2023 Was A Good Economic Year...Or Was It?

Depends On How Much You Love Government Spending

The Bureau of Economic Analysis has issued their advance estimate for GDP growth in the fourth quarter of 2023. Unsurprisingly, the BEA found yet another quarter of “strong” economic growth.

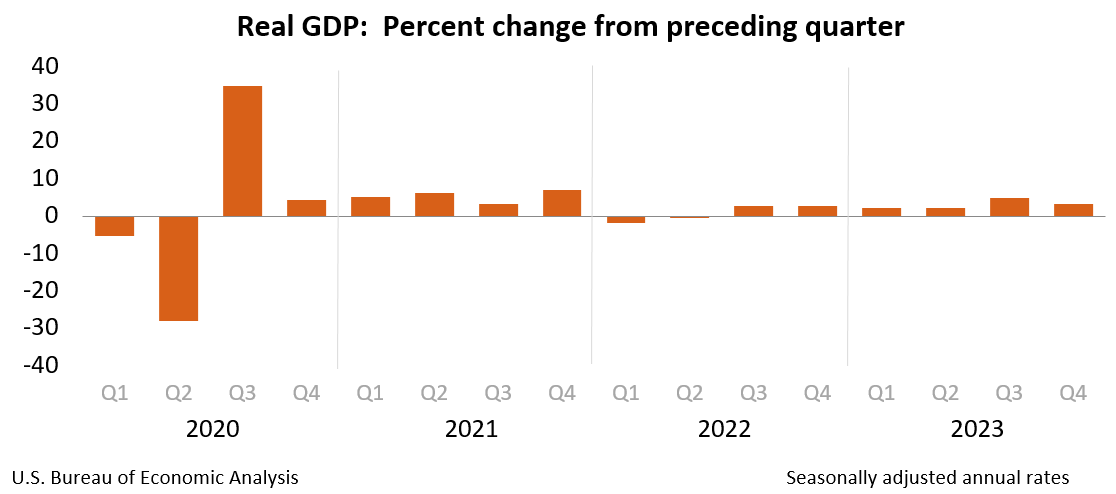

Real gross domestic product (GDP) increased at an annual rate of 3.3 percent in the fourth quarter of 2023 (table 1), according to the "advance" estimate released by the Bureau of Economic Analysis. In the third quarter, real GDP increased 4.9 percent.

For the full year 2023 also is being touted as a marked improvement over 2022.

Real GDP increased 2.5 percent in 2023 (from the 2022 annual level to the 2023 annual level), compared with an increase of 1.9 percent in 2022 (table 1). The increase in real GDP in 2023 primarily reflected increases in consumer spending, nonresidential fixed investment, state and local government spending, exports, and federal government spending that were partly offset by decreases in residential fixed investment and inventory investment. Imports decreased (table 2).

Naturally, all of Wall Street’s “experts” were caught quite off guard by these numbers. Q4 was not supposed to be nearly that good.

When we peel back the layers of data, we find that—surprise!—Q4 was not that good, nor was 2023 as a whole?

What makes the headline numbers look so good? Government spending.

On the surface, the BEA numbers certainly sound good, and come in well above what Wall Street forecast would be the case:

Gross domestic product increased at a 3.3% annualized rate, according to the government’s preliminary estimate out Thursday. For all of 2023, the economy expanded 2.5%.

The economy’s main growth engine — personal spending — rose at a 2.8% rate. Business investment and housing also helped fuel the larger-than-expected advance last quarter.

A closely watched measure of underlying inflation rose 2%, the Bureau of Economic Analysis report showed.

Even alt-media treatments of the data recognize a fundamental problem for the Fed’s rate strategy: the numbers appear to be “too good”.

Gross domestic product, the government’s broadest scorecard for the economy, rose at an inflation-adjusted 3.3 percent annual pace in the fourth quarter.

Economists had been expecting the economy to grow at a two percent pace in the October through December period. Even the most bullish forecasts saw just 2.5 percent growth in the fourth quarter.

After adjusting for inflation, the economy grew at a 4.9 percent pace in the prior quarter.

Measured from the fourth quarter of 2022 to the fourth quarter of 2023, real GDP rose 3.1 percent.

