For the love of money is a root of all kinds of evil: which some reaching after have been led astray from the faith, and have pierced themselves through with many sorrows. — 1 Timothy 6:10

There is a certain irony in a Substack which purports to focus on facts, data, and evidence starting with a bit of Scripture. However, it is an irony with a purpose, which I hope to make clear.

Even without the ongoing bloodbath in the US banking sector, money has been very much in the news of late.

We are told that Central Bank Digital Currencies (CBDCs) are sure to be a major issue in next year’s Presidential election contest.

“Expect this CBDC issue to become a presidential campaign talking point,” said Ron Hammond, director of government relations at Blockchain Association. “Perfect intersection of fear of government, China and finance collapse with the bank crisis.”

There is no shortage of commentators tut-tutting over the US dollar’s “inevitable” decline as global financial hegemon—with “de-dollarization” the latest talking point fad.

The unintended consequence of the US’ decision to weaponise the dollar and use it as part of the extreme sanctions regime on Russia has been to shock the world’s central banker community and undermine confidence in the dollar as the default foreign exchange currency of trade and reserves.

The result has been to give impetus to the long-mooted desire to break the dollar’s monetary hegemony, so that there is for the first time some real political will behind making the change.

More than a few readers of this Substack have voiced concerns that the current economic turmoil will lead to the imposition of a dystopian, Orwellian, CBDC here in the US.

And that will lead to "digital money" in which we all will bank with GOOGLE or some similar on-line entity which will be controlled ultimately by China. At least the little "people."

Money, it seems, is a news focus of the moment. As Pandemic Panic was the narrative of 2020 and 2021, money is at the core of the narratives being advanced for 2023. CBDCs in particular are very much on people’s minds, both by people who would encourage and advocate for them and by those who reject and condemn them.

Thus the “love of money” becomes a useful framing even for a fact-based and data-driven view of that narrative. The Biblical precaution against the “love of money” actually sets up many of the reasons not only for why monetary artifices such as CBDCs are not succeeding where they are being tried, but also for why it is not possible for them to succeed.

One point I do need to make clear: it is my thought that, even if the Federal Reserve should impose a CBDC on the US, it will fail as a currency replacement for the non-digital dollar. This does not mean that I believe the Federal Reserve will choose against implementing a CBDC, merely that I do not believe Federal Reserve has even a snowball’s chance in Hell of making it work.

To understand why this is, we must begin with fundamental definitions. Most importantly, we must be clear on what money—as well as currency—is, and it is not.

Money, simply put, is anything people use to pay for goods and services1.

Money is anything that serves as a medium of exchange. A medium of exchange is anything that is widely accepted as a means of payment. In Romania under Communist Party rule in the 1980s, for example, Kent cigarettes served as a medium of exchange; the fact that they could be exchanged for other goods and services made them money.

There is nothing about money which requires or even recommends it be based on or in computer technology of any kind.

“Currency” is generally apprehended to be the paper money and metallic coins we traditionally associate with “money”.2

But something need not have intrinsic value to serve as money. Fiat money is money that some authority, generally a government, has ordered to be accepted as a medium of exchange. The currency—paper money and coins—used in the United States today is fiat money; it has no value other than its use as money. You will notice that statement printed on each bill: “This note is legal tender for all debts, public and private.”

However, we should note that with the advent of crypto currencies and their central banking cousins, CBDCs, “currency” is morphing into a concept that embraces electronic/digital forms as well. Still, even digital currencies, crypto or otherwise, work as currencies because people are willing to accept them as currencies. If a proposed form of currency is rejected as “unacceptable” by the greater mass of people, it will fail as a currency, no matter how coercive or repressive the regime which attempts to implement it3.

What makes something money is really found in its acceptability, not in whether or not it has intrinsic value or whether or not a government has declared it as such. For example, fiat money tends to be accepted so long as too much of it is not printed too quickly. When that happens, as it did in Russia in the 1990s, people tend to look for other items to serve as money. In the case of Russia, the U.S. dollar became a popular form of money, even though the Russian government still declared the ruble to be its fiat money.

The first hurdle that CBDCs need to overcome—and which they are failing to overcome, is that of acceptability.

