Normally, the inflation data from the Bureau of Economic Analysis tracks with that from the Bureau of Labor Statistics. When the two inflation measures diverge, that is usually an indication something significant is unfolding.

Instead of inflation and spending cooling across the board, the BEA’s Personal Consumption Expenditures Price Index (PCEPI) showed core inflation printing hotter in February, yet with no firm trend in the headline number.

From the preceding month, the PCE price index for February increased 0.3 percent. Excluding food and energy, the PCE price index increased 0.4 percent.

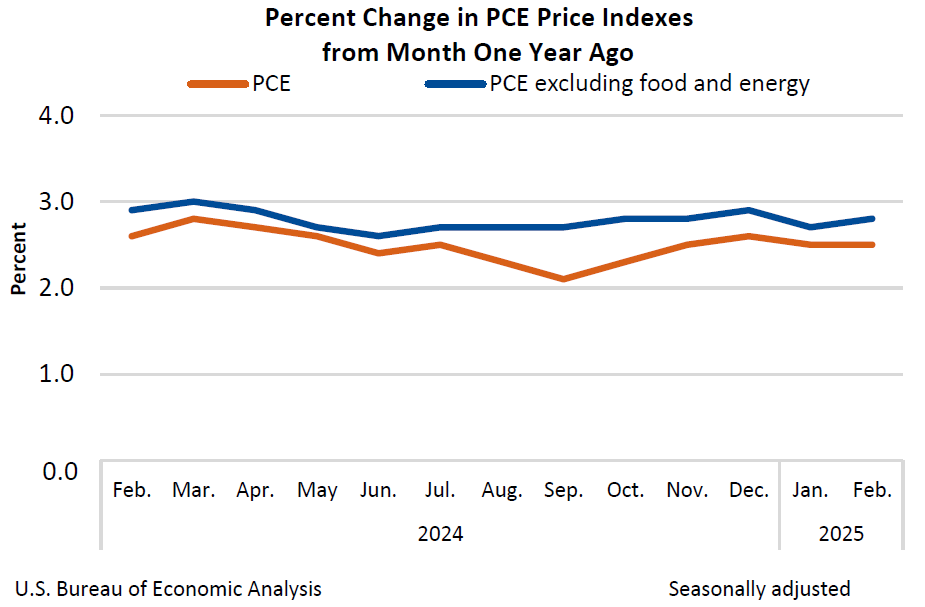

From the same month one year ago, the PCE price index for February increased 2.5 percent. Excluding food and energy, the PCE price index increased 2.8 percent from one year ago.

Are we seeing a return of consumer price inflation? Or are we seeing signs of a potentially more toxic mixture of inflation and deflation signals that herald stagflation instead?

Whichever turns out to be the case, it is not likely to bode well for President Trump’s agenda. Continued economic decline is something voters are expecting Trump to change.

Please support the fight against corporate media propaganda with a paid subscription or a one-time donation on Ko-Fi. Thank you for your support!

Month on month, the numbers were equally muddled, with headline inflation in the PCEPI decreasing just under 0.01pp, to 0.32%, while core inflation rose 0.07pp to 0.37%

Food price inflation, the other component in the headline number outside of core inflation, printed outright deflation in February, dropping by 0.01% month on month.

Even core inflation was something of a mixed bag. Durable goods inflation rose 0.09pp month on month, while non-durable goods fell 0.46pp, and services rose 0.11pp.

While one month’s data does not count as a trend, this is a far cry from the strong cooling signal we saw with the BLS Consumer Price Index data, and if the BEA data is the trend going forward, this mixture of rising and falling inflation rates could signify the start of a stagflationary recession scenario within consumer prices overall.

Break From Consumer Price Index

While the BEA data for February was internally muddled, what was clear is that it was a shift away from the Consumer Price Index data reported earlier. Not only did core inflation move down in the CPI data, both durable and non-durable goods printed deflation month on month, and even services printed a modest disinflation.

That cooling trend was sustained even year on year.

The BEA data is clearly not aligning with the BLS data for February.

Strictly speaking, we should expect them to align, as both metrics theoretically are measuring the same phenomena. We might see variations in the magnitudes, but the trends should match up. A strong disinflation signal at the core in the CPI data should be matched by a disinflation signal in the PCE data. When one prints disinflation and the other prints inflation, the data is telling us that something is shifting.

The increase, which was more than what economists had expected, was driven by a rise in prices for everyday items, suggesting Mr. Trump’s tariffs are starting to have a more notable impact. Until a couple of months ago, goods prices were consistently flat or on occasion turned negative, helping to bring inflation down.

Of course, we should note that the New York Times views all data as the latest sign that Trump’s tariff and trade war strategies are counterproductive.

The Gray Lady also used the inflation print to try to hang the stagflation albatross around President Trump’s neck.

“It shows some preliminary signs of stagflationary pressures,” said Gennadiy Goldberg, head of U.S. rates strategy at TD Securities. “This reinforces the narrative that growth may be becoming a little bit more sluggish even as inflation is starting to show some signs of perking up before we really get the brunt of the trade disruptions.”

Clearly, they mean to be an early adopter in the “Trump-caused recession” narrative.

