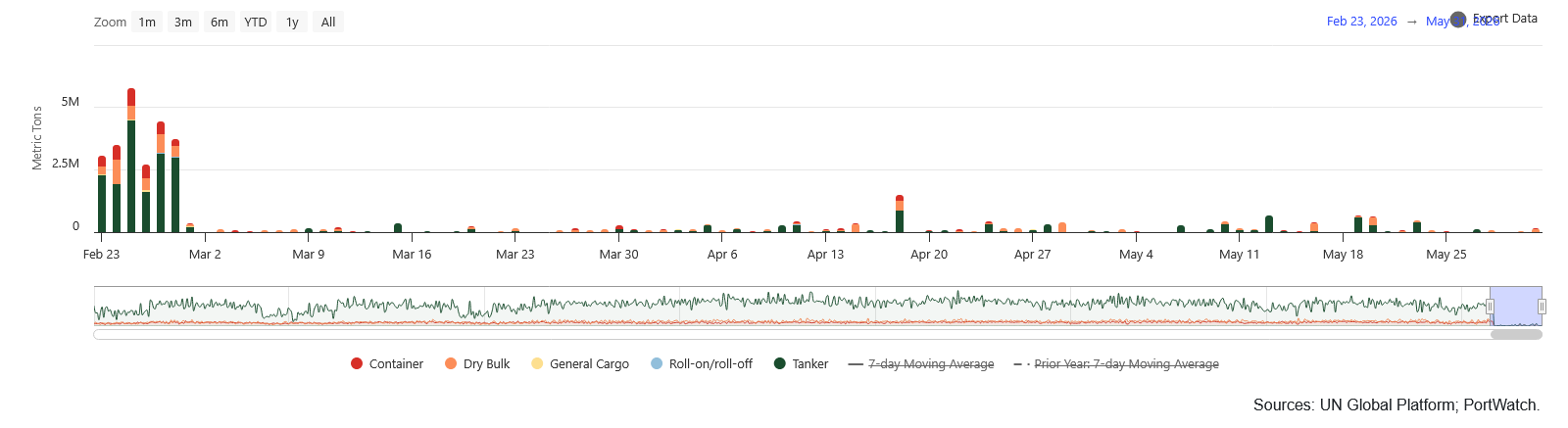

With the ceasefire between the US and Iran having technically “held” since mid-April, the status quo in the Persian Gulf has not changed much.

Iran still has illegally closed the Strait of Hormuz. The US is still blockading Iranian shipping.

As of May 31, tanker traffic through the Strait is still virtually nil.

Overall cargo volumes are equally nonexistent.

Because the Strait is still virtually completely closed, all the stagflation pressures we have seen for the past couple of months are still present.

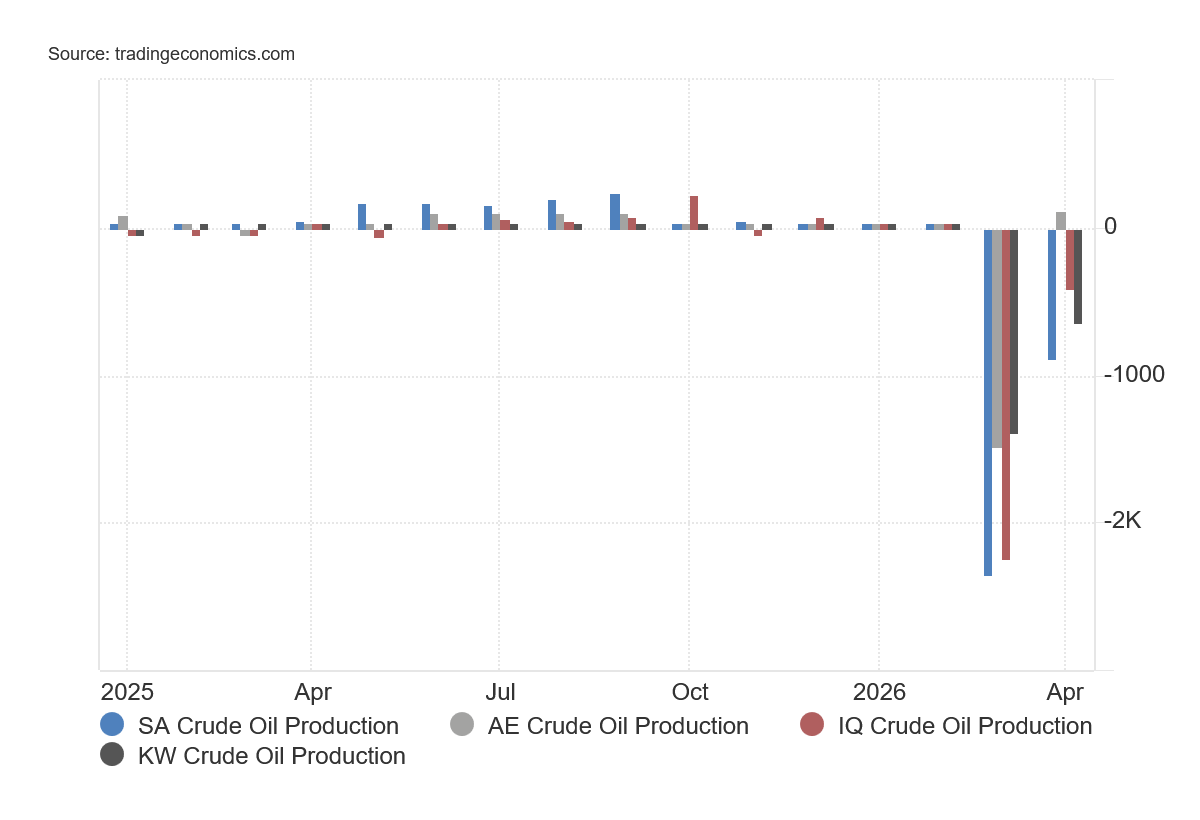

In particular, oil production in the Persian Gulf has plummeted.