The most glaring example of this has been China’s CBDC experiment, the digital yuan. Even after two years of adoption efforts by Beijing—perhaps the most totalitarian regime on the planet—the digital yuan has gained little traction.

Xie Ping, a former PBOC research director and current finance professor at Tsinghua University, made critical public comments about China’s central bank digital currency (CBDC) at a recent university conference, according to a Dec. 28 Caixin report.

Xie noted that cumulative digital yuan transactions had only crossed $14 billion (100 billion yuan) in October, two years after launch. “The results are not ideal,” he said, adding that “usage has been low, highly inactive.”

To make the situation even worse for the digital yuan, transaction volume at the end of 2021 was reported at $13 billion—meaning for all of 2022 there were merely $1 billion worth of digital yuan transactions in the world’s second largest economy.

Yet China’s experience is not at all unique. Nigeria was the first African nation to implement a CBDC in 2021, yet fewer than 1% of Nigerians have used it—even though more than 50% of Nigerians use or hold cryptocurrencies.

Not that Nigeria’s central bank has not tried to incent people to use the digital currency, also known as the eNaira.

A year after launching Africa’s first digital currency, Nigeria’s central bank is turning to the nation’s three-wheeler taxi operators to speed the adoption of the eNaira, as regulators across the world scrutinize its every move.

It’s offering a 5% discount to drivers and passengers of the motorized rickshaws -- known locally as Keke Napep -- who use the eNaira. It’s the latest attempt to kickstart the digital currency, which has so far attracted just one in 200 people in the continent’s most populous country.

The most fundamental weakness of the eNaira is this lack of acceptability—many Nigerian merchants apparently do not take the digital currency in payment.

There may be a dearth of merchants willing to accept the eNaira, according to London-based Varun Paul, CBDC and market infrastructure director at institutional crypto custody platform Fireblocks. Paul, who previously worked at the Bank of England as an economist and head of its fintech hub, is now leading Fireblocks’ efforts to build out infrastructure for CBDC integration.

Concerns over acceptability appear to be one reason India is proceeding very tentatively on its CBDC project. Although the project has gathered some 50,000 users and roughly 5,000 merchants, the most populous country in the world apparently is not opening the implementation project up to new users at this time.

Announcing the first public milestones of India’s digital currency at a policy press conference, RBI deputy governor Rabi Sankar stressed that the government plans to proceed with CBDC testing in the smoothest way possible.

“We have our targets in terms of users, in terms of merchants. We will go slowly,” Sankar stated, noting that the RBI doesn’t want to push CBDC developments without having full awareness of its potential impact.

The latest announcement adds up to data from an official digital rupee application, which suggests that the pilot is taking no more users. According to data from the digital rupee app by the ICICI Bank, India’s CBDC program is full at the time of writing, suggesting that more users would be able to join the trial at a later date.

At a minimum, India’s hesitancy regarding its digital rupee suggests users and merchants alike are somewhat skeptical of the CBDC, and are not really prepared to accept it as money.

Even in countries without actual CBDCs, there are strong movements against accepting them as money. In Switzerland, a petition drive by the Free Switzerland Movement claims it has amassed sufficient signatures for a popular vote on its proposal to amend the country’s currency laws to guarantee physical currency will always be available.

Swiss citizens will get the chance to try to ensure their economy never becomes cashless, a pressure group said, after collecting enough signatures on Monday to trigger a popular vote on the issue.

The Free Switzerland Movement (FBS) says cash is playing a shrinking role in many economies, as electronic payments become the default for transactions in increasingly digitised societies, making it easier for the state to monitor its citizens' actions.

It wants a clause added to Switzerland's currency law, which governs how the central bank and government manage the money supply, stipulating that a "sufficient quantity" of banknotes or coins must always remain in circulation.

Clearly, the acceptability of CBDCs has a way to go!

Of course, the mere fact that CBDCs are not accepted as money today is not a bar to central banks proceeding with efforts to implement them tomorrow. Despite the lackluster results elsewhere, Russia is proceeding with its own digital ruble project.

The Bank of Russia is preparing to roll out the first consumer pilot for the nation’s central bank digital currency (CBDC) on April 1, 2023.