The rapid pace of growth in the fourth quarter could upend expectations for Fed cuts early this year. Fed officials have said that they think the economy will need to grow “below trend”—around 1.8 percent—for a period of time for inflation to sustainably fall to the central bank’s two percent target.

However, Breitbart’s assessment of the numbers does highlight that the main source of the seeming strength is government spending.

Government spending rose 4.3 percent last year after adjusting for inflation. Compared with the prior quarter, government expenditures were up 3.3 percent in the fourth quarter, a slowdown from the quarterly rate of growth of 5.8 percent in the third quarter.

Federal government spending rose four percent in 2023, including a 4.7 percent rise in nondefense spending and a 3.3 percent rise in defense spending. State and local government spending climbed 4.5 percent.

Thus any sober assessment of the BEA report has to consider the impact government spending has on the broad numbers.

One thing that must be noted about 2023—GDP growth is a fairly easy metric to apparently hit because of how little growth actually occurred in 2022.

With even the official estimates for “real” GDP—GDP adjusted for inflation using the government’s own deflator factors—show almost no GDP growth in 2022, any rise in real GDP for 2023 is going to look good by comparison.

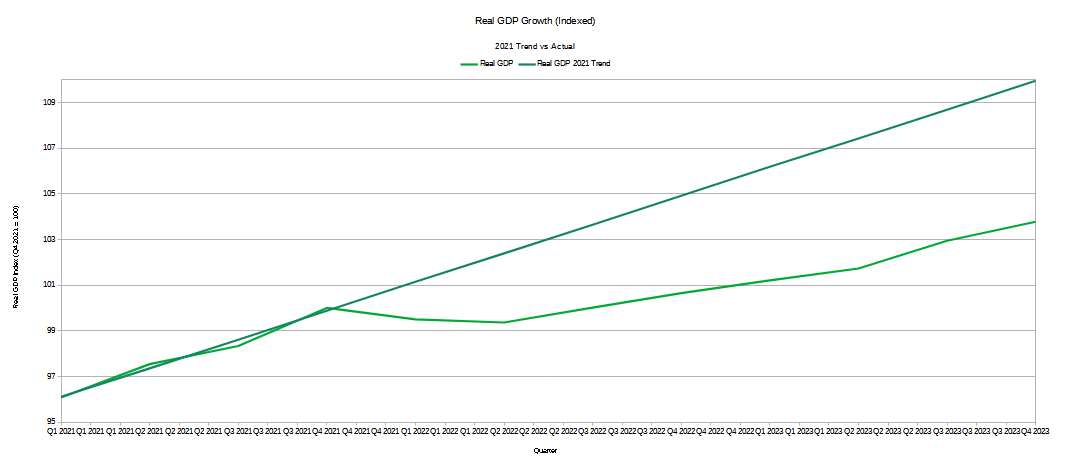

However, if we index GDP and real GDP to the fourth quarter of 2021—the high point before real GDP retreated for two consecutive quarters (a “technical” recession)—we find that real GDP has only risen 3.8% since then.

Real GDP as of Q4 of 2022 is almost exactly the same as real GDP as of Q4 2021. Even by the generous metrics used by the BEA, by Q4 of 2023, real GDP is not anywhere near where it would have been had the trend of 2021 persisted.

In a very “real” sense, not only has there not been any actual “growth” in the economy, we have not even recovered to where the economy should have been if just the performance of 2021 been continued.

Thus even the headline numbers put out by the BEA are not anything to be excited about. The economy is still losing ground, and still losing steam.

Admittedly, if we look at just the year on year change in various elements of Gross Domestic Product over 2023, real GDP growth does appear to look good.

However, even at just the year on year change, we see that private domestic investment growth is extremely weak, and was even negative for the first two quarters of 2023, the continuation of a trend from the 4th quarter of 2022.

It’s when we look at the percentage change in these elements that we begin to see where the substantial economic growth is taking place: government spending.

Government spending persistently had the highest level of relative growth throughout 2023.

This is what the Bureau of Economic Analysis counts as economic growth: the government spending more taxpayer dollars.

When we look into the composition of that government spending of taxpayer dollars, there are more problems to be seen.

