Now comes the fallout. Is the banking crisis over? Is it even close to being over?

Over the weekend, the Swiss National Bank and the Swiss banking regulator FinMa scrambled to arrange a "shotgun wedding" merger between dying Credit Suisse and its Swiss rival UBS.

After much wrangling and requests (read “demands”) for government assurances on Credit Suisse debts and liabilities, UBS finally on Sunday made a tender offer for Credit Suisse at $0.27/share.

After much back and forth, UBS and Credit Suisse finally agreed on a stock purchase (Credit Suisse investors get UBS stock instead of cash for their Credit Suisse stock) worth approximately $3 Billion.

UBS (UBSG.S) sealed a deal to buy rival Swiss bank Credit Suisse (CSGN.S) in an effort to avoid further market-shaking turmoil in global banking, Swiss authorities said on Sunday.

The Swiss central bank will supply substantial liquidity to the merged bank, it said at a news conference in the Swiss capital, Bern. It said the deal marked a solution to secure financial stability and protect the Swiss economy in an exceptional situation.

With the deal having been done while markets were still closed for the weekend, the hope throughout the banking world is that this will “finally” stop the turmoil, the decline in share prices, and, most importantly, the steady outflow of deposits from banks large and small.

It would be very nice if that were the case. Don’t count on that happening.

While the deal may prove beneficial to UBS over the long term, in the immediate situation it has not changed much. Credit Suisse’ assets are changing hands, but the underwater investments are still underwater, and the money-losing operations are still losing money.

UBS as much as admitted this in their press announcement of the merger, as they do not expect to see a profit from the deal until 2027.

UBS anticipates that the transaction is EPS accretive by 2027 and the bank remains capitalized well above its target of 13%.

“EPS accretive” is finance-speak for the deal adding to UPS’ earnings per share—i.e., “profitable.” The merger won’t be profitable for UBS for four years.

One eye-catching provision in the deal: it’s being rammed through without shareholder approval. Credit Suisse management and Swiss regulators said yes, and that’s good enough, apparently (rather like the mother and the father of the bride consenting to the marriage without actually asking her).

The transaction is not subject to shareholder approval. UBS has obtained pre-agreement from FINMA, Swiss National Bank, Swiss Federal Department of Finance and other core regulators on the timely approval of the transaction.

UBS Chairman Colm Kelleher put the situation bluntly:

UBS Chairman Colm Kelleher said: “This acquisition is attractive for UBS shareholders but, let us be clear, as far as Credit Suisse is concerned, this is an emergency rescue. We have structured a transaction which will preserve the value left in the business while limiting our downside exposure. Acquiring Credit Suisse’s capabilities in wealth, asset management and Swiss universal banking will augment UBS’s strategy of growing its capital-light businesses. The transaction will bring benefits to clients and create long-term sustainable value for our investors.”

UBS is taking on Credit Suisse to prevent a complete meltdown of Europe’s 17th largest bank by total assets, with all the contagion risks and ripple effects that implies.

How bad the meltdown would be is somewhat indicated in Credit Suisse’ announcement of the combine, in the disclosure of the haircut being imposed on certain CS bondholders.

On Sunday, Credit Suisse has been informed by FINMA that FINMA has determined that Credit Suisse’s Additional Tier 1 Capital (deriving from the issuance of Tier 1 Capital Notes) in the aggregate nominal amount of approximately CHF 16 billion will be written off to zero.

The “Tier 1 Capital Notes”, also known as “AT1 Bonds”, are a special breed of investment security introduced in Europe after the Great Financial Crisis, specifically to impose a loss of capital—or a “haircut”—on bondholders in the event of a bank collapse.

AT1 notes are a key instrument in regulators' post-crisis bail-in regime, which seeks to impose principal losses on creditors during firm-level financial distress, outside the normal bankruptcy process, and, in theory, without recourse to the public purse. Regulators hope hybrid securities and the provision of ex-ante rules to ensure orderly re-capitalization, or eventual liquidation, of a given institution can take place without triggering system-wide distress.

In the case of Credit Suisse, the AT1 bondholders just lost their entire investment.

Who are these bondholders? Mainly other banks.