Russia’s central bank is set to soon debut the first real-world digital ruble transactions involving 13 local banks and several merchants, first deputy governor Olga Skorobogatova said.

While China’s digital yuan has been less than successful, its existence is prompting Japan to push the Bank of Japan to at least begin laying the conceptual groundwork for a digital yen.

While the political attention has yet to translate into any other direct investment, it is also likely to keep the Bank of Japan (BOJ) under pressure to shift away from its cautious, baby-step approach toward issuing a digital yen, analysts say.

"We must think about what could happen to Japan's national security if other countries move ahead on CBDC," said Takayuki Kobayashi, a minister overseeing economic security - a new role created under Prime Minister Fumio Kishida's administration.

"Japan must speed things up so it's ready to issue a digital yen any time," he said.

But this begs a question: is it really sound monetary policy for any central bank to pursue new forms of currency merely because “everyone else is doing it”? Does it really make sense that CBDCs are made rational and useful simply because they are the popular fad of the moment? Are CBDCs truly something to be desired (“loved”?) by central banks merely because they are popular with other central banks?

While popularity certainly serves to overcome the acceptability hurdle, Gresham’s Law4 cautions against mere acceptance as sufficient to gauge a currency’s worthiness.

Sir Thomas Gresham lived from 1519 to 1579 and wrote about the value and minting of coins while working as a financier and later founded the Royal Exchange of the City of London. When Henry VIII changed the composition of the English shilling, replacing a substantial portion of the silver with base metals, citizens separated the English shilling coins and hoarded the coins containing more silver which were worth more than their face value.

Both currency types were liquid and available simultaneously for use as acceptable forms of exchange. Gresham observed that bad money was driving out good money from circulation. Bad money is a currency with equal or less value than its face value. Good money has the potential for a greater value than its face value. People will choose to use bad money first and hold onto good money. The Scottish economist Henry Dunning Macleod attributed this law to Gresham in the 19th century.

When spending money, people will prefer to use their “bad” money first, in order to retain their “good” money. As a result, “bad” money—money which has been debased in value or has some other defect which impairs its utility—is more likely to be in wide circulation, as the “good” money is stored away. Popularity arguably suggests a currency qualifies as “bad” money if people choose to spend it rather than hold it.

Why would a CBDC be “bad” money?

Consider how a central bank would implement a digital currency, and in particular consider the characteristics the Federal Reserve ascribes to a conceptual CBDC in its 2022 paper5 on the subject.

As noted above, for the purposes of this discussion paper, CBDC is defined as a digital liability of the Federal Reserve that is widely available to the general public. Today, Federal Reserve notes (i.e., physical currency) are the only type of central bank money available to the general public. Like existing forms of commercial bank money and nonbank money, a CBDC would enable the general public to make digital payments. As a liability of the Federal Reserve, however, a CBDC would not require mechanisms like deposit insurance to maintain public confidence, nor would a CBDC depend on backing by an underlying asset pool to maintain its value. A CBDC would be the safest digital asset available to the general public, with no associated credit or liquidity risk.

Straight away, the Federal Reserve is differentiating a CBDC from the balance in a bank checking account or on a non-bank debit card. Money held in a bank checking account is “commercial bank money” in the argot of the Federal Reserve. Money on a non-bank debit card is “nonbank money”. Physical currency is, within the United States, the only form of “central bank money” in circulation.

The Federal Reserve’s thesis for a CBDC is that, as a direct liability of the Federal Reserve, a CBDC would not be at risk of a bank collapse such as the recent First Republic Bank failure. The Federal Reserve is, presumably, the “safest” bank in the US.

However, as the recent bank failures have demonstrated, credit risk and liquidity risk are not the only types of risk. There is also interest rate risk, and it is this type of risk which precipitated the downfall of Silicon Valley Bank, Signature Bank of New York, and First Republic Bank.

Interest rate risk6 arises in a financial environment characterized by rising interest rates.

Interest rate risk exists in an interest-bearing asset, such as a loan or a bond, due to the possibility of a change in the asset's value resulting from the variability of interest rates.

If a CBDC is allowed to earn interest while it is on deposit with the Federal Reserve, any time the Federal Reserve raises interest rates, the CBDC loses value in much the same way bank securities portfolios have lost value.

