Are Higher Interest Rates Even Possible?

The Not Quite So Odd Impotency Of Central Banks

If the IMF is to be believed, eventually the world of finance will return to the low interest rates that have been the norm since the 2008 Great Financial Crisis.

Though rates are high now as major central banks battle inflation, "when inflation is brought back under control, advanced economies’ central banks are likely to ease monetary policy and bring real interest rates back toward pre-pandemic levels," IMF analysts said in research released as part of the latest World Economic Outlook.

Of course, the key word here is “if”. As with the rest of the world’s economic institutions, one does well to take the IMF’s pronouncements about the state of the world economy with several grains of salt and a double dose of skepticism.

Yet as central banks worldwide struggle to contain rising consumer price inflation, we are increasingly seeing an odd phenomenon: interest rates are not rising, despite the best efforts of the central banks to push them higher.

Certainly we are seeing this with the Federal Reserve’s battle to bring down inflation. Despite multiple rate hikes, the overall trajectory of interest rates in the US has been downward since last November.

Treasury yields in particular peaked in November and have been drifting lower ever since.

Aside from a brief surge in the 1-Year and 2-Year yields in February and March, Treasury yields all along the yield curve have ignored the Federal Reserve’s increases to the federal funds rate and moved steadily lower.

Nor is it just Treasury yields. Corporate debt yields generally run higher than Treasury yields, but they, too, have been trending down since November.

Junk debt yields run higher still, but are still moving lower, albeit much more incrementally than investment grade corporate debt.

Even residential mortgage rates peaked late last fall and have drifted down ever since.

These rates have all moved down despite multiple Federal Reserve rate hikes to the federal funds rate. In theory, raising the federal funds rate has a knock-on effect that pushes other interest rates up as well.

In reality, those other interest rates behave however they will, irrespective of what happens with the federal funds rate.

As these broad debt yield metrics move, so too do individual interest rates, such as the rates typically charged for personal loans, which have also fallen recently for the three-year loan term.

For borrowers with credit scores of 720 or higher who used the Credible marketplace to select a lender between April 3 and April 9:

Rates on 3-year fixed-rate loans averaged 14.48%, down from 14.71% the previous seven days and up from 10.54% a year ago.

Rates on 5-year fixed-rate loans averaged 17.96%, up from 17.42% over the previous seven days and up from 13.95% a year ago.

As I mentioned in yesterday’s article, the Federal Reserve is doing many things, but raising interest rates is not one of them.

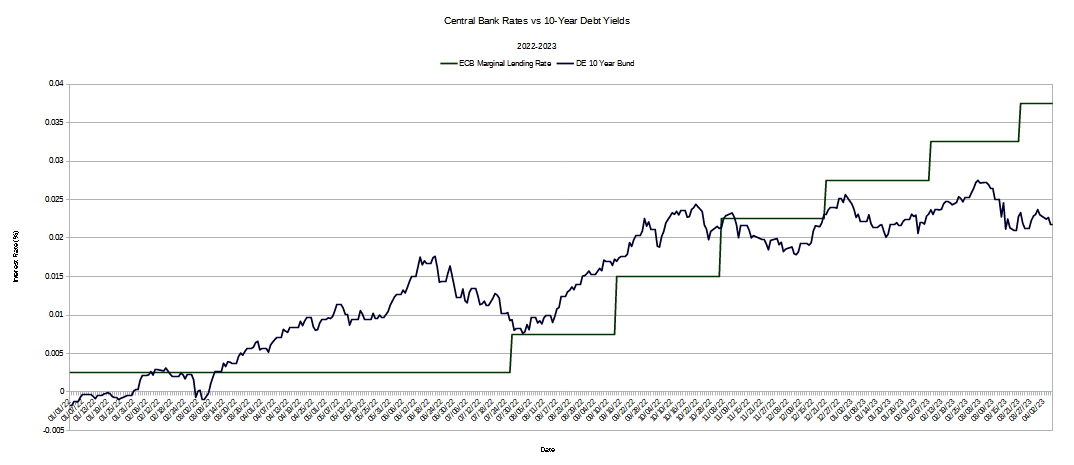

We must be mindful as well that the Federal Reserve is not the only central bank that has been pushing interest rates higher. The European Central Bank has enacted six interest rate rises within their key interest rates since last summer. However, the 10-Year German Bund yields have demonstrably not kept pace.

This has been true even though European interbank interest rates—or “Euribor” rates—have been on a steady upward trajectory since before the ECB began raising interest rates.

In Europe just as in the United States, the broad spectrum of interest rates have not been rising in recent months, even though the ECB has been pushing their key interest rates higher.

