Can Germany Re-Industrialize?

Friederich Merz Is Staking The Future Of His Coalition On The Answer

One way or another, Germany is on the cusp of a fairly substantial transformation.

Not only is incoming Chancellor Friederich Merz advocating a substantial defense buildup and re-armament program, he wants to rewrite Germany’s constitution to do it.

Germany is in for a massive ramp-up in spending under an agreement, opens new tab by the parties hoping to form its next government, with a 500 billion euro special fund sought for infrastructure and plans to unshackle defence investment from its debt rules.

With spending programs and constitutional amendments in hand, Merz hopes to begin his Chancellorship with a fairly rapid re-industrialization of Europe’s declining industrial superpower.

At the levels of spending being contemplated, Germany’s pivot on spending promises to have significant ramifications not just for the German but also for the European economy. Very likely Merz is also betting the future of his coalition government in Germany’s Bundestag.

Decline Of German Industry

To appreciate the significance of what Merz is proposing, in conjunction with his presumptive coalition partners, one has to appreciate just how poorly German industry has fared in recent years.

In January, German industrial production shrank 1.6% More importantly, however, is that January was the 20th consecutive month that Germany’s industrial output declined.

German industry took it on the chin during the 2020 COVID Pandemic Panic, but a moderate recovery in 2021 has gone exactly nowhere in the three years since the start of the Ukraine War in 2022.

We should take care to note that Germany’s industrial woes did not start with Ukraine, although that war certainly has not helped any.

A related metric to industrial production—Manufacturing Production—decreased 4% in December of last year.

Industrial production covers all of German industry, while manufacturing production focuses on specific goods such as cars, computers, and various types of electrical equipment. Regardless of the item, however, Germany has been making steadily less of it for nearly the past two years.

Unsurprisingly, the output decline in German industry has impacted the overall economy, with most every other quarter since the start of the Ukraine war posting a decrease in GDP.

Equally disconcerting for German industrial output is that the value of that output has decreased every quarter since the first quarter of 2023.

This was insult added to injury for the German economy, as German construction was already contributing a declining amount to GDP.

By way of comparison, Germany’s GDP from Agriculture has done much better.

In what can only be described as a bureaucrat’s dream come true, Germany’s governmental bureaucracy—Public Administration—has also been a fairly reliable contributor of GDP.

This is what de-industrialization looks like. Not only is German industrial output shrinking, but it is shrinking relative to GDP. Germany’s industrial decline also means it is become less and less industrial.

For a country that has long been Europe’s industrial powerhouse, this is not a good thing.

Whatever It Takes?

These are the metrics that Friederich Merz has pledged to reverse, and to do “whatever it takes” to fulfill that pledge.

While details still need to be fleshed out, the historic deal between the chancellor-in-waiting and his likely coalition partners, the centre-left Social Democrats, allows for potentially unlimited borrowing for defence spending and creates a €500bn ten-year fund to drive infrastructure investments.

Economists expect the plan, which must still be approved by a two-thirds supermajority in parliament, can provide up to €1tn of additional borrowing over the next decade — a sum that represents more than a fifth of Germany’s entire economic output — and resurrect Europe’s largest economy after years of stagnation.

€1Trillion of new borrowing over ten years is a tremendous amount of debt, but in and of itself it is a fairly unremarkable and doctrinaire Keynesian approach to economic stimulus.

However, two aspects of Germany’s proposed spending are remarkable.

First, there is a heavy component of defense spending, to which Merz is also applying the “whatever it takes” mantra.

“In view of the threats to our freedom and peace on our continent, whatever it takes must now also apply to our defense,” Merz, leader of the CDU/CSU conservatives, said Tuesday.

Not coincidentally German defense industry companies have seen their stock valuations rise as Merz has ratched up the defense rhetoric.

The other noteworthy aspect of this proposed spending initiative is that Germany has to amend its Constitution to institute it.

Article 115 of Germany’s “Basic Law” (Constitution) limits how much borrowing can be done in any given year. Annual borrowing cannot currently exceed 0.35% of nominal GDP.

