"Too Late" Powell Is Sure To Live Down To His Trumpian Tag

A 25-Point Rate Reduction Won't Cut It

Wall Street is convinced that the Federal Open Market Committee will trim the federal funds rate by 25 basis points at the conclusion of its two-day meeting tomorrow.

The Federal Reserve will cut its key interest rate by 25 basis points on September 17 as labor market softness overshadows inflation risks, said almost all 107 economists in a Reuters poll, with most expecting one further cut next quarter.

Given Jay Powell’s predilection for pandering to Wall Street’s expectations, it would be quite a shock if tomorrow the Fed announced anything other than a 25bps rate cut.

That tells us something else about the Fed’s rate-cut decision: at 25 basis points, Powell is all but certain to live down to his Trumpian “Too Late” tag.

The markets are signalling they want a dramatic rate cut.

The employment data from the Bureau of Labor Statistics, tainted though it is by sloppy data management and lack of methodological rigor, has been crying for months for a dramatic rate cut.

Wall Street does not see Jay Powell even thinking about a dramatic rate cut, and we are not likely to see a dramatic rate cut.

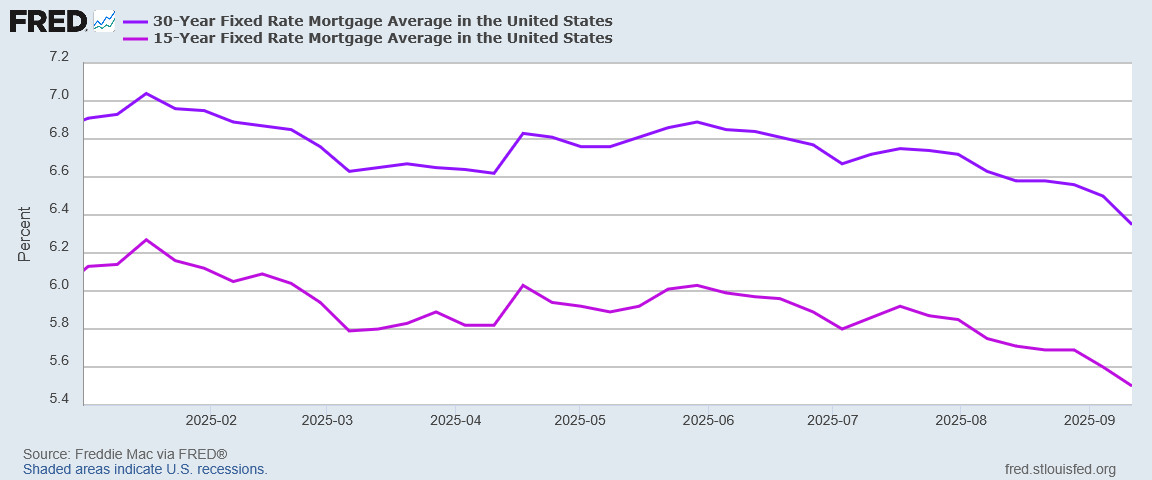

Leading the push for a significant rate cut is the 30-year fixed mortgage rate from Freddie Mac, which last week dropped 15bps. More significant than last week’s sharp drop, however, is the 54bps decline in the 30-year mortgage rate since the beginning of June.

Since January 16, the 30-year mortgage has dropped 71bps.

Market interest rates really and truly want to move lower. A large rate cut very likely would catalyze a significant drop in mortgage rates, corporate debt, and Treasuries.

