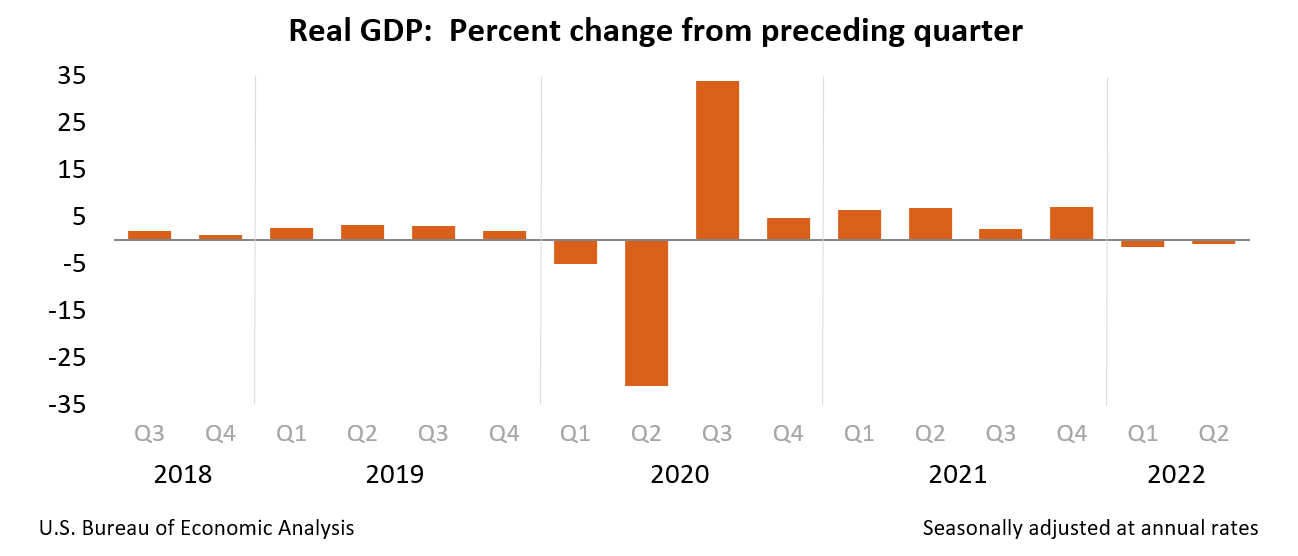

Real gross domestic product (GDP) decreased at an annual rate of 0.9 percent in the second quarter of 2022 (table 1), according to the "advance" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP decreased 1.6 percent.

"Coming off of last year’s historic economic growth — and regaining all the private sector jobs lost during the pandemic crisis — it’s no surprise that the economy is slowing down as the Federal Reserve acts to bring down inflation," Biden said Thursday in a statement. "But even as we face historic global challenges, we are on the right path and we will come through this transition stronger and more secure."

Wall Street: Perhaps Not A Recession (Yet)

Setting aside for now the inherent contradiction in the White House position—that an economy which is “slowing down” is not an economy heading into recession when every definition of recession entails a deceleration of economic activity1—there is no denying that, judging by how stock markets have reacted yesterday and thus far today, Wall Street agrees with the White House.

However, that sentiment is hardly a complete Wall Street consensus, as Treasury yields not only remain inverted, but the inversion2 between 10-Year Treasury yields and 2-Year Treasury yields is increasing, with the 2-Year yields rising even as the 10-Year yields are falling.

This deepening inversion suggests that bond market sentiment on the near-term economic future is more pessimistic than on the longer term—which also cuts against the White House narrative of “slowing down, but not a recession.”

Wall Street may not view the current economic situation as outright recession, but it is far from enthusiastic about the economy’s prospects for expansion in the near term.

Does Main Street Share Wall Street’s Sentiments?