Private banks and retail investors – before they were banned by the FSA in 2014 – have traditionally been the main buyers of AT1 instruments followed by asset management companies, hedge funds and banks. Aside from calls to standardize the regulatory treatment of bank securities, investors are still trying to understand the mechanical trigger levels, loss-absorption mechanism and discretionary triggers that should influence AT1 yields.

How much liquidity at other banks just evaporated is indeterminate at this time. However, if ₣16 Billion got wiped out in the “rescue” of Credit Suisse, it follows that considerably much more would have been lost in a “worst case” meltdown.

Whether the loss of ₣16 Billion across other banks and investment funds throughout Europe is its own contagion ripple effect won’t be known until the markets have had a chance to digest the merger.

As of this writing, bank stocks in Asian markets are taking a beating, and the AT1 bonds of other banks are coming under increasing scrutiny.

Worries about what that might mean for holders of AT1 bonds issued by other banks added to persistent anxiety about a range of other risks including contagion, the fragile state of U.S. regional banks and moral hazard.

Standard Chartered Plc and HSBC shares each fell more than 6% in Hong Kong on Monday to more than two-month lows, with HSBC facing the possibility of posting its largest one-day drop in six months. The MSCI index for financial stocks in Asia ex-Japan (.MIAX0FN00PUS) was down 1.3%.

In other words, there is at least some contagion, and not just a small amount.

What the UBS-Credit Suisse merger cannot do, any more than Dimon’s Eleven depositing $30 Billion with First Republic could hope to do, is change the fundamental dynamic—all of Credit Suisse low-yield assets are still on Credit Suisse’ books, and are still a financial burden.

This is a point that corporate media has either ignored, not understood, or deliberately glossed over, and yet it goes to the very heart of this banking crisis.

It is a basic principle of finance that raising interest rates makes any investment locked into the historical (‘low”) rates worth less.

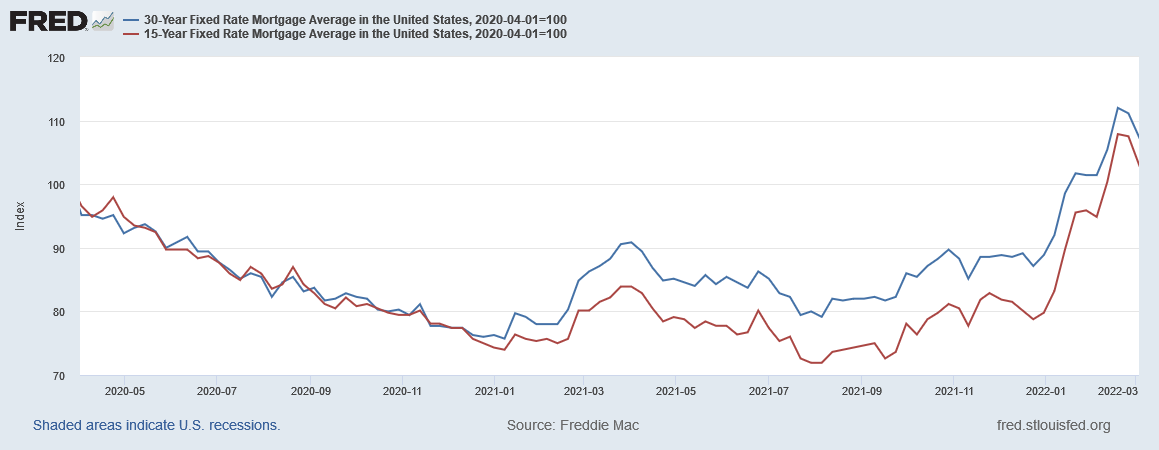

Nor does it take much movement in interest rates to achieve significant declines in the market value of legacy debt securities. By way of illustration, if we index the interest rate percentages applied to 15- and 30-Year mortgages in the US, we see that between April of 2020 (the end of the COVID Recession) and March 2022 (when the Fed began hiking the Federal Funds rate), mortgage rates increased 3.1% and 7.4% of their April 2020 levels (note, this is a percentage of the original rate, not an increase by 3.1 percentage points).