Return To Norm?

Yet what might actually have occurred is that consumer pricing patterns and behaviors may have reverted to recent norms. That certainly was the case with transfer payments, where the January decline was very nearly offset by a February surge.

Even in the core expenditures breakdown there was a February resurgence in spending on goods, although with a small decrease in spending on services.

Looking ahead into March, we have reason to suspect this may be a broader reversion to the norm, as the supply chain squeeze which appeared to vanish in February returned with a strong signal—namely, a trend reversal in commodities prices, which began rising again.

Even copper prices resumed their previous rise in March, after having fallen during February.

Not only is the BEA seeing rising prices again in February, but we are seeing a number of signals which suggests further price rises in the March data, and perhaps even beyond.

Stagflation Or Inflation?

While the Consumer Price Index data for February showed a clear shift towards disinflation, the PCE data is showing a muddled mess. Some inflation gauges rose, while others either fell or stayed the same.

One hallmark of stagflation is when there is a muddling of price trends, so that inflation and deflation occur at the same time.

Certainly rising commodities prices suggest we will be seeing higher prices for durable goods especially. The much ballyhooed “supply chain squeeze” appears to be coming back to the fore.

Yet energy and food prices are not showing much contribution to inflation, if any. In food prices overall we are even seeing incremental deflation, and energy prices very nearly slipped into deflation on the month.

That would be the precursor to a classic stagflationary squeeze, with constrained commodities prices pushing up some prices, while soft energy and food prices combine to ease upward price pressures overall.

What the PCE data does show, and what the March commodities and interest rate signals suggest, is that the US economy is getting more sluggish. While Trump’s tariff threats are very likely contributing somewhat to the sluggish signals in the data, we should be mindful that the sluggish numbers themselves are a continuation of a sub-par 4th quarter for 2024.

Whether we are looking at stagflation or inflation, we are looking at a softening and deteriorating economy regardless.

If that trend continues that is going to become a political problem for Donald Trump, as resolving the underperforming economy as well as getting consumer prices down are very much at the core of his Agenda 47.

If Trump cannot deliver on the economy his capacity to deliver in other areas is likely to become constrained. Donald Trump needs a win on the economy at least in the short term in order to keep his agenda alive past his first 100 days in office and especially heading into next year’s mid-term elections. We should not forget—and Donald Trump has surely not forgotten—that the Democrats are waiting and fervently hoping for a policy mis-step they can exploit to rebuilt their party’s shattered fortunes.

There is no way yet to assess what will be the ultimate impact of President Trump’s multiple tariff threats and newly instituted tariff policies. We should anticipate that there will be an impact, be it to ease the coming supply chain squeeze or to exacerbate it.

However, what does seem likely is that whatever maneuvering window Trump had with respect to tariffs and trade wars is steadily closing, and may be closed completely in the very near term. An economy that continues to deteriorate is less likely to have the resiliency to contend with the trade disruptions tariffs invariably must bring.

Neither tariffs and stagflation nor tariffs and inflation are likely to turn out well for the economy or for President Trump’s agenda. However, tariffs and either stagflation or inflation are very likely what we are about get, and very soon.

Please support the fight against corporate media propaganda with a paid subscription or a one-time donation on Ko-Fi. Thank you for your support!

Thank you for detailed figures that zero in on what’s going on, Peter. The picture may be muddled, but your analysis SHOWS that it’s muddled, and therefore significant change is beginning.

And this is what I’ve been afraid of. Trump needs to do a better job of explaining to the public how his long-term strategy will work, how we need to be patient. The corporate media will be screaming otherwise, and so Trump needs to counter that, or his agenda is in political trouble.

Peter, I’ve always wanted to ask you about the statistical margin for error in the government figures. For example, if the figure for food inflation declines 0.01 %, is that within the margin for error, and does the government tell us what that margin for error is?

I’m thankful for Bogleheads advice to build a TIPS ladder but now I’ll have to see what happens to them in stagflation. Anyone shopping for basic staple goods is not caught off guard by inflation. I wonder how inflation will be impacted if we have a “conflict” or even war given the armament build up in Diego Garcia and tensions mounting with Iran? The Middle East is always explosive but things seem to have escalated.

Thank you for detailed figures that zero in on what’s going on, Peter. The picture may be muddled, but your analysis SHOWS that it’s muddled, and therefore significant change is beginning.

And this is what I’ve been afraid of. Trump needs to do a better job of explaining to the public how his long-term strategy will work, how we need to be patient. The corporate media will be screaming otherwise, and so Trump needs to counter that, or his agenda is in political trouble.

Peter, I’ve always wanted to ask you about the statistical margin for error in the government figures. For example, if the figure for food inflation declines 0.01 %, is that within the margin for error, and does the government tell us what that margin for error is?

I’m thankful for Bogleheads advice to build a TIPS ladder but now I’ll have to see what happens to them in stagflation. Anyone shopping for basic staple goods is not caught off guard by inflation. I wonder how inflation will be impacted if we have a “conflict” or even war given the armament build up in Diego Garcia and tensions mounting with Iran? The Middle East is always explosive but things seem to have escalated.