What Does The Fed Do Now?

One Dollop Of Economic Good News Sheds Little Light On What The Fed Does Next

Wall Street’s bulls were positively ecstatic by yesterday’s surprise CPI print showing headline consumer price inflation declining to 8.5% in the month of July, rising sharply yesterday and continuing this morning.

On Wednesday, the Dow Jones Industrial Average DJIA, 0.89% rose 535 points, or 1.63%, to 33310, the S&P 500 SPX, 0.95% increased 88 points, or 2.13%, to 4210, and the Nasdaq Composite COMP, 1.04% gained 361 points, or 2.89%, to 12855. The S&P 500 is up 14.8% from its 2022 closing low hit in mid-June but remains down 11.7% for the year to date.

Wall Street is clearly celebrating the Fed’s “win” over inflation. But is it celebrating too soon? More than likely.

The Fed Is Still Pushing Rate Hikes

Although Wall Street is anticipating a softer Fed stance on interest rates, the Fed itself has been quick to downplay such expectations, with Chicago Federal Reserve President Charles Evans talking up further rate increases.

With consumer prices unchanged last month compared to June, but up 8.5% from a year earlier, inflation is still "unacceptably" high, and the Fed will likely need to lift its policy rate, currently in the 2.25%-2.5% range, to 3.25%-3.5% this year and to 3.75%-4% by the end of next year, Evans said.

With only three meetings left in 2022 in which to raise interest rates, for the Fed to reach Evans’ year-end rate target, at least one rate hike of 50bps or more is mathematically necessary, which reduces the likelihood of only a 25bps rate hike any time soon.

Even before the CPI Summary came out, Clevelend Federal Reserve President Loretta Mester cautioned against making too much of a drop in inflation over a single month.

So, again, we might see goods inflation and commodities inflation come down but at the same time see the services side--I said "supply side"--I meant services side of the economy, right, stay up and that's what we got to keep watching for. So, and that's when I say compelling evidence. It can't be just a one-month oil prices went down in July, that will feed through to the July inflation report, but there's a lot of risk that oil prices will go up in the fall. It's got to be sort of a sustained, several months of evidence that inflation has first peaked--we haven't even seen that, yet--and then, is moving down.

The cautionary notes arguably are somewhat prescient, as commodity prices, especially for oil and gasoline, rose on the day yesterday, along with gold, silver, and copper.

Are Rate Hikes Even The Answer?

However, the Federal Reserve is facing an even greater question about its rate hike policies, although it probably does not realize it—the rate hikes may not be having much if any influence on inflation at all.

That the Fed can corral inflation through interest rate manipulations is considered almost axiomatic in economic and finance circles, and is certainly taken as an article of faith by both the corporate and alternative media. So ingrained is this principle, that, with consumer price inflation running at 8.5% even Wall Street has conceded that there will be interest rate hikes still to come.

It will come as something of a surprise to many, therefore, to learn that the correlation between interest rates and inflation is a good deal less certain than the prevailing wisdom suggest.