Over the same time period, the SPDR Mortgage-Backed Bond Exchange Traded Fund—which gives a good metric of the market value of a portfolio of mortgages—as well as the CMBS Ishares Exchange Traded Fund, lost 7.63% and 3.38%., respectively.

Note, this decline in the value of mortage-backed securities occurred before the Federal Reserve started raising the federal funds rate.

If we look at those same interest rates from early March, 2022, to the present, we can see approximately how much just the mortgages banks had on the books in 2022 have lost value in a rising interest rate environment.

In the year since the Federal Reserve began raising the federal funds rate, the SPDR ETF shed 10.14% of value, and its commercial cousin, the CMBS ETF, lost 9.16% of market value.

In this same period, the 30-Year mortgage rate rose 71.4% of its March, 2022 level, and the 15-Year mortgage rate rose 90.9%.

Viewed more normally in terms of percentage point increases, mortgages rates over this time period rose by about 3 percentage points.

If we look at Treasury yields, and compare them to associated Exchange Traded Funds, we can see how much the interest rate hikes between March, 2022, and the present have cost Treasuries in fair market value.

Depending on the spot on the yield curve, interest rates in this country have risen approximately 2-4 percentage points. Over that same time frame, the GOVT ETF, which tracks Treasury yields, and the IEF ETF investing on the 7-10 year time frame for Treasuries, shed as much as 3-3.5% of their fair market value.

Interest rates have risen by roughly 3 percentage points, and investments in debt securities have declined in fair market value by roughly 3 percentage points. As interest rates go up even higher, the ETFs tracking specific securities will decrease in fair market value.

One point bears repeating often here: these securities are not “toxic” in the usual sense, where there is a rising risk of default. A quick review of loan default rates shows that the major areas of default risk among consumer loans in the US are primarily credit card debt and similar loans, not mortgages.

Commercial loans are not presenting with any increased default risk at all.

The only reason banks’ investments in debt securities (including mortgages) are losing value is because interest rates for new securities have risen, while interest rates on legacy securities remain locked in based upon the terms of the security. By and large, the securities themselves are notionally sound, but with a return that is no longer profitable.

Rising interest rates wreck the market value of legacy debt securities. Every time.

This relationship between rising interest rates and declining fair market value of legacy debt securities is true for all interest rates, all interest-bearing instruments, held by all banks worldwide.

This relationship is why FDIC Chairman Martin Gruenberg publicly estimated1 that banks were sitting on some $620 Billion in unrealized losses in investment securities.

However, Gruenberg is very likely understating the situation. Remember, the relationship holds for all debt securities, not just Treasury notes. Corporate bonds and mortgage-backed securities, as well as mortgages themselves, are all impacted in the same general way by rising interest rates. By definition, this issue is much larger than US Treasury investments alone.

Last week a team of economists, led by Erica Jiang of the University of Southern California, published the results of their research2 into the investment portfolios of America’s banks, in which they attempted to quantify the impact of the Fed’s monetary tightening, raising of interest rates, and the contribution of same towards liquidity problems and bank runs. They found some 200 banks with potentially lethal exposures to underwater securities and investments as a result of the rising interest rate environment of 2022.

We analyze U.S. banks’ asset exposure to a recent rise in the interest rates with implications for financial stability. The U.S. banking system’s market value of assets is $2 trillion lower than suggested by their book value of assets accounting for loan portfolios held to maturity. Marked-to-market bank assets have declined by an average of 10% across all the banks, with the bottom 5th percentile experiencing a decline of 20%. We illustrate that uninsured leverage (i.e., Uninsured Debt/Assets) is the key to understanding whether these losses would lead to some banks in the U.S. becoming insolvent-- unlike insured depositors, uninsured depositors stand to lose a part of their deposits if the bank fails, potentially giving them incentives to run. A case study of the recently failed Silicon Valley Bank (SVB) is illustrative. 10 percent of banks have larger unrecognized losses than those at SVB. Nor was SVB the worst capitalized bank, with 10 percent of banks having lower capitalization than SVB. On the other hand, SVB had a disproportional share of uninsured funding: only 1 percent of banks had higher uninsured leverage. Combined, losses and uninsured leverage provide incentives for an SVB uninsured depositor run. We compute similar incentives for the sample of all U.S. banks. Even if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to insured depositors, with potentially $300 billion of insured deposits at risk. If uninsured deposit withdrawals cause even small fire sales, substantially more banks are at risk. Overall, these calculations suggest that recent declines in bank asset values very significantly increased the fragility of the US banking system to uninsured depositor runs.

