What Commodity Price Changes Can Tell Us About Future Inflation

Not Every Price Drop Means Peak Inflation

The hopium in the corporate media that “finally” we may be past peak inflation has been pretty rampant this past week. The latest “sign”, or so we are told, is that the broad drops in commodity prices are a sign that the worst of the rise in inflation may be behind us, and that inflation is due to decline very soon.

From the Wall Street Journal on July 4:

“Moderating commodity prices are clear evidence that inflation is cooling,” said Louis Navellier, chief investment officer at Reno, Nev., money manager Navellier & Associates.

From News.AM on July 7:

Despite ongoing supply disruptions, prices for everything from gasoline to wheat are falling on concerns that a stagnating global economy will weigh on demand. This may be of some help in the fight against high inflation in many countries, Bloomberg reported.

From the Globe And Mail on July 8:

As inflation rates climb to multi-decade highs across the world, some of the biggest drivers of consumer-price growth have entered a new and welcome phase: Their prices are actually declining.

Does the data really bear that out? Are commodity prices a reliable indicator, leading or trailing, of inflation trends? Unfortunately, the linkage is less precise than the media wants you to believe. The falling commodity prices are not a signal of “peak” inflation.

Are Commodities A Cause Of Inflation?

One of the enduring battles of dueling narratives within practical economics is the contention that commodities either do or do not “cause” inflation. As is generally the case when narratives collide, the facts frequently get left behind.

One of the leading advocates for the “do not” thesis, Daniel LaCalle, Chief Economist at European investment management firm Tressis SV, states flat out that…

Rising prices are always caused by more units of currency being directed to scarce or tangible assets.

Unfortunately for Mr. LaCalle, having “more units of currency” for purchasing scarce quantities of goods only results in rising prices if the quantities of those goods remains the same. However, a price rise also happens when the units of currency remain the same but the available quantities of goods decreases. The implicit predicate in his thinking of a steady state—”all things being equal”—is only true in the hypothetical, and is frequently false in the real world. All things are rarely kept equal, and, from the oil shocks of the 1970s to the supply chain dislocations of the present day, we have several examples of the available quantities of particular goods being reduced, triggering price increases.

That is the essence of what a “supply shock” is.

To understand the flaw in his thinking, recall for the moment the basic monetarist equation:

MV == PQ

Where M == money, V == money velocity, P == Price, and Q == Quantity of goods being bought or sold.

What Mr. LaCalle asserts, which is correct as far as it goes, is that if M is increased while Q and V are held constant, then P will also increase. Thus, from his perspective, the “root cause” of inflation is excess money printing by the world’s central banks. Unstated but implied in his thesis is that there has been no change in either Q or V, and therefore the massive monetary stimulus applied during the pandemic lockdowns is the only source of the current inflation.