If a CBDC is not allowed to earn interest while it is on deposit with the Federal Reserve, the CBDCs value is intrinsically diminished relative to commercial bank money on deposit with a bank balance.

In both scenarios, however, the way the individual depositor can protect himself against interest rate risk is the same: spend the CBDC. This is no different than the way banks today would mitigate interest rate risk on their securities portfolios: they must sell the securities.

A currency which is better spent than held is the essence of “bad” money.

Would the Federal Reserve wish to allow CBDC deposits to earn interest? Potentially it might not have any choice. We only have to look at the crisis facing commercial banks today to see why.

Ever since the Federal Reserve began raising the federal funds rate, banks have been losing deposits, which have flowed to higher-yielding money market accounts and non-bank deposit accounts. One only needs to compare average interest rates between bank savings accounts and money market accounts to see why the flows have happened.

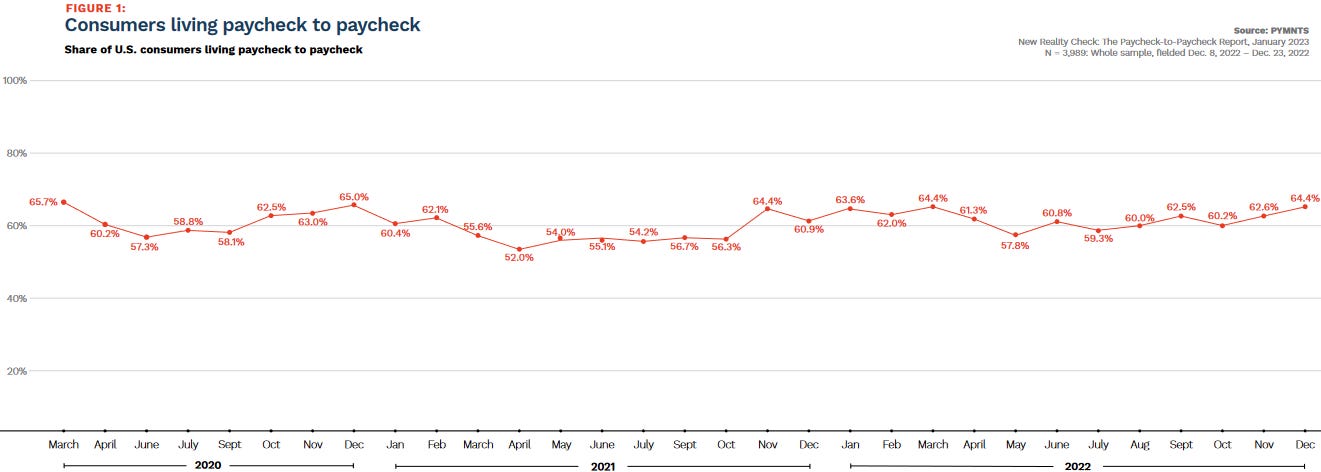

However, even without the interest rate imbalance, consumer price inflation pressures were resulting in an increasing number of consumers in this country living paycheck to paycheck.

The upward trend lines up reasonably well with the rise in inflation.

Without wandering into the weeds of why inflation is happening or why more consumers are living paycheck to paycheck, the key point for this discussion is that these consumers are spending their money rather than holding it.

Back in the 1960s, economist Milton Friedman identified this pattern of spending rather than holding as the fundamental economic behavior driving consumer price inflation7.

Given that people are so stubborn about the amount they hold in the form of money, let us suppose that, for whatever reasons, the amount of money in a community is higher than people want to hold at the level of prices then prevailing. It does not for our purposes matter why, whether because the Government has printed money to finance expenditures or because somebody has discovered a new gold mine, or because banks have discovered how to create deposits. For whatever reason, people find that although on the average they would like to hold, let us say, the 7 weeks’ income that they hold in India, they are actually holding, say, 8 weeks’ income. What will happen? Here again it is essential to distinguish between what happens to the individual and what happens to the community. Each individual separately thinks he can get rid of his money and he is right. He can go out and spend it and thereby reduce his cash balances. But for the community as a whole the belief that cash balances can be reduced is an optical illusion. The only reason I