Thus, in order to enact this spending program, Merz needs to amend Germany’s Basic Law. Compared to what is required to amend the United States Constitution, however, the process is relatively straightforward. Merz requires only a two-thirds supermajority in both the Bundestag and the upper chamber, knowns as the Bundesrat, per article 79.

This is where the process gets tricky. Merz’ CDU party and his coalition partners the Social Democrats can get the requisite two-thirds vote if they can secure the support of the Greens (who support amending the so-called “debt brake” provision of the Constitution as a matter of policy), and if they can get the votes done before the new Bundestag is seated on March 25th.

In other words, the parties whom the voters largely rejected at the polls last month are about to rewrite Germany’s spending constraints and Constitution to their liking, after losing the election.

Already the far-left Die Linke party has promised a legal challenge should the amending legislation be passed prior to the new Bundestag being seated.

As of this writing, it is still uncertain if the Greens will back the amendment. If they do not, the amendment likely will not reach the two/thirds vote threshold, which would imperil the entire spending proposal.

With Spending Will Come Inflation

One aspect of Merz’ proposals that has not been explored by the corporate media is the impact a surge of government spending will have on inflation in Germany.

Amazingly, the assessment of corporate media is that Germany’s spending plan “might” have knock-on effects for the European Central Bank.

"The ECB will have to take into account that inflationary pressure will rise again as a result of the planned expansionary fiscal policy in Germany," said Cyrus de la Rubia, chief economist at Hamburg Commercial Bank.

Let us be clear: the German government spending up to a trillion euros over the next decade, particularly to the degree it is spent on defense procurement, is going to push up inflation at least in Germany.

Inflation is what will be rising, not “inflationary pressure.”