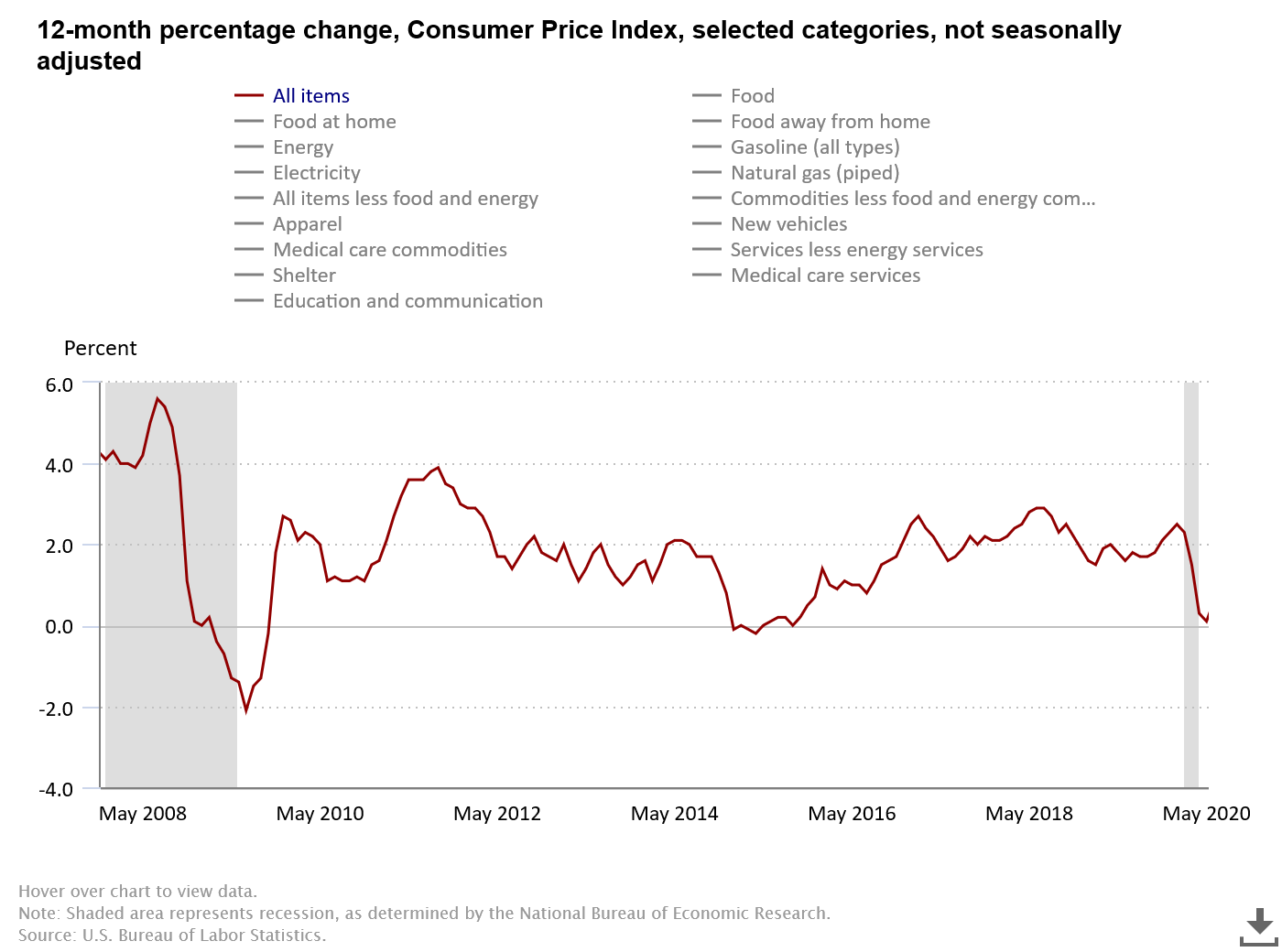

However, history is not on Mr. LaCalle’s side, given that the rampant money printing in the wake of the 2008 Great Financial Crisis did not result in rampant consumer price inflation. For the most part, consumer price inflation between the 2008 recession and the 2020 pandemic lockdown-induced recession trended largely horizontally, fluctuating up and down by a couple of percentage points but establishing no clear upward trend.

It is worth noting that this observation holds true even if we look at the alternate CPI metrics and charts from ShadowStats.

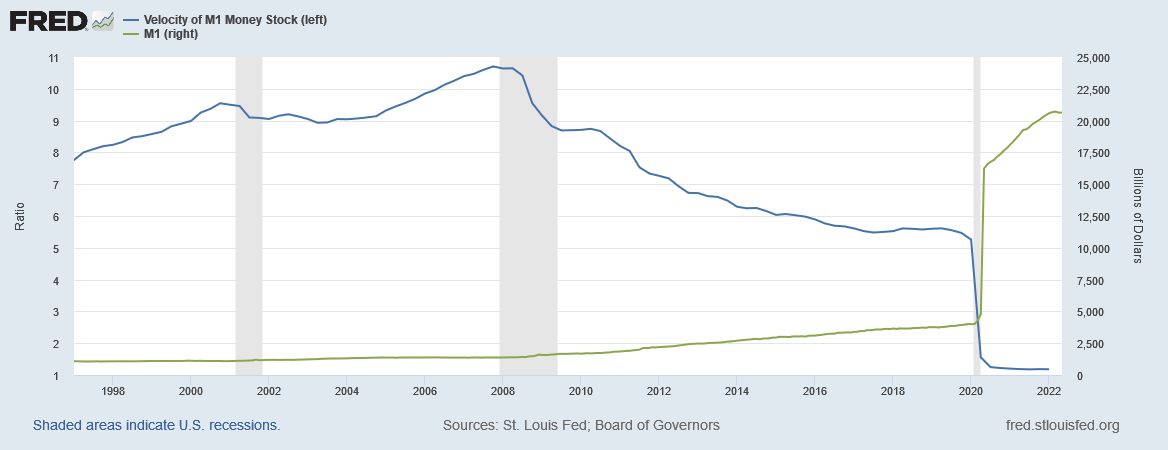

This happened while the Federal Reserve was greatly expanding the M1 money supply—and while the velocity of that money was steadily dropping.