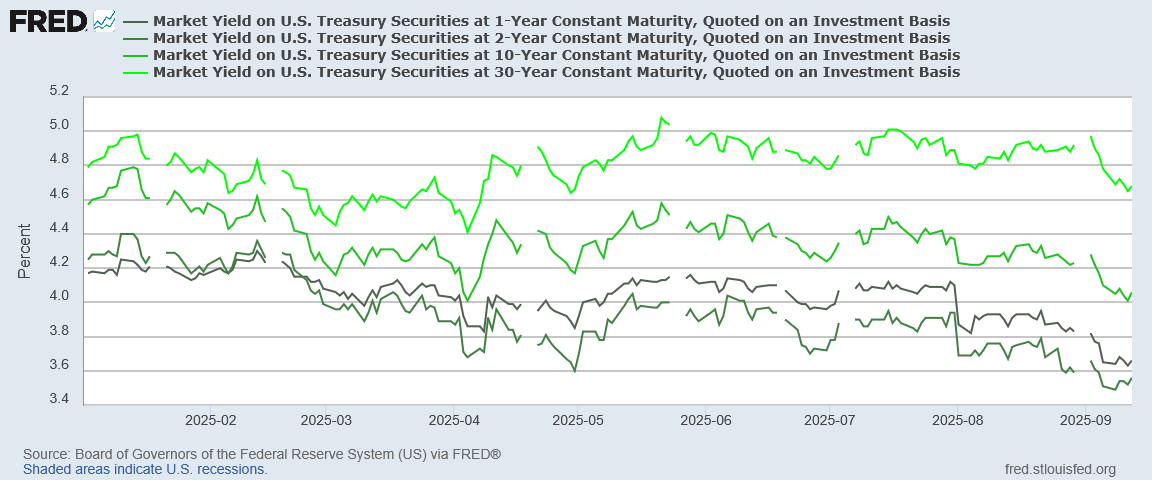

Keep in mind that mortgage rates are following Treasuries lower.

Since the middle of May, the 10-Year Treasury rate has dropped 54bps, and the 30-Year rate has drop 40bps.

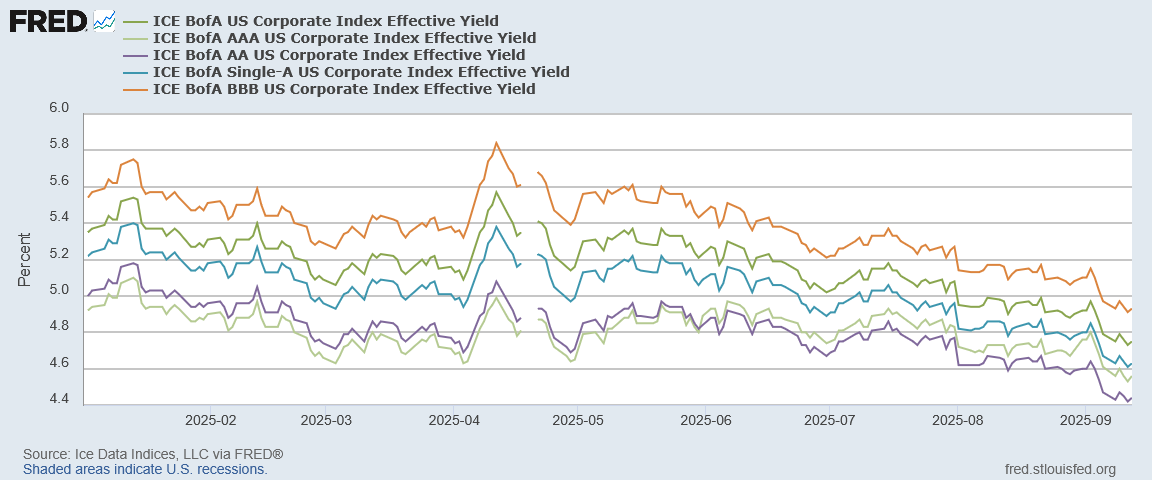

The leader, however, is corporate debt, which has moved 82bps lower since April 11.

Over the past week, corporate debt yields have reached their lowest point all year, as have Treasuries and fixed rate mortgages.

Wall Street’s message to Jay Powell is clear: lower rates.

That Main Street has been pining for a rate cut was made plain months ago, in the weak and deteriorating jobs numbers that corporate media only just now decided to notice.