Let those numbers sink in: US banks are carrying assets on their books for $2 Trillion more than their fair market value. If uninsured depositors get spooked and start pulling their money out, nearly 200 banks involving $300 billion of insured deposits could potentially go under.

This was what happened to Silicon Valley Bank, prompting a regulatory takeover. This is what has been happening at First Republic Bank, prompting Dimon’s Eleven to plunk $30 Billion in uninsured deposits in the bank, which only bought it 120 days to resolve its exposures to underwater debt securities.

This was the final nail in the coffin of Credit Suisse, for interest rates have been rising in Europe as well as in the US, with all the major central banks having raised rates over the past year.

This was what triggered the margin calls and near-meltdown of UK-based pension plans last fall.

The shotgun wedding merger of UBS and Credit Suisse does not address this issue in the slightest, other than to add Credit Suisse’ exposure to that of UBS, with the silent prayer that UBS has enough capital and liquidity to survive.

UBS may have enough reputation in banking and finance circles to soothe anxieties over Credit Suisse deposits and thus halt the outflow of those deposits. That might be enough to stop the bleeding for now. The turmoil in Asia noted above suggests that hope is already in vain.

Yet the exposures to underwater securities remains—and the Jiang study only reviewed US banks and US securities, which means their $2 Trillion figure does not include European exposures to the same problems driven by the same reason.

European banks have the same exposures, however. Interest rates have risen just about everywhere in the world, which means every bank has potential exposure to underwater investments that are notionally sound, but with yields below current market rates. We may not have a quantified figure for Europe as we now do for the US, but it is certain that there is a quantity of impaired assets on par with that same quantity in the US.

How much will it take before a run starts at UBS, just like was ongoing at Credit Suisse? Will UBS survive the morning’s Asia bloodbath?

There is no way to know, and no way to predict, when or if the outflow of deposits will resume—or indeed if it will even stop. If all that happens is a general slowing of the pace of outflows, the UBS-Credit Suisse merger will buy a brief grace period at most before its UBS’ turn to confront financial meltdown and collapse (and Switzerland is fresh out of banks large enough to buy UBS).

As markets open today in the US we will soon see what investors decide to do with bank stocks on both sides of the pond. They will either continue to sell them and pull money out of untrusted institutions, or they will stop, giving the banks a second chance to prove they are sound.

Asia has apparently already delivered its verdict, and it is not a good one.

Through all the turmoil, the underwater investments remain. The exposure to uninsured deposits remains. Depositing $30 Billion in First Republic did not change these things, and neither does the merger between UBS and Credit Suisse. These problems have yet to even be addressed, much less resolved.

Will the merger between UBS and Credit Suisse end the banking crisis? In a word: No.

Gruenberg, M. Remarks by FDIC Chairman Martin Gruenberg on the Fourth Quarter 2022 Quarterly Banking Profile. 28 Feb. 2023, https://www.fdic.gov/news/speeches/2023/spfeb2823.html.

Jiang, E., et al. “Monetary Tightening and U.S. Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?” SSRN, 2023, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4387676.

(2 of 2) There is no precedent for this, because there are far more people involved than during the Great Depression, because they are much more interdependent and because they are much more aware of what is going on all around the world - and because that information now travels in seconds, minutes and hours in unlimited volumes, while in the Great Depression, there was only telegraphs and newspapers.

Then there is increasing destruction from climate change, shortages of hydrocarbon fuels and mining reserves, and surely a massive growth in people escaping one place in hope of moving somewhere better where they are really not welcome, or likely to be highly productive.

In general, people are basing their idea of the future on an over-estimate of everyone else's confidence, solvency and of the real value which exists in capital items and which can be produced by factories, farms and service industries.