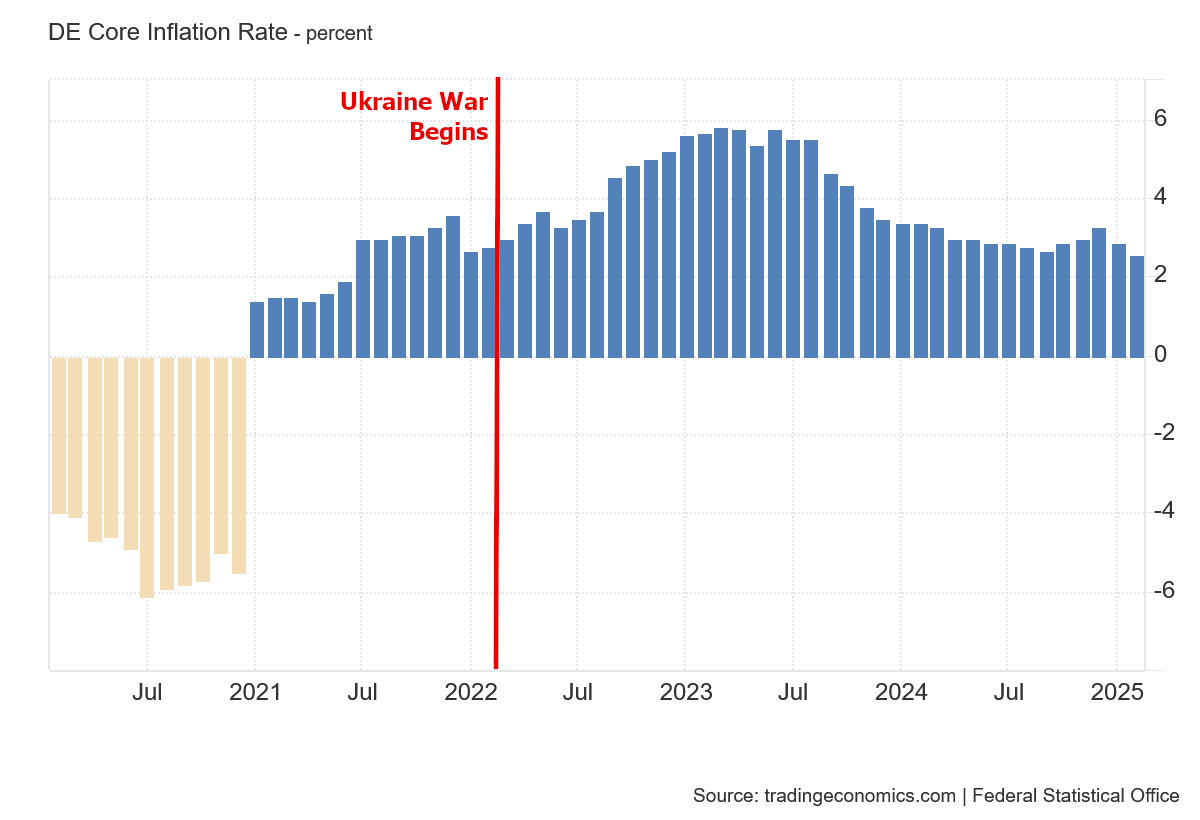

That would be a significant consequence of the proposed spending, in large part because Germany even after the start of the war in Ukraine has managed to retain one of the lower inflation rates in Europe.

Despite the dislocations from sanctions, Germany’s inflation now is lower than it was at the start of the war in Ukraine.

Even month on month inflation has been lower after the war than before.

Even core inflation stabilized around the same level it had been at before the war broke out.

Despite losing access to cheap Russian energy exports as a result of sanctions, Germany has actually been experiencing energy price deflation recently.

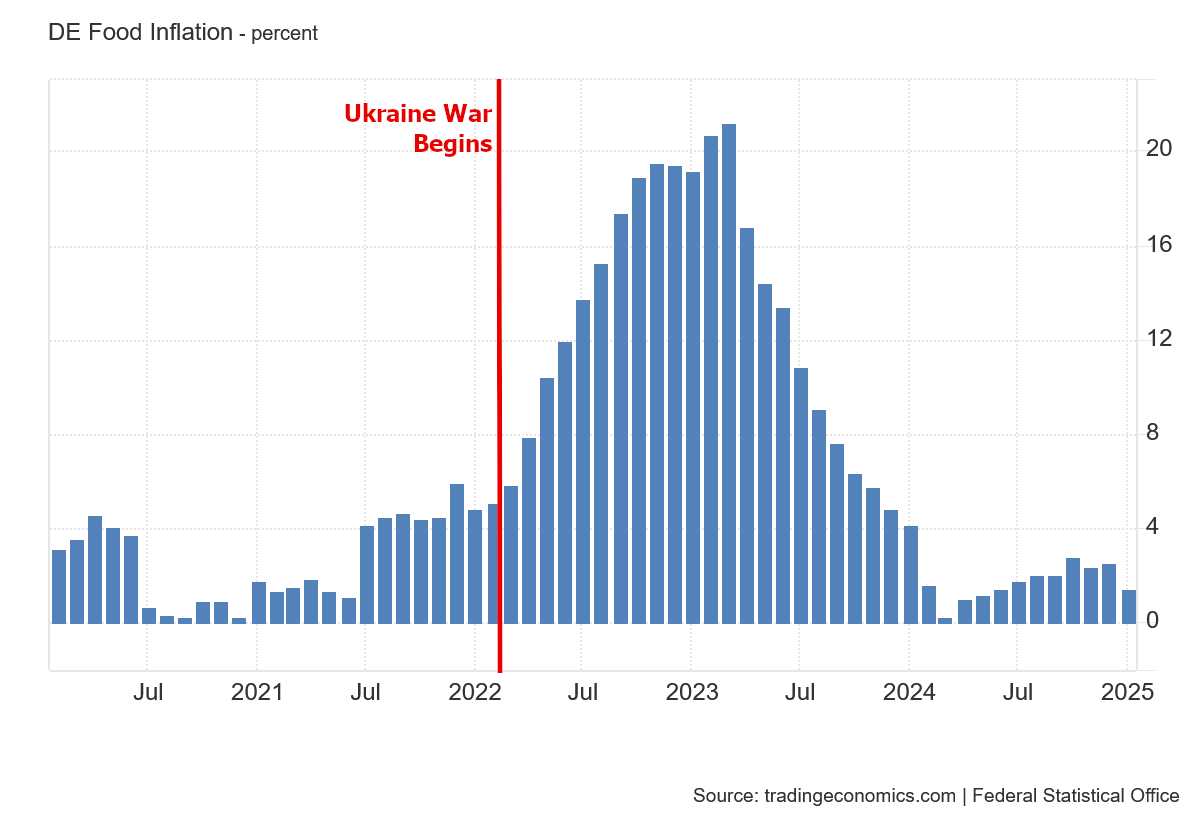

Food price inflation has also been lower recently than right before the war broke out.