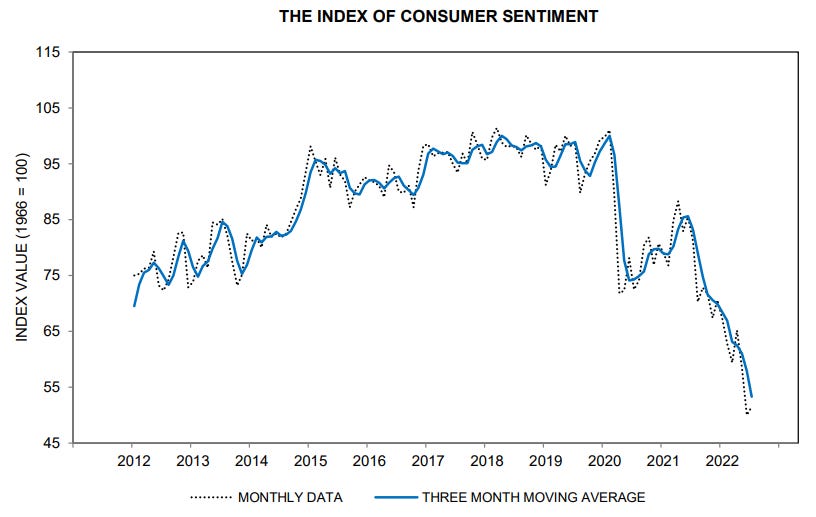

For its part, US consumer confidence has been moving steadily towards the “we’re in a recession” end of the assessment spectrum since early 2021.

Note also that the decline since April, 2021 fits a larger downward trend extending back to the beginning of 2020. For whatever reason (and there is not space here for a full exploration of all the potential reasons), consumers in the US have been turning increasingly more pessimistic about the future of the economy, although that shift may be reaching its own zenith.

Note that the Conference Board survey, like the University of Michigan survey, shows growing pessimism by consumers since last year. Consumer confidence actually peaked in 2018, moderated in 2018 and 2019 before dropping dramatically in 2020, and, after a rebound, resumed a downward trajectory that pre-dates the pandemic, the lockdowns, and the attendant economic disruptions and dislocations. The pandemic at this juncture appears less impactful on future sentiments than media narratives might suggest.

Regardless of what the White House says, however, “Main Street, USA” is saying pretty emphatically that the US is in a recession—and has been for quite some time now.

Sentiment Matters

Why focus on “sentiment”?

While the empirical data tells us in great detail where the economy has been, how consumers, businesses, and investors react to that data as well as economic forecasts invariably creates a feedback loop where the inherent biases each brings to there assessment of economic data pushes future measurements in the direction of the bias.

In his seminal 1936 book The General Theory of Unemployment, John Maynard Keynes used the phrase “animal spirits” to describe the idea that beliefs and views not only matter for decision-making, but also change in ways that are hard to predict and manage. As a longtime business practitioner, I too think of sentiment in this way. I believe our economy’s performance is driven in important ways by the outlook and beliefs of consumers and businesses—over and above what the hard data, and past patterns in it, by themselves would imply. In other words, having the incoming data is one thing, but knowing what consumers and companies think about the road ahead is quite another.

The ability of changes in confidence to directly influence the economy seems intuitive. Consumers who are nervous about their future employment or worried that an imminent stock market correction would wipe out a substantial chunk of their savings might be reluctant to make big purchases and take on new debt. The resulting fall in consumption would then lead to an economic contraction that validates consumers' worst fears. Likewise, businesses worried about changes in regulations or the failure of a hoped-for trade agreement might be reluctant to invest in new projects, driving down productivity across the economy.