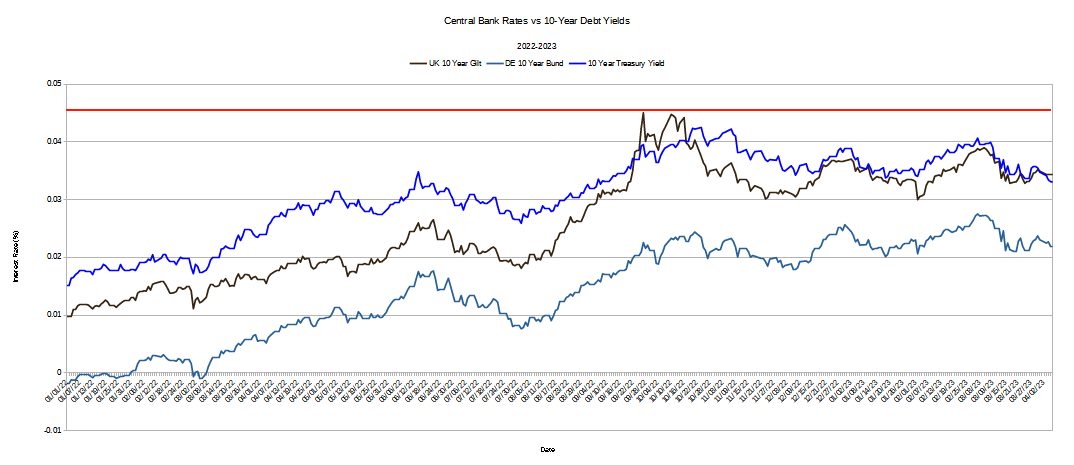

In Great Britain, the same phenomenon has been playing out. The Bank of England has raised its official bank rate multiple times over the past year, but the most recent raises have been largely ineffective at pushing broader interest rates higher. The yields on 10-Year gilts have been largely impervious to the most recent bank rate increases by the BoE.

As with the European Central Bank and the Federal Reserve, the most recent rate hikes by the Bank of England have failed to move debt yields higher—despite that being an explicit intention behind the rate hikes.

This is a problem for the central banks, because interest rate increases are their preferred means of addressing rampant consumer price inflation, which has been rising steadily in the US as well as the UK and Europe.

It is considered “settled science” among the world’s economists that hiking interest rates are how consumer price inflation is brought under control. If a central bank is going to contain consumer price inflation for any nation or group of nations, it must be able to push interest rates higher if this strategy is to be utilized whenever inflation becomes a problem—and inflation is indisputably a problem worldwide.

Not only is consumer price inflation a global problem, raising interest rates is by far the “global” solution—at least, it is the solution central banks are using. Almost all of the world’s central banks have raised their particular key interest rates this year.

In every instance, the goal is to move interest rates higher.

If central banks cannot effectively move interest rates higher as needed, their “go to” tool for controlling and reducing consumer price inflation loses much of its efficacy.

Why are central banks unable to push interest rates higher, as they (and most) would expect?

One possible explanation for this is that the “natural”, or neutral, rate of interest developing economies and their central banks especially should utilize is fairly low—perhaps as low as the IMF has recently projected.

In its latest World Economic Report, the IMF argued that rates in the US and other industrial countries will revert toward the ultra-low levels that prevailed prior to the pandemic, driven by aging populations and sluggish productivity growth. It sees the so-called natural or neutral rate – the inflation-adjusted short-term rate that neither pushes the economy ahead nor pulls it back – comfortably below 1% in the US in the coming decades.

That contrasts with the stance taken by Summers, who suggested last month that the real neutral interest rate — or R* in economists’ parlance — might be in a range of 1.5% to 2% going forward, in part because of stepped-up government borrowing to finance increased military outlays and the transition to a greener economy.

If the neutral rate of interest is lower than otherwise thought, then it could be that, as central banks attempt to push interest rates ever higher, countervailing pressures build in financial markets. Accordingly, beyond a certain point those same market forces overwhelm the central banks’ rate-hiking efforts, keeping interest rates from rising, and eventually forcing them back down again.

No matter what the actual neutral rate of interest is, or what its influence on financial markets might be, the market reality that, at present, global financial markets are not allowing sovereign debt yields much above ~4.5-5% for a 10-year maturity. In effect, the markets are “capping” sovereign debt.

As we can see with US debt yields, sovereign debt is the bellwether by which private debt yields are driven.

Moreover, for a considerable portion of recent history, Treasury yields have been well above 5%, even outside of Volcker’s interest rate shock therapy experiment of the early 1980s.