A surge of government spending, particularly on manufactured and industrial items, is going to roil consumer prices to a significant degree. At the levels of spending being contemplated, there is almost no way for the spending not to have at least some inflationary impact.

With established inflation levels being fairly low, even a moderate increase in consumer price inflation could have dramatic perceived impacts on consumer prices. Inflation at 2.3% makes a rise to 4% inflation appear much more impactful than a rise to 6% inflation from 4%.

That Germany does not control its own money supply—that being handled by the ECB—makes contending with the inflationary impacts of a surge in spending structurally more challenging for Germany. The Bundesbank cannot simply soak up any excess liquidity.

Thus the question will need to be asked how will Merz temper the spending to mitigate or eliminate its inflationary impacts. That will not have a straightforward answer, because, in a manner of thinking reminiscent of Abenomics in Japan a decade ago, a primary selling point of the new spending initiative is that it is large. There will be a lot of spending, and it will be used to buy a lot of tanks, a lot of weapons, and a lot of bullets. It will inject money into the economy even as it takes resources out, and thus will create an upward pressure on prices.

Mark my words, if this spending program gets through the Bundestag, there will be inflation. The only operative question is going to be “how much?”

Debt Bazooka

Abenomics is an imperfect analogy, as Germany’s use of the euro currency takes monetary stimulus off the table. The monetary aspects of the stimulus package are by default off-loaded to the ECB and will thus reverbate across the continent.

However, there is no denying that the spending package itself is intended to be large and impactful.

“A really big bazooka,” wrote Berenberg economist Holger Schmieding, commenting on the German measures. “These proposals for an immediate loosening of Germany’s fiscal rules will likely be enacted. They are a fiscal sea change for Germany.”

Merz said the CDU/CSU and SPD would submit a motion to the Bundestag lower house of parliament next week to amend the constitution so defense expenditure above 1% of economic output is exempt from the debt brake.

According to German polling firm INSA, just under half of all Germans support the idea of revising the “debt brake” to allow for greater government spending, and greater debt levels to sustain the greater government spending.

Constitutional issues aside, however, one of the many unanswered questions swirling around the spending proposals is how strong is the market for additional German debt?

What rate of interest will be needed to ensure a ready market for the new debt issuances?

That answer, of course, is unknowable, but the basic prognosis is that interest rates would have to rise.

Given that Germany has historically had one of Europe’s lower interest rates, and thus the debt service cost on German bunds is systemically lower than for the sovereign debt of other leading countries in Europe, even a seemingly small rise in interest rates is going to have a larger impact on debt service costs.

With Debt Will Come Interest Rate Hikes

Part of the challenge surrounding the inevitability of interest rates rising as a consequence of the spending program is that interest rates have already been rising recently.

Since the start of the war in Ukraine, interest rates in Germany have moved out of negative territory and climbed very nearly to 3% in the fall of 2023. Recent speculation over the proposed debt-and-spending package being championed by Merz is pushing bund yields close to that level yet again.

As we saw in the fall of 2022, when the Bank of England had to intervene to stop yields on British gilts from rising too high too fast, rising interest rates can precipitate a liquidity crisis

Rising interest rates were the catalyst which roiled a number of US banking concerns in the spring of 2023.

If interest rates rise too far and too fast, Germany’s banks could end up in rough waters.