What Mr. LaCalle forgot to take into consideration was that, for a constant quantity of goods Q, an increase in price requires that the product money times velocity (MV) increase. Not only does this mean that consumer price inflation can result from an increase in money velocity, it also means that a decrease in money velocity can offset an increase in money supply—which is, broadly speaking, what happened in the wake of the Great Financial Crisis. Money supply expanded, but because less and less of it actually circulated, the inflationary effects of that increase were effectively negated.

Thus, even after the massive increase in the M1 in the wake of the pandemic lockdowns, consumer price inflation could not result strictly from that increase, because at the same time the velocity of that money dropped to near zero.

The assertion that inflation is simply the result of too much money in circulation is an oversimplification.

Arguing the causal link between commodities and inflation is, among others, Kevin Kliesen, Business Economist with the Research Division of the St Louis Federal Reserve, who asserts that…

The linkage between commodity price changes and the changes in prices that consumers pay for goods and services is intuitive: If the price of steel increases, consumers will pay more for durable goods such as motor vehicles and appliances, which will tend to lift the measure of inflation that the Fed targets (the personal consumption expenditures price index, or PCEPI).

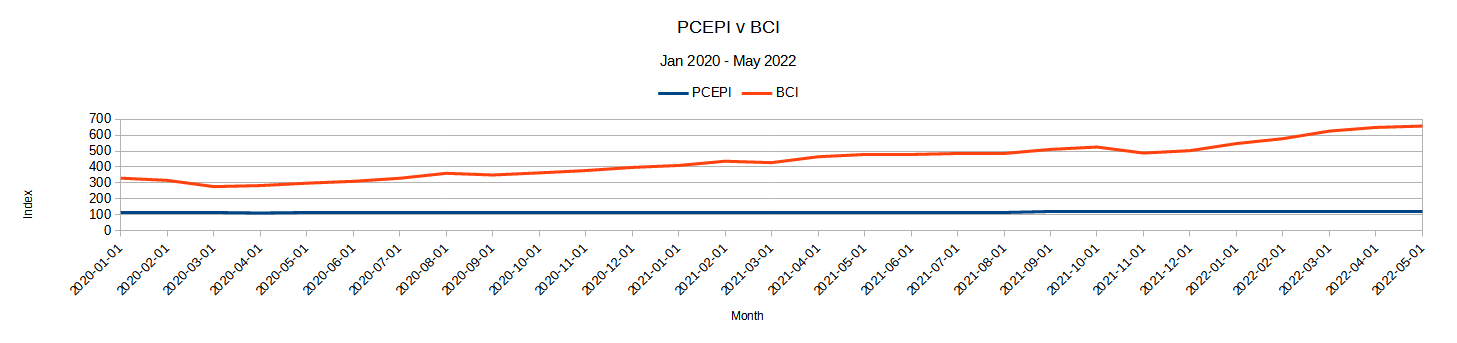

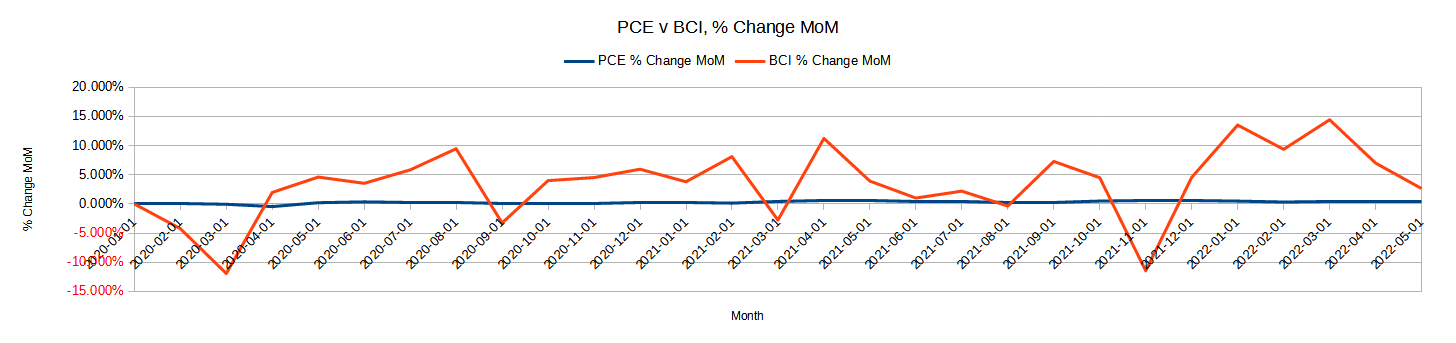

Perversely, the data does not actually support that assertion either. While the correlation between the PCEPI and one of the commodity indices Mr. Kliesen cites, the Bloomberg Commodity Index, does appear to be quite strong at a correlation coefficient of 0.9697 (1 being perfect correlation), the same does not hold true for the correlation between the percentage changes of either index, either on a month-on-month basis (0.3276) or a year-on-year basis (0.3924). This is intuitively obvious when the two indices are placed on the same graph:

While rises in either index are matched by rises in the other index, the magnitude of the rises varies significantly.

Consequently, commodities, while unquestionably linked to inflation, despite Mr. LaCalle’s assertions, that linkage is far broader and not nearly as precise as Mr. Kliesen appears to present.

What we have to remember about the current inflation trend is that, contrary to the implicit assumption of Mr. LaCalle, Q in the equation above is not held equal in the current situation, but is in fact greatly reduced. A simple bit of algebra suffices to show that if Q is reduced, while M and V are held constant, P must increase then also. Between the results of global pandemic lockdowns, and the disruptions to the flow of goods and grain out of the Black Sea as a result the Russo-Ukrainian War, in several commodities Q has been suddenly and dramatically reduced.

Thus, even though the money supply greatly expanded after the pandemic lockdowns, the, another major driver of prices of particular goods is the steep decline in the availability of various commodities which are the raw inputs for those goods.

Both narratives are, to a large degree, simply inaccurate. The amount of money in circulation does drive consumer price inflation, but the availability of commodities and other inputs—which availability is broadly indicated by price changes—also drives consumer price inflation. At the same time, money supply increases which are offset by decreases in money velocity are going to have little or no impact on inflation.

Understanding inflation requires that all of these factors be considered accordingly. Focusing on just one—the logical error of both sides of the “root cause of inflation” debate—paints an inaccurate picture of the situation.

Prices Measure Both Availability And Demand

Because of the relationships between money supply, product (or commodity) price, and product (or commodity) quantities bought and sold defined by the equation above, it is immediately clear that price measures both availability as well as demand for products and commodities. Price discovery occurs when fluctuations in both demand (MV) and availability (Q) are resolved, resulting in a price P.