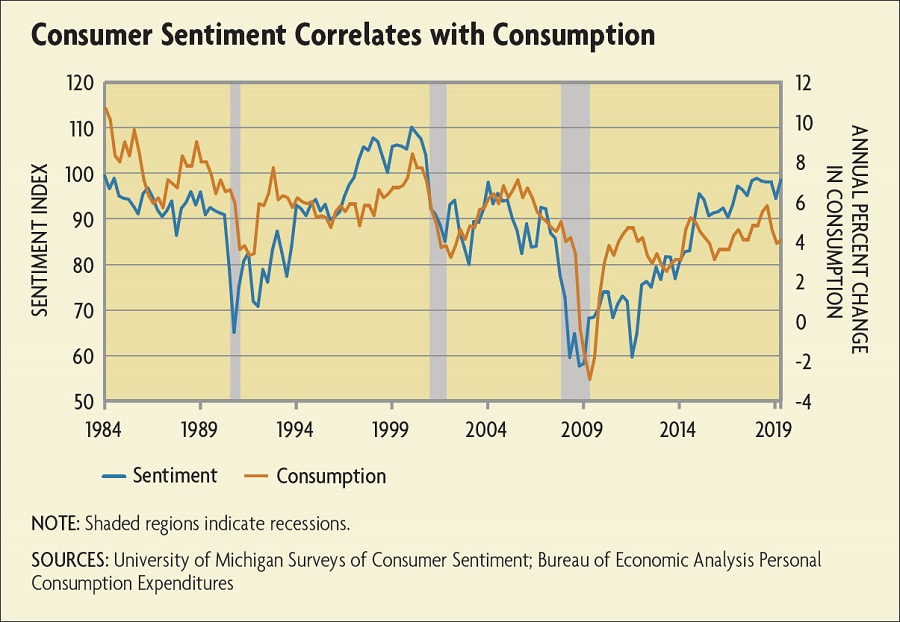

These correlations are readily apparent in the data. Changes in the University of Michigan's Consumer Sentiment Index, which surveys consumers about where they think the economy will be a year from now, generally track changes in consumer spending. (See first chart below.) Likewise, the Conference Board's CEO survey, the Measure of CEO Confidence, largely moves in sync with business investment. (See second chart below.) There is even evidence that seasonal changes in stock market returns are correlated with the change in daylight hours from summer to winter. It seems that stockbrokers get SAD (seasonal affective disorder) too.

What these empirical studies have uncovered is that our speculation is accurate. In response to news shocks, these macroeconomic quantities move in unison: An anticipation of higher future productivity raises consumption, investment, output and the labor supply. Moreover, this is consistent with the intuition outlined above, whereby the wealth affect seems to dominate the intertemporal substitution effect.

Where we think the economy is headed plays a direct role in determining where the economy ultimately heads.

Reading The Tea Leaves: Where Are We Headed Next

Wall Street’s stock market optimism arguably suggests confidence that the Fed will soon moderate its rate hike policies and even reverse them. Whether this is an accurate take on the Fed’s own sentiments regarding current economic data or a misperception of it remains a question, as Morgan Stanley Chief Investment Officer Mike Wilson noted on Wednesday:

“The market has been a bit stronger than you would have thought given the growth signals have been consistently negative,” he said. “Even the bond market is now starting to buy into the fact that the Fed is probably going to go too far and drive us into recession.”

Given that consumer sentiment moved sightly up month-on-month from June in the UMich survey, Wall Street’s optimistic take on how the Fed proceeds from here may not be that wide of the mark. If low consumer sentiment creates sufficient demand destruction to moderate consumer price inflation, the Fed’s own logic reduces the need for future large rate hikes.

The devil in the details is that word “sufficient”. Has enough demand destruction been imposed to push consumer price inflation down?

The Cleveland Fed’s inflation nowcast is showing a slight easing in consumer price inflation, from 8.89% to 8.82% year-on-year. Depending on how close the nowcast comes to the final July number (for May and June the nowcast undershot the final figure by about 0.5%), peak inflation could be at hand.

At the same time, FreightWaves is noting that container ship backlogs at the nation’s ports are back at levels last seen in January and February, indicating a fresh supply chain bottleneck is building, which will push inflation still higher in spite of demand destruction to date.

In January and February, when North American congestion previously peaked, there were just under 150 container vessels waiting off the coastlines. Two-thirds were in the Los Angeles/Long Beach queue.

As of Thursday morning, there were 153, the majority off East and Gulf Coast ports. Whereas the earlier West Coast pileup was centralized, highly publicized and relatively easy to track, today’s ship queue is more widely disbursed and attracting less attention.

The container ship backlog has not gotten the attention it has in the past, which could mean Wall Street has not fully priced its impact on inflation. In turn that means Wall Street has still not fully priced in future Fed rate hikes.

The container ship backlog also underscores the reality that Wall Street and consumer sentiment both have to constantly respond to constantly shifting forces. Consumer sentiment suggests that inflationary forces to date are fully factored in—i.e., we are at or near “peak inflation”—but new inflationary forces remain a possibility, and in this case a probability. Consumer sentiment has not yet accounted for those.

While both Wall Street and consumer sentiment are ready to be done with inflation rises and interest rate hikes, inflation is likely not yet done with either Wall Street or consumers. The recession is still going to get deeper from here.

The precise standard used by the National Bureau of Economic Research states that a recession begins at the peak of an economic cycle and ends at the trough. The other metrics devised in 1974 by Julius Shiskin included a 9-months-plus decline in non-farm employment and a 6-month decline in employment in at least 75% of all economic sectors. Investopedia defines recession as “a significant, widespread, and prolonged downturn in economic activity.“ Every definition thus involves at least one dimension of declining economic activity.

Investopedia: “An inverted yield curve describes the unusual drop of yields on longer-term debt below yields on short-term debt of the same credit quality. “