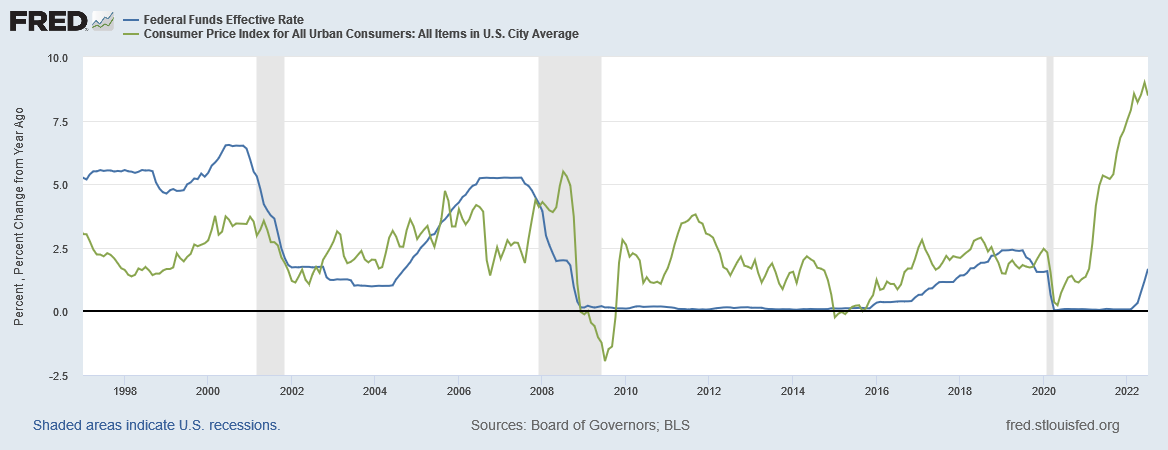

A comparison chart between the Federal Funds Rate and Year-on-Year change for inflation shows a rather low level of correlation between the interest rate and consumer price inflation, particularly since 2020.

Nor is the visual representation deceiving. A computation1 of the correlation coefficient2 between the monthly measurement from 1997 through to the present of the Federal Funds Rate and year-on-year consumer price inflation yields a rather low value of 0.22516. The covariance3 between the Federal Funds Rate and inflation is similarly low at 0.325.

While there is a relationship between the Federal Funds Rate and inflation, it is far from a certain one.

The correlation coefficient rises if one focuses on the past 24 months (correlation coefficient 0.50494), and even more so if one focuses on the past 12 months (correlation coefficient 0.60543). However, the covariance declines both in the 24-month analysis (0.55947) and in the 12-month analysis (0.37957).

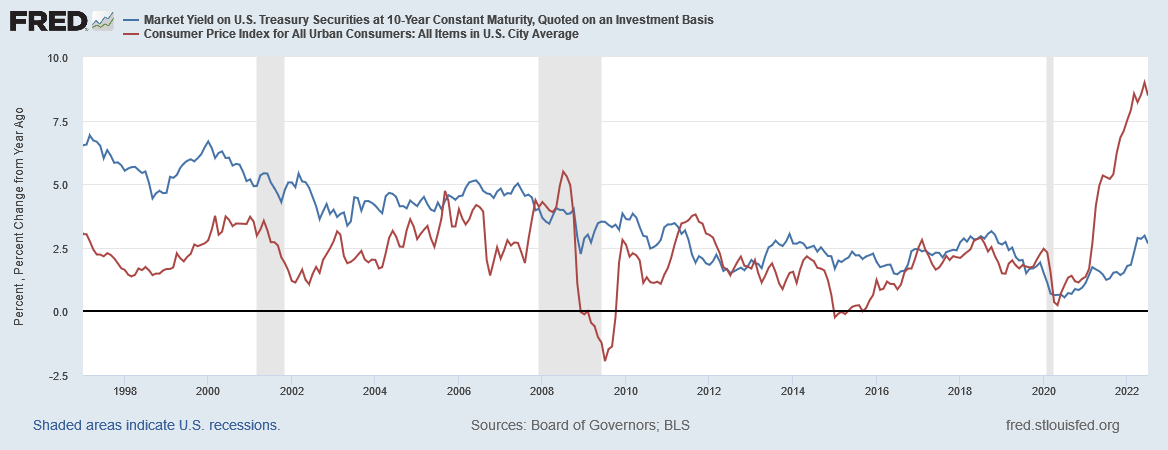

The situation is largely the same if we consider the 10 Year Treasury Yield against consumer price inflation, although the relationship between interest rates and inflation is in this instance more defined.

Analyzing monthly yield and inflation values since 1997 gives a correlation coefficient of 0.12957 and covariance of 0.31008. Narrowing the focus to the past 24 months yields a correlation coefficient of 0.83598 and covariance of 1.55567. However, when the focus narrows again to the past 12 months, while the correlation coefficient rises slightly, to 0.85589, the covariance drops significantly, down to 0.64287.