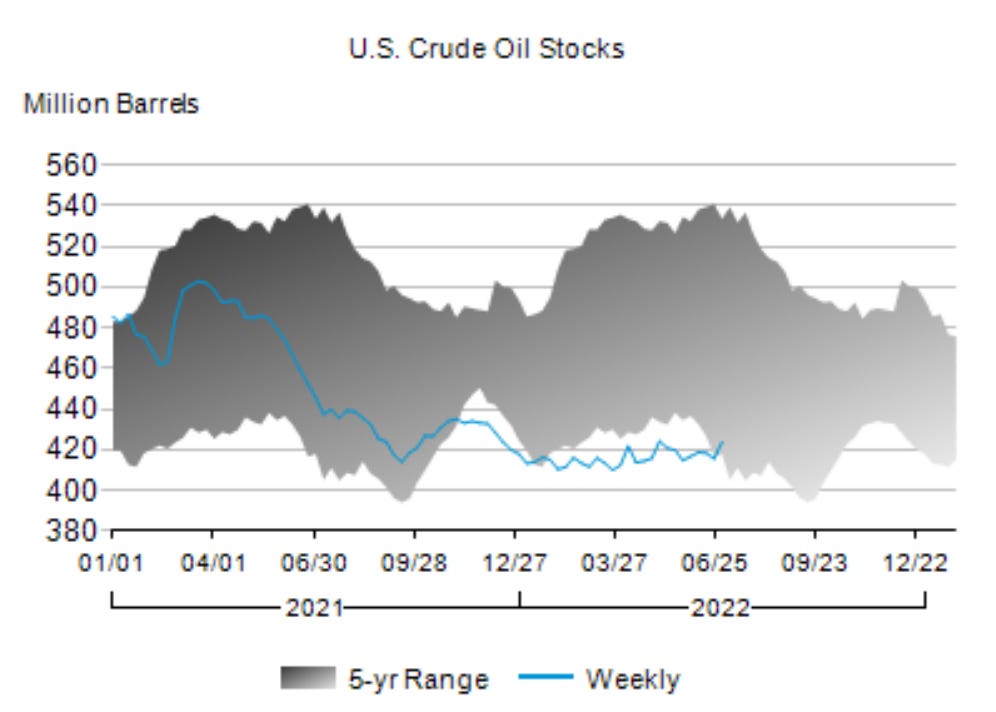

To illustrate this, let us consider the fluctuations in the price of crude oil (West Texas Intermediate) through 2021 and 2022 to date.

Money supply and demand variables alone cannot explain all the fluctuations in the price of oil over this time period, because the spike in price March of this year was not accompanied by a sudden influx of new money. Rather, the likely driver of that price spike was the Russo-Ukrainian War and its disruptions of Russian oil exports—i.e., a decrease in supply. Q dropped (or, more precisely, was anticipated to drop), and thus price rose accordingly.

This also tracks with oil supply data provided by the US Energy Information Association, which monitors oil inventories in the United States.

The long-term rising trend in crude oil price is matched by a long-term decline in crude oil supply. If we presume the March spike in crude prices was driven by fears of a supply shock, the leveling out of crude inventories arguably ameliorates that concern, and thus by May the price was more in line with the long term rising trend.

By the same token, the ending of pandemic lockdown restrictions and the resumption of demand are not clearly indicated by the rise in oil price. By 2021 the large spike in money supply had already occurred, and if the price rise were solely the result of that spike, the rise in crude oil prices would be far more abrupt and front-loaded than we are seeing.

Note that crude oil prices have dropped in recent weeks, and crude inventories have risen somewhat—although it would be premature to argue there is a long-term trend of building up oil inventories at this juncture.

Does this indicate that demand for oil is diminishing? At a minimum, demand relative to available supply appears to be dropping. A sustained drop in crude oil price would be indicative of the demand destruction sought by the Fed with its interest rate hikes, particularly if not matched by corresponding inventory increases in crude oil.

Commodity Prices Tell Us About Demand Relative To Available Supply

As is the case with crude oil, so it is with all commodity prices: they tell us about demand relative to available supply. The availability dimension is important to remember because, as we can see just by looking at the continued congestion at the nation’s freight terminals, there are considerable supply constraints for a number of goods as well as a few commodities.

There were 125 container ships waiting off North American ports on Friday morning, according to an analysis of ship-tracking data from MarineTraffic and queue numbers from California.

That’s down 16% from 150 waiting ships in January, when West Coast congestion peaked, but up 36% from 92 ships a month ago.

Those supply constraints drive Q down in the monetary equation, which pushes prices up at all levels of demand (MV). As I commented on my Minds channel, significant progress on consumer price inflation will require the container ship backlog at the nation’s ports be overcome as well—and it has not been.

In order to overcome inflation, demand destruction has to be of sufficient magnitude to overcome the inflationary pressures of constraints on Q.

The question regarding commodity prices is not if recent declines represents demand destruction—it would be difficult to interpret any sustained decline in commodity prices as anything else, given the aforementioned supply constraints—but whether there is sufficient demand destruction to overcome those supply constraints as well. How large those supply constraints might be is not information that can be captured solely by price, which can only summarize demand relative to whatever supply is available after accounting for the effects of those supply constraints.

Accordingly, commodity prices are problematic as a leading indicator on inflation. Because of the dueling forces of both demand and availability, commodity prices do not, in and of themselves, provide a reliable predictor of when peak inflation will be reached. At most, falling commodity prices suggest a slowing of the increase in the rate of inflation, not proximity to "peak inflation” after wish disinflation will set in.

Much as with falling rents in various US markets, falling commodity prices do not signify the beginning of the end on inflation. They may indicate we are getting close to the end of the beginning.

Falling commodity prices give us hope on inflation. They do not give us anything more substantial than that. They certainly do not provide assurance that peak inflation has been reached, or even is about to be reached. The corporate media narratives in this regard are simply wishful thinking.