can reduce my cash balances in nominal terms is because somebody else is willing to increase his. One man’s expenditures are another man’s receipts. People as a whole cannot spend more than they as a whole receive. In consequence, if everybody in the community tries to cut the nominal amount of his cash balances, they will on the average be frustrated. The amount of nominal balances is fixed by the nominal quantity of money in existence and no game of musical chairs can change it. But people can and will try to reduce their cash balances and the process of trying will have important effects. In the process of trying to spend more than they are receiving, people will bid up the prices of all sorts of goods and services. Nominal incomes will rise and real cash balances will indeed be reduced, even though nominal balances, the number of rupees, are not affected. The rise in prices and incomes will bring cash balances from 8 weeks’ income to 7 weeks’ income. People will succeed in achieving their objective, but by raising prices and incomes rather than by reducing nominal balances. In the process, prices will have risen by about an eighth. This in a nutshell and somewhat over-simplified is the process where by changes in the stock of money exert their influence on the price level. It is over-simplified because there is a tendency to over-shoot, followed by successive readjustments converging on the final position, but this complication does not affect the essence of the adjustment process.

Just as there is an incentive/pressure to spend money today (or at least the lack of an incentive to hold money), a similar pressure and incentive would exist for a CBDC.

Without the opportunity to earn interest, consumers deposits of CBDC would be subject to the same spending pressures—without interest to rationalize holding rather than spending—a CBDC will be inherently inflationary, for the same reasons spending is incentivized within the current state of the US financial system.

Additionally, the Federal Reserve has acknowledged the capacity of a CBDC to allow government micromanagement of personal savings and spending patterns8.

A non-interest-bearing CBDC, for example, would be less attractive as a substitute for commercial bank money. In addition, a central bank might limit the amount of CBDC an end user could hold.

The likelihood the Fed would be tempted to do just that would also drive spending rather than holding and saving. Again, the way an individual can mitigate the perceived negative impacts of a CBDC would be to spend it straight away—to treat the CBDC as “bad” money

Encouraging spending is the acme of inflationary monetary policy. Every time.

When one examines every one of the features (and presumed “benefits”) of CBDC acknowledged by the Fed, the potential for people to view such features negatively ultimately would encourage spending—to get rid of the unwanted currency—and thus would drive inflation.

The Federal Reserve admits that a CBDC by its very nature would accrete personal data about spending patterns, personal tastes and preferences, even movements. Anyone wishing to avoid being so catalogued would not want to hold CBDC in any account—and would therefore spend it as quickly as they could just to be rid of it.

The Federal Reserve admits that a CBDC would be designed to inhibit money laundering and similar financial crimes. The criminal element of society would definitely not want a CBDC just for this reason alone—and again would spend it just to be rid of it.

The Federal Reserve defines a CBDC as a liability of the Federal Reserve. A checking account is a liability of the bank holding the funds, and a debit card account is a liability of the nonbank entity providing the card. Any entity—bank, nonbank, fintech firm, et cetera—offering such services is thus sidelined by a CBDC, which the Federal Reserve also acknowledges9.

Banks currently rely (in large part) on deposits to fund their loans. A widely available CBDC would serve as a close—or, in the case of an interest-bearing CBDC, near-perfect—substitute for commercial bank money. This substitution effect could reduce the aggregate amount of deposits in the banking system, which could in turn increase bank funding expenses, and reduce credit availability or raise credit costs for households and businesses. Similarly, an interest-bearing CBDC could

result in a shift away from other low-risk assets, such as shares in money market mutual funds, Treasury bills, and other short-term instruments. A shift away from these other low-risk assets could reduce credit availability or raise credit costs for businesses and governments.

Holding deposits is the foundation of all banking services, whether performed by a bank, a money market fund, a fintech firm, or any other entity. As both an accounting and legal matter, it is not possible for any entity—including the Federal Reserve—to hold deposits if there is no liability attached.

Liability and obligation are the essence of all financial transactions. The liability of the bank to the depositor is what enables the bank to lend, while the liability of the borrower is what enables him to pay for a house, for goods, or for the materials with which to make goods. The liability of the buyer to the seller of anything is fully one half of every transaction.