Notionally, private consumption indexed from the first quarter of 2021 (the beginning of Dementia Joe’s Reign of Error) outpaced government consumption, and federal defense and non-defense consumption spending actually declined.

However, that performance relies heavily on rises in private consumption in 2021. If we reindex to the first quarter of 2022, federal government consumption spending growth outpaces private consumption spending growth, and state consumption spending growth is roughly the same as private consumption spending growth.

Government spending growth has been the primary engine of GDP “growth” for most of the past two years.

If we delve into the investment categories, we can see why government as a driver of GDP growth is a problem.

If we index to the first quarter of 2021, federal nondefense investment shows the largest level of relative growth, with federal defense investment beating out private investment for second place.

Again, however, this relies primarily on the 2021 growth performances. If we reindex to Q1 of 2022, private investment growth is persistently in the negative, while state and local investment, federal nondefense investment, and federal defense investment, all chart significant growth.

When the economy shows shrinking private investment, that means the economy is shrinking. Without private investment future economic potentials are by definition foreclosed. Government “investment” by definition is a reflection of government spending priorities, enacted through the expropriation of taxpayer dollars.

Anyone uncertain what government spending priorities do to an economy need only look at the ongoing collapse in China, where the economic data keeps getting worse.

With government spending driving US economic growth, it is not a question of if a similar fate will befall the US economy, but when.

Readers will recall that last month’s Producer Price Index summary effectively predicts that this outcome is not that far off.

This is the “strong” economy produced by Dementia Joe’s “Bidenomics” fustercluck. Shrinking investment, slowing consumption spending, stagnating fundamentals.

This is what the Federal Reserve is likely to tout as its hoped-for “soft landing”.

Meanwhile, ordinary working men and women are still grappling with consumer price inflation that stubbornly remains well above the Fed’s Holy Grail figure of 2% year on year.

The BEA and Wall Street might consider this to be a “strong” and “resilient” economy. The Federal Reserve might even congratulate itself for having engineered the nearly impossible “soft landing” from its inflation fight.

However, this is only true if you consider government spending to be the equivalent of private sector spending for both consumption and investment. Given that government spending can only take place by taking taxpayer dollars away from private sector spending, that presumption is absurd on its face.

Such is the state of the US economy at the end of 2023: a state of utter absurdity.

Yes - ‘absurdity’ is the word for it! And there’s going to be such a reckoning for this absurdity.

In the past several decades, the field of economics, with all the fancy econometrics and so on, has strayed too far from the basics. A healthy economy is the result of private investment and PRODUCTIVITY - output per man-hour of work. Government spending essentially just redistributes, and increases the debt. How can they all be so blind!

Hey, on an unrelated note, Dr. Robert Malone posted his weekly “Friday Funnies’ column an hour ago, in which he included a couple of pro-Texas comics regarded your border stance against the Feds. I posted a one-sentence comment, “I stand with TEXAS!”, and the ‘likes’ have been rolling in by the dozen ever since. I believe nearly everyone who reads Malone’s Substack is agreeing with your principled stance. God bless you courageous Texans!

"This is what the Bureau of Economic Analysis counts as economic growth: the government spending more taxpayer dollars."

If so, the BEA is definitely missing something. A huge portion of money spent is supplied from borrowings, not taxes. The deficit's growth is an important engine of so-called economic growth, and the amt reported as growth is, in fact, an indicator of redistribution, too, which is growing exponentially, like the dedicit.

Last week I happened to vsit the CBO's web site when checking another writer's alarmist claim about the budget deficit. I noticed that the deficit in the 1st qtr of FY 2024 had increased by about 21% from the same qtr of the prior FY. If that rate for the 1st qtr were constant (admittedly unlikely), the deficit would double in 3.6 yrs and triple in about 5.75. This situation is absurd.

Much of this redistribution and so-called growth goes to the plutocracy and to wealthy foreigners who own corporate beneficiaries of government borrowing. Another large portion goes to people who are far more likely to vote for D than for R. It's no wonder then that the middle class is being squeezed hard, but it's being squeezed by the uniparty, esp. the varsity faction, which is in charge of the Great Replacement, too.