While there is clear correlation between interest rates and inflation, interest rates are demonstrably less impactful on consumer price inflation than the Fed’s prevailing narrative would suggest, and raising the Federal Funds Rate has been at most only minimally impactful on inflation. There is ample room for other factors (i.e., fluctuating availability of supply) to have far greater impact on inflation than raising interest rates via the Federal Funds Rate.

Even an examination of Treasury Yields and inflation during the 10 years encompassing the Volcker Recession shows a low correlation between the two entities (correlation coefficient 0.26624), although the correlation is higher than since 1997 and the covariance over that same time frame is considerably higher than now (2.28454).

However, the Federal Funds Rate over the same period was significantly more impactful on inflation, with a correlation coefficient of 0.61133 and covariance of 8.01020.

Interest rates might be the primary weapon against inflation in the Federal Reserve’s arsenal, but that is hardly the same as saying interest rates are an highly effective weapon against inflation. At a minimum, interest rates have become significantly less effective against inflation than during Paul Volcker’s tenure.

Were Interest Rates Set Too Low?

These few graphs are hardly sufficient analysis to establish clear relationships of cause and effect, but it is perhaps noteworthy that, for most of the time since the Volcker Recession, both the Federal Funds Rate and the 10 Year Treasury Yield have been largely higher than the rate of consumer price inflation as measured by the CPI.

It was immediately prior to the 2020 recession that Treasury yields were allowed to fall below the rate of inflation.

Is this the reason raising interest rates is apparently less effective now than in the past? While the data here does not prove that absolutely, it does make the inference quite attractive. If that should be the case, then the Fed is effectively impotent against inflation, as to restore the potency of interest rates in that regard the Federal Funds Rate and 10 year Treasury Yields would both have to rise above 8.5%—a magnitude of increase that may be unattainable in the current economic and financial climate.

Jay Powell Cut His Own Throat In 2019

If interest rates are simply too low to be effective against inflation, then Jay Powell cut his own throat in 2019 when he caved to the markets and lowered interest rates back down towards the zero bound. While Bernanke had set the Federal Funds Rate below inflation, and Janet Yellen had continued that policy, Treasury yields largely stayed above the inflation rate until 2019. It was only after Powell buckled on rates then that Treasury Yields slipped below inflation, where they have stayed ever since.

While it is problematic whether the Fed can raise rates sufficiently to be impactful against inflation, it is highly likely that the Fed needs to pursue higher interest rates as a matter of policy, just to have a hope of eventually getting Treasury yields above the rate of consumer price inflation. When interest rates are above inflation, there is some indication they act as a bulwark against inflation, and keep a rising inflation trend from taking hold in the economy; for that reason, it is an imperative that the Fed get interest rates above inflation—not just with a mind towards ending this inflation but also towards preventing future inflation.

While it remains debatable whether Powell can achieve any good on inflation with further rate hikes, it is quite certain that the one thing Powell should not do is lower interests again for any reason. Only by keeping rates elevated can the Fed hope to be in a position to put a cap on inflation once the pace of consumer price inflation has fallen back to its historical norms.

Wall Street is hopeful that the Fed will ease up on interest rate hikes soon, as a result of falling inflation numbers. What Wall Street fails to realize is the Fed may no longer have the option of “easing up”. Rate hikes may be the norm for the foreseeable future, no matter what inflation does.

Statistical calculations performed using the Statistics Toolset embedded into LibreOffice Calc 7.3.3.2.

Weisstein, Eric W. "Correlation Coefficient." From MathWorld--A Wolfram Web Resource. https://mathworld.wolfram.com/CorrelationCoefficient.html

Weisstein, Eric W. "Covariance." From MathWorld--A Wolfram Web Resource. https://mathworld.wolfram.com/Covariance.html

I was especially interested in your chart of CPI vs Fed Funds rate because I had done a similar comparison of the US dollar versus gold.

Many suspect that a higher dollar means a lower gold price, in other words, an inverse relation, but, as in your chart, no obvious correlation.

Reality is complex.