The whole collapse will be so pervasive and unprecedented that only the very wealthy will survive without genuine reduction in their living standards, even if they only wind up with 1/10th of the real value they have, or think they have now.

It is impossible for me to imagine any government trying to fix the mounting challenges they face without printing or electronically inventing more currency. We see this in the ability of the Swiss and the US governments so suddenly, within a day or so of heated negotiation, promise tens of billions of whatever currency they print, to supposedly prevent confidence sapping contagion in general, by backstopping this or that bank out of dozens and hundreds of other banks.

They didn't suddenly raise taxes to obtain that currency by tapping the productivity and/or wealth of their taxpayers. They print or electronically create it.

So the government responses are bound to be profoundly inflationary.

What happens when this inflation and the overall reduction in confidence feeds back onto itself to further lower confidence and flood the system with currency? More inflation and more loss of confidence.

What of the dizzying world of finance, with all its entanglements and derivatives? This was a barely stable arrangement when the real value of currency remained fairly stable, but all the assumptions this system relies upon to remain stable disappear with massive inflation and the inability of parties to these loans and derivatives to meet their contractual obligations.

Farms will still produce food - and people always want food. Mines will always be needed, since civilisation depends entirely on mining, as it does on agriculture and manufacturing. Manufacturing will still exist. I just hope that it will continue to work with complex supply chains able to provide all the components needed to make products - and every factory and many high-value products relies on very particular semiconductors and numerous other components. I know, since I make a few electronic products. If you can't get even one component - and connectors, integrated circuits, potentiometers etc. are exceedingly specific and typically come from only a single company, and so factory - you can't make the entire product.

In broad principle I can imagine a subset of banks failing and the rest surviving, in part due to depositors' funds being transferred to the them. However, the whole global economy is so complex, entwined and interdependent that even moderate levels of disruption are likely to drastically reduce manufacturing capacity of numerous products. That is inflationary - a smaller number of products are available and so command a higher real price in terms of other commodities and as measured in currency units.

If all the world used money, rather than currency, a lot of this trouble would have been avoided. Money has intrinsic value, such as a precious metal which is actually needed for production. (Gold's value is largely a social contagion. It is a useful metal but there's plenty of gold metal around without mining any more to meet the needs of electronics manufacturing and jewellery for years to come.) Copper, silver, and numerous engineering and precious metals have real value.

However, how could all money be 100% intrinsic value? Such a large amount of it would need to exist as actual metal, that it would be difficult to move around the place and it would require a massive amount of mining to create this, with that metal being unproductive.

!00% gold or whatever backed paper or electronic currencies are real money, and get around the physical transport problem - but who wants to tie up all that valuable metal in a vault?

Bitcoin started as an honest attempt to do better than fiat currency, but it became, and still is, a speculative craze. Its reliance on hugely energy intensive computations to process transactions and to enable the supply of its currency units to expand without some actor being able to create it at will means that it is a very costly and inefficient currency. It is not even private.

I have never been able to figure out enough about cryptocurrencies to assess the claims of Etherium or whatever to be practical non-fiat currencies.

I can't find a path through my model of the likely future which looks at all optimistic, such as limited damage and not too much social unrest - and this is ignoring the Ukraine war and what China threatens regarding Taiwan. The fact that China would face widespread starvation - and the West extraordinary disruption by not being able to get what China manufactures - is no reason to believe that the CCP wouldn't go ahead with an attack. Putin's invasion of Ukraine is all the evidence we need to establish this.

Don't think that Western leaders are any better. The Biden government's direct or complicit involvement in the Nord Stream pipeline sabotage proves the point Putin tried to weaken NATO and wound up strengthening it enormously. Biden tried to strengthen it and fatally weakened it by showing that even being the strongest NATO ally of the USA is no protection from a crippling and humiliating attack by the USA itself.

US government funded research lead to the creation of the SARS-CoV-2 virus. This could have caused little trouble if everyone had sufficient 25-hydroxvyitamin D to run their immune systems, but instead we got a global pandemic response which lead to tens of millions of people being killed. https://vitamindstopscovid.info/00-evi/ and https://nutritionmatters.substack.com/p/the-covid-19-pandemic-response-killed .