Only the United Arab Emirates has managed to regain any of its lost oil production.

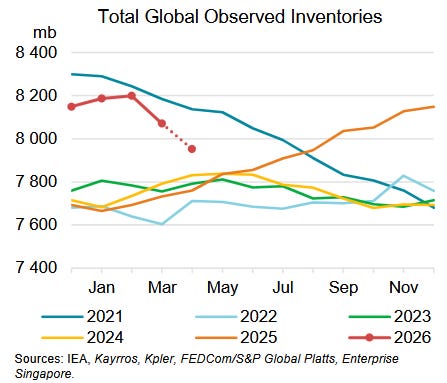

The major industrial economies of the world have so far been able to buffer the resultant supply shock with releases from strategic petroleum reserves.

If the current drawdown trend continues, there is a point in the near future when total global observed oil inventories, including strategic reserves, will no longer be able to buffer the supply shock. When that happens, oil and energy prices are going to move sharply higher.

Currently, energy prices have been moderating, with oil prices trending down from their earlier peaks.

When the buffering of strategic reserve releases is exhausted, this moderating trend will cease. Oil prices will move sharply higher, carrying other commodities prices higher (as they have already done). Global stagflation is largely baked in without a quick peace deal, and even then we might see some of this.

While the price and supply shock side of the stagflation scenario is almost sure to happen, given the lack of progress on peace talks, we have to also remember that stagflation is the collision of inflationary price shocks with the deflationary forces present in a weak or underperforming economy.

If job growth is strengthening in this country, if the economy is therefore growing more or less strongly, then the stagflationary impact of the price and supply shock in energy is reduced in direct proportion to the growth.

Stagflation requires a weak or underperforming economy. Strong job growth would mean a strong and potentially overperforming economy.

If the job growth reported in the Employment Situation Summary over the past few months continues for the next two to three months, when the next price and supply shock does hit the US economy—which most prevailing forecast anticipate in the next one to three months—the US economy may be in a stronger position to withstand that sort of body blow.

The stagflation signals are not going away, nor are they even really diminishing, but the strengthening job markets raise hope that the ultimate stagflation impact arising from the disruption of Persian Gulf oil flows will be proportionally muted.

The best way to avoid 1970s-style stagflation in the US is for there to be an actual jobs recovery over at least the next few months.

No Question: May Is A Good Jobs Report

There is no disputing that the May Employment Situation Summary is a good jobs report.

There is also no disputing that the May ADP National Employment Report is a good jobs report.

The April JOLTS report is more problematic, but it also points to there being at least some job growth in April.

Over the past few months, the jobs reports have reported steadily improving outcomes. We are seeing more and more job growth, and we are seeing it in more and more job sectors.

There is no denying that is what a jobs recovery should look like.

If we can be certain the trends of the past few months will be the trends of the next few months, there would be no question that we were in the midst of a jobs recovery.

That uncertainty about the future is the only restraint on calling a jobs recovery is now underway. If job growth suddenly stops next month, or reverses in a big way as it did in February, the jobs recovery narrative would sound immediately foolish.

If job growth continues, not calling the jobs recovery would also sound immediately foolish.

Is a jobs recovery underway? For now at least, yes, it is. Since March, we are seeing improving job growth numbers. Since March, the revisions to the jobs report have been positive. Wages are growing, and the only reason they might not keep pace with consumer price inflation is the resurgence of consumer price inflation.

We should be mindful that this is a very young jobs recovery. It likely will not take much to snuff out this recovery effort, and the price and supply shocks likely heading towards the US economy over the next couple of months definitely fit within the concept of “much”.

For now, we have a jobs recovery. After nearly three years, we are seeing meaningful job growth in the US economy. We cannot say how long this recovery will last, but it is appropriate to celebrate the jobs recovery while it does last.

The May Employment Situation Summary is a good jobs report which shows a jobs recovery is underway. 2026 is so far a good year for job growth.

That’s good news. We should enjoy it while it lasts (because it may not last).

We can count on you, Peter, to give us a factual, level-headed picture of where things stand - and that’s priceless! Thank you.

With the midterm election season ramping up, Trump has some good figures to spin into votes. If his administration is on the ball, they will find ways to tease apart the data and show that economically, Democrat-controlled cities such as LA and Portland are faring worse compared to Republican locales. If he can combine that data with proof that cities such as LA have rigged previous elections, Republicans could get a sweet response!

Be curious to see if it sustains into the next month, or if we get the typical revisions.