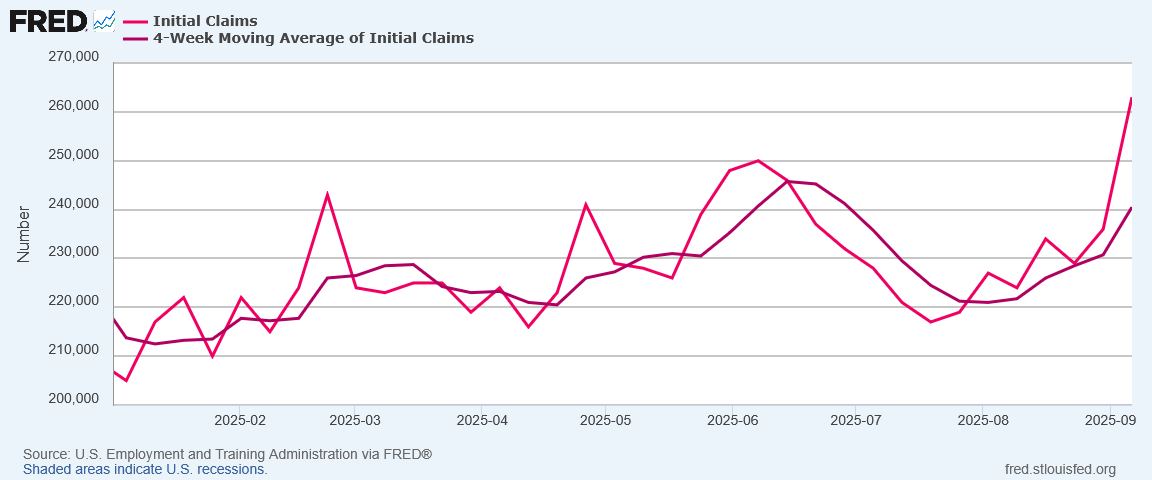

Last week’s surge in initial unemployment claims underscores just how much Main Street needs a rate reduction.

Initial claims have been rising since the middle of July, after declining from a summer peak in mid-June.

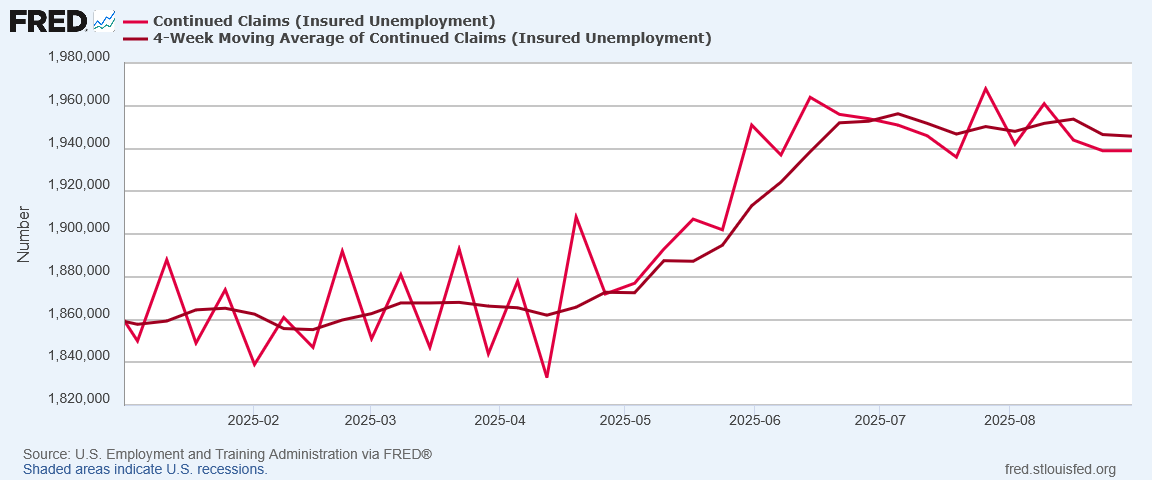

While Continued Claims plateaued in July, that was only after rising by 100,000 since the start of the year.