In many respects, governments are run by corrupt nincompoops - and it seems that banks are not much different. So why should we believe that they will handle a real crisis (economic collapse of confidence, for very good reason) in a way which leads to long-term best outcomes?

There is a general feeling that "the authorities" won't allow things to get any worse than some threshold. However, the problems were created by the authorities, clueless and corrupt in direct ways, and corrupted and misdirected by a voting public which itself much prefers cheap short-term fixes over costly long-term solutions.

Please cheer me up if you can!

(1 of 2) My eyes glaze over after considerable effort at trying to understand all this stuff. I can't find any reason here at All Facts Matters or in anything I read at https://zerohedge.com to think that a growing epidemic of bank runs - based on and causing lack of confidence in the ability of all banks to pay back depositors currency - is the inevitable path from here. This is one mechanism by which the economic system can collapse.

This is the start, and other mechanisms will naturally develop as a result. Some involve positive feedback especially in the short term - making them much more rapid, intense and destructive - while perhaps having long-term benefits and stabilising aspects. For instance, lack of economic confidence in US banks and business in general can reduce the value of the USD$ which boosts inflation immediately, but over years enables more real value to be created by manufacturing inside the USA.

The USD$ being a reserve currency has been a long-term curse, since all the US government needs to do is print USD$s and manufacturers, miners, and farmers overseas readily accept this in trade for their real stuff - reducing the ability of US manufacturers etc. to compete. It takes decades to build the skills, infrastructure and factories to recover from this.

The economic system, at every level from companies to countries, is a house of cards with most people and businesses having been in the habit of equating currency with value (not unreasonable since we can trade it for real things of value) and assuming that this level of value will remain stable enough to make ordinary life, business and planning possible.

Inflation weakens that conviction and both inflation and rising interest rates weaken the real value of whatever banks bought as reserves (some types more than others), to meet depositor, shareholder and regulatory expectations that they can firstly firstly remain solvent and profitable and secondly repay depositors' currency even if there is a run on the bank.

Since banks are all tangled up in each other by way of bonds (such as those just erased, as noted above) and derivatives / credit-default swaps (maybe not the same thing, but near enough for this high-level analysis) there's no reason to believe that the banking system is anywhere near as strong or able to pay back depositors' currency as they all pretend and wish to be.

Many companies have huge amounts of debt. Governments have such astronomical amounts of debt that they could never pay it back without strangling their populations and businesses with taxation for a decade or two, which would kill productivity and cause the people to flee to another country. (If they tried, they would soon by voted out or otherwise overthrown, to be replaced by some alternative which also pretends to be able to solve the massive problems, at least for a few years, without extracting massive, real, value from their citizens and businesses).

I don't really understand all this debt. Who is it owed to? The Chinese government has a lot of US treasuries. They are getting ready to fire hypersonic missiles to destroy US aircraft carriers which protect Taiwan. China relies on imports of food, hydrocarbons, coal for electricity and smelting iron AND the great majority of the semiconductors it needs to maintain its extraordinary manufacturing capability. Except for material coming from Russia and a few other land-reachable countries, the flow of semiconductors, food, etc. is by ships and aircraft which would be blockaded the moment China lurched at Taiwan.

Overall, I think governments behave as if they are sound when they are not, that their debt is sustainable, and that they can somehow carry on borrowing and printing currency in a way which firstly delays whatever immediate disaster would occur if they didn't do this AND not make the long-term, inevitable, chaotic correction of all this very much worse.

Many larger companies behave as if their general level of business and so income stream can be relied upon from one year to the next. But, depending on the short-term essentiality of their products or services, this is not the case. Shortage of currency and/or confidence about the future will greatly reduce their business activities and so the real value of currency they earn.

Likewise individuals and families have lots of debt, based on the idea that their jobs will continue and that they will continue to be paid about the same amount of real value.

However, pretty much every individual, company and government is basing their idea of the real and currency unit values of their future income, and of their assets, on the recent past in which the general level of confidence was - and still is - far higher than is justified considering the fundamental problems and the chaotic unraveling, rebalancing, value and confidence destruction which is about to ensue.