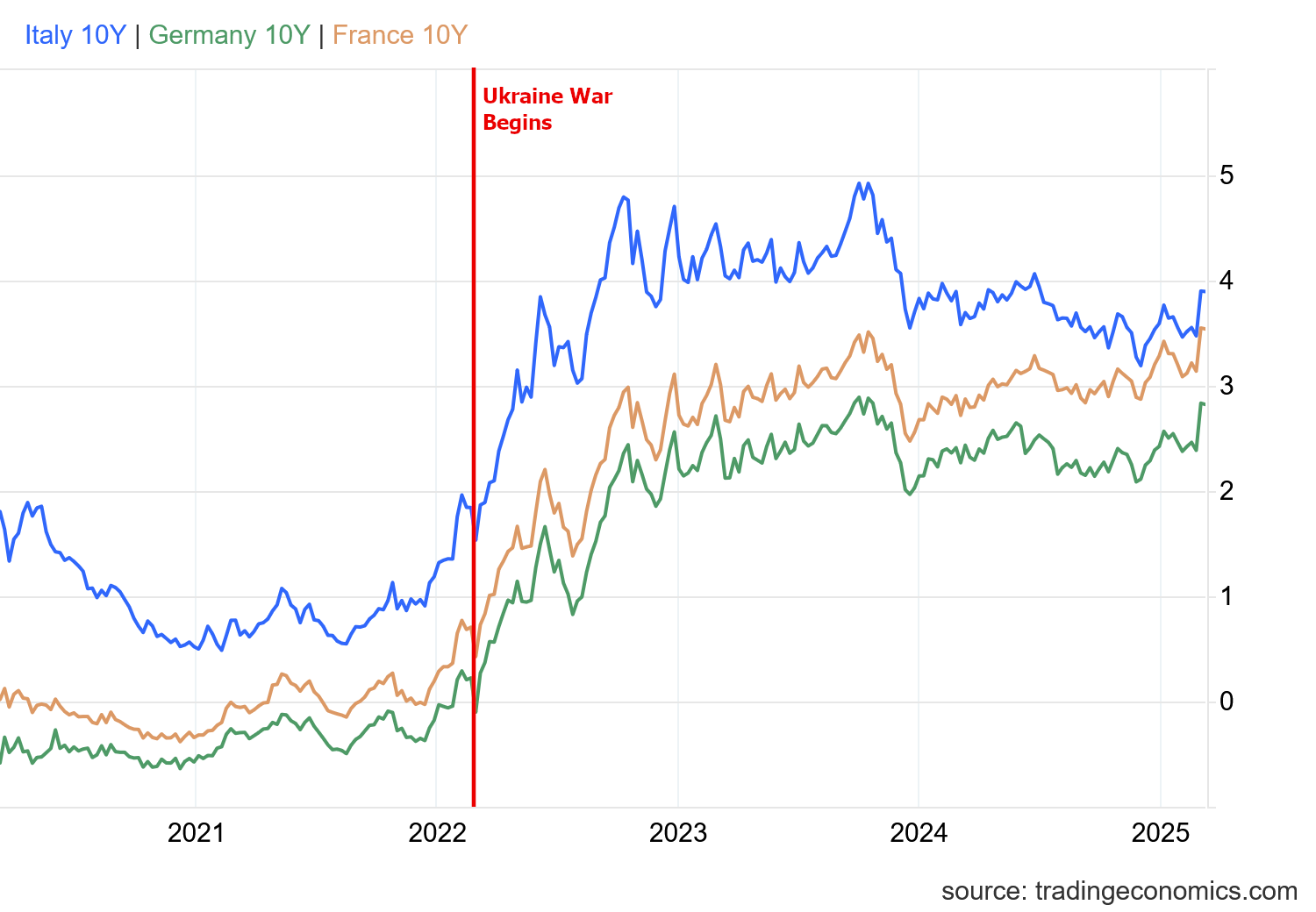

Nor will the interest rate question be limited to Germany. Because Germany has one of the lowest interest rates within the Eurozone, other countries’ sovereign debt is often more attractive, because it offers greater yield.

Italy and France, for example, offer a full percentage point worth of interest premium above Germany in order to compete with German bunds. As the chart shows, there is a strong correlation among European interest rates. If Germany’s “debt bazooka” acts as it almost certainly will, pushing up German interest rates, then yields on French and Italian debt will also rise, and indeed yields on European indebtedness as a whole will rise.

Can Europe withstand an increase in the market interest rates of a percentage point or more? More precisesly, can European banks and investment funds avoid a liquidity crisis from a rapid rise in debt yields?