The markets are, in effect, taking higher debt yields off the table. Higher interest rates are increasingly presenting as something beyond what is possible. Higher interest rates are certainly presenting as something Wall Street finds not at all desirable.

When we look at all the data, we quickly learn that we should not be surprised that markets are responding in this way. What has never been acknowledged by the Fed or any central bank economist anywhere is the degree to which major interest rate increases are a complete change in the markets’ financial plumbing world wide.

As I have discussed before, because rates have risen, bank asset valuations have declined, and not by a small amount.

The loss of value has been calculated to be as much as $2 Trillion, and possibly more.

The fragility is disturbingly quantified by economist Erica Jiang’s recent research into bank assets which found the market value of bank assets is underwater to the tune of $2 Trillion

We analyze U.S. banks’ asset exposure to a recent rise in the interest rates with implications for financial stability. The U.S. banking system’s market value of assets is $2 trillion lower than suggested by their book value of assets accounting for loan portfolios held to maturity. Marked-to-market bank assets have declined by an average of 10% across all the banks, with the bottom 5th percentile experiencing a decline of 20%. We illustrate that uninsured leverage (i.e., Uninsured Debt/Assets) is the key to understanding whether these losses would lead to some banks in the U.S. becoming insolvent-- unlike insured depositors, uninsured depositors stand to lose a part of their deposits if the bank fails, potentially giving them incentives to run. A case study of the recently failed Silicon Valley Bank (SVB) is illustrative. 10 percent of banks have larger unrecognized losses than those at SVB. Nor was SVB the worst capitalized bank, with 10 percent of banks having lower capitalization than SVB. On the other hand, SVB had a disproportional share of uninsured funding: only 1 percent of banks had higher uninsured leverage. Combined, losses and uninsured leverage provide incentives for an SVB uninsured depositor run. We compute similar incentives for the sample of all U.S. banks. Even if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to insured depositors, with potentially $300 billion of insured deposits at risk. If uninsured deposit withdrawals cause even small fire sales, substantially more banks are at risk. Overall, these calculations suggest that recent declines in bank asset values very significantly increased the fragility of the US banking system to uninsured depositor runs.

This, in sum, is the minefield Jerome Powell and the FOMC have to navigate to reach a decision on interest rates.

Such valuation decline was inevitable once interest rates started to rise. Such valuation decline is inevitable everywhere interest rates started to rise. Such valuation decline is of such magnitude that it amounts to a structural change to banking itself; the types of assets banks can plausibly hold and not go bankrupt is dramatically changed in a high interest rate environment.

Part of the Fed’s failure, part of the ECB’s failure, and the Bank of England’s failure, has been to acknowledge the dramatic restructuring of bank balance sheets higher interest rates demand. It requires no great leap of imagination to perceive Wall Street pushing back on the an implicit central bank demand for permanent structural changes within bank balance sheets and thus within banks themselves.

Arguably, Wall Street’s rejection of higher interest rates is as much a matter of financial self-defense as it is anything else. Similarly, the IMF’s embrace of lower interest rates is a reflection of how fundamental a change to the financial status quo higher interest rates ultimately are.

Ultimately, before central banks can continue to push interest rates and debt yields up, they must confront the destruction of value among existing lower-yielding bank assets such policies require. This they have not done.

If central banks do not acknowledge the destruction of value among existing bank assets their rate-hike policies demand, banks’ own instincts for self-preservation will work to prevent any further increase in market-driven interest rates. As we are already seeing, central banks ultimately are impotent against the concentrated force of financial markets.

As usual, your analysis makes more sense than anything else I’ve read. Two trillion dollar loss of value - there is no way that any of the financial powers can ‘whitewash’ that away - what were they thinking?

I don’t know the ‘natural’ value of anything financial anymore. Take stocks, for example. When they started the quantitative easing in 2009, certain assets such as stocks became overvalued, as in a bubble. So, all these years later, are they still overvalued, or have they somehow come to a ‘natural’ level? If they’re still a bubble, shouldn’t there be more concern by financial professionals that the bubble will pop? Have the financial powers and government so messed up normal market forces that traditional metrics like P/E ratios don’t even matter any more in stock valuation? And how do all these zillions of dollars in derivatives fit into the picture - does *anyone* really understand it? It’s the fact that so few people seem to be able to comprehend the big financial picture that worries me...

"central banks ultimately are impotent against the concentrated force of financial markets"

They are impotent against spending money you don't have, especially when it is on a worthless plan such as climate change, or "gore bull warming" as I call it.

Despite all the forecasts, it is going to be getting colder, than it already is, and there isn't a thing that we can do about it, even the idea of a nuclear exercise, multiple explosions (400!) on the Great Plains, will do nothing to make it worse or better.