The only good news in the Continued Claims data is that long-term unemployment for the moment is not getting any worse.

Coming on the heels of August’s anemic-and-sure-be-revised-down jobs number, the weekly unemployment stats confirm the trend of rising joblessness in this country.

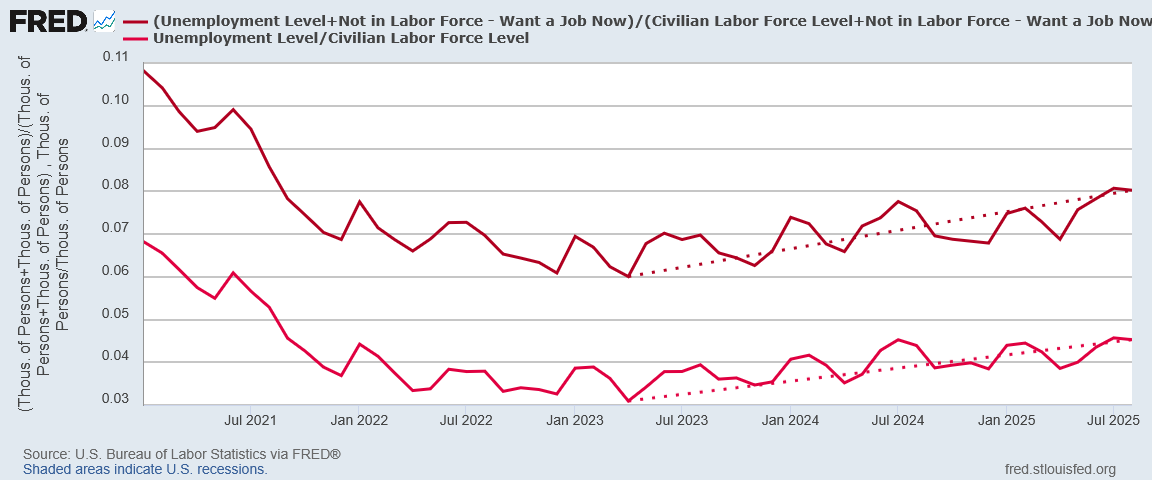

Bear in mind the trend of rising joblessness extends back to April of 2023.

April 2023 is when labor markets stopped getting stronger post-COVID.

November 2023 is when the jobs recession began. It has continued uninterrupted until now.

If the Federal Reserve wants to goose labor markets sufficiently, a 50bps rate cut is the very least it should announce on Wednesday. A 75bps cut, or even a full percentage point, would be preferable.

Wall Street would probably rally with a large rate cut. Treasuries, corporate yields, and mortgage rates would all drop significantly—that last would deliver a much-needed stimulus shot to housing markets. Equities would surge, but Wall Street rather likes asset price inflation (which is why it has tolerated more than a decade of recklessly loose monetary policy by the Fed).

Wall Street wants a large rate cut of 50bps or more—but Wall Street is only pricing in a 25bps rate cut. That’s how much confidence Wall Street has in Powell’s ability to understand the economic data he claims drives Fed decisions on interest rates.

Tomorrow afternoon, the FOMC will announce its 25bps rate cut. Jay Powell will give his post-meeting presser and probably spook Wall Street as only he can with his witless ramblings.

Main Street will be stuck with a reduction in the federal funds rate that will be both too little and too late to disrupt the steady deterioration in labor markets.

That is what Wall Street has actually priced in: Jay “Too Late” Powell earning his Trumpian tag.

And why wouldn’t he push a 50 bp cut? The one and only reason is because it would help Trump too much. Powell is a partisan hack who demonstrates it time and again through inaction or, in this case, minimal action.

Makes me wanna cry