That seems unlikely. We have seen in Britain and here in the US the stress on the banking system that rapid interest rate hikes can have. It beggars belief to suppose that a surge in debt yields on the continent because of Germany’s new-found debt liberalism would not impose a similar stress on banks across Europe.

Will Merz Succeed?

The sixty-four thousand euro question in all of this, of course, is “will it work?”

Will Friederich Merz succeed in getting Germany’s Basic Law amended to allow for greater levels of debt spending particularly in areas of defense?

Will Germany be able to reinvigorate defense production, and be able to churn out more tanks, more artillery systems, more munitions of all kind, both for use within the German military and for sending to Ukraine in support of their war effort (assuming that the recent ceasefire proposal proffered by the United States to which Ukraine has agreed does not take hold or does not last)?

The first question is by far the most immediate and therefore the most relevant. In addition to the likely challenge to Merz constitutional amendment promised by Die Linke, the far-right (and rising Bundestag power broker) Alternative für Deutschland is also promising challenges to the constitutionality of Merz’ manipulation of the lame duck session of the Bundestag, as AfD spokesman Jan Wenzel Schmidt affirmed in an interview with the Asia Times.

Asia Times: So, the whole AfD parliamentary delegation will take legal action against this initiative?

Jan Wenzel Schmidt: Yes, we have already prepared a formal complaint for the Federal Constitutional Court.

If Merz is unable to get the debt brake amendment through the legislature during the lame duck session, it is unclear what will happen to either the amendment or the spending package in the new legislative session. What is certain in the new legislative session is that together Die Linke and AfD are large enough to block any constitutional amendment.

Even if Merz gets the debt brake amendment passed, and then the spending bill passed, it is by no means certain the spending will have the desired effects.

German industry has been in a tailspin for at least the past three years, and Germany’s cutting themselves off from Russian oil and Russian natural gas via sanctions on Russia has not been kind to a number of German firms. The question I posed in the fall of 2022—“will Europe deindustrialize?”—has largely been answered grimly “Yes”.

With this debt-and-spending proposal, Germany aims to reverse this decline. Certainly defense spending is one of the more reliable ways a government can stimulate the national economy, particularly in a country with a mature industrial sector such as Germany.

However, the challenges to German industry are not alleviated merely by the commitments of more spending by the government. The loss of Russian energy sources has been a burden for German industry, and as a consequence many German firms have relocated their factories and production lines out of Germany, and even out of Europe. Plants which were shuttered more than two years ago are not going to be easily re-opened, and building new production capacity will take time.

Thus far corporate media has been quite receptive to Germany’s proposed “debt bazooka”, as has the German public. It is not hard to understand why—the economic data of the past few years makes plain that Germany needs to change its economic course and quickly.

However, there is no getting around the reality that Germany may not get to fire that bazooka, and even if it does, no guarantee that it will be able to hit the target.

What happens to Merz’ government in that worst-case scenario is an unknown, of course, but it is difficult to fathom an outcome to that scenario where Merz and his coalition are around for very long if the “debt bazooka” does fail.

Thank you for another intelligent and comprehensive analysis, Peter. We are able to read through it and see how, in one way after another, Germany has painted itself into a corner.

For decades German politicians have indoctrinated their constituents that Green is good, industry is bad. Oil is bad, military is bad, capitalism is bad, investment is bad. Now these politicians have to suddenly reverse course and actually DO all of the things they have said are bad! How is that going to work out for them politically? Any member of the Green Party advocating for ramping up industrial production and favorable policies for the energy industry is going to be attacked as a traitor to Green philosophy!

I see long-term wins for AfD and similar reality-based political mindsets. Reality wins out, every time! It’s my birthday today, and this is like a present from the Universe: reality is winning, and the world is (painfully) righting itself.

I appreciate the analytical effort you went to in order to document your post, but the fundamental question is “can governments legislate economic prosperity?” The past years of German government has shown us that the answer is a redundant NO. Why would the new coalition be different, especially as you point out, even before taking power, they are supercharging the old coalition? I’m afraid all these billions will be wasted, only to profit yet another grift. Let’s talk again in 4 or 5 years.