Without liability, there can be no money. Without liability, finance stops. As much as the Federal Reserve offers anodyne words about “intermediation”, because a CBDC is the liability of the central bank and of no other bank, there is no financial role left for a bank to play. The Federal Reserve even acknowledges this in a back-handed manner10.

The Federal Reserve Act does not authorize direct Federal Reserve accounts for

individuals, and such accounts would represent a significant expansion of the Federal Reserve’s role in the financial system and the economy. Under an intermediated model, the private sector would offer accounts or digital wallets to facilitate the management of CBDC holdings and payments. Potential intermediaries could include commercial banks and regulated nonbank financial

service providers, and would operate in an open market for CBDC services. Although commercial banks and nonbanks would offer services to individuals to manage their CBDC holdings and payments, the CBDC itself would be a liability of the Federal Reserve. An intermediated model would facilitate the use of the private sector’s existing privacy and identity-management frameworks; leverage the private sector’s ability to innovate; and reduce the prospects for destabilizing disruptions to the well-functioning U.S. financial system.

This is actually a paradox. Remember, a deposit by definition is never the bank’s money—that is why it counts as a liability of the bank11.

A deposit is money held in a bank account or with another financial institution that requires a transfer from one party to another.

With federal reserve notes as well as commercial bank and nonbank money, deposits are fungible12 once deposited, which is to say one block of funds is indistinguishable from (and interchangeable with) another block of funds. By the Federal Reserve's own description of how CBDCs function, CDBC deposits could never be fungible—the accretion of personal data within the CBDC itself precludes this possibility at a structural level—and thus the capacity of banks to generate loans off CBDC deposits would be impaired if not eliminated.

Moreover, even in a CBDC regime, for a bank to make a loan, the liability has to go to the bank, not to the central bank. Thus, even if a CBDC merely stands in as an electronic variant of today’s paper federal reserve note (and therefore fungible), the bank loan is still not central bank money but commercial bank money—the very monetary phenomenon a CBDC is seeking to replace. Wherever a liability is created in finance, so, too, is money, by definition13.

Where does money come from? How is its quantity increased or decreased? The answer to these questions suggests that money has an almost magical quality: money is created by banks when they issue loans. In effect, money is created by the stroke of a pen or the click of a computer key.

The only way to avoid commercial bank money is to avoid commercial banks. If the Federal Reserve does not intend to eliminate commercial banking and thus nationalize the entire US banking sector, it cannot offer a non-fungible CBDC. Commercial banking or non-fungible CBDC are the choices—there is not a third.

Even with a non-fungible CBDC, however, people would still generate money by simply trading digital “wallets” holding the CBDC. Just as people already do with gift cards—prepaid debit cards holding a specified amount of money—a transferable digital wallet would start out as a service to be offered and quickly mutate into yet another (non-CBDC) form of money.

This paradox goes a long way towards explaining why people simply do not embrace CBDCs when they are offered—why they have been a failure in China and in Nigeria and elsewhere: Central bank digital currencies, despite all the glowing phrases used by the Federal Reserve, don’t actually solve any monetary problem people have. By their very nature, CBDCs create additional problems for people.

Because of this paradox, CBDCs can never be anything but “bad” money—which is to say they can never provide anything but monetary inflation as people rush to rid themselves of CBDC holdings by spending them (and refusing to accept them).

Which brings me back to the verse from 1 Timothy. The failures, the wasted efforts, the inflation, the monetary disruptions and dislocations that a CBDC would have to bring all arise from the error of a central bank in hyperfocusing on money itself.

Regardless of one’s ethical or spiritual framework, money is never the point of anything. As a medium of exchange, money is simply a means to an end. It can never be anything more than that.

The Federal Reserve’s own statement of its purpose and mission—its reason for being—concedes this fundamental point.

The Federal Reserve System is the central bank of the United States. It performs five general functions to promote the effective operation of the U.S. economy and, more generally, the public interest. The Federal Reserve

conducts the nation’s monetary policy to promote maximum employment, stable prices, and moderate long-term interest rates in the U.S. economy;

promotes the stability of the financial system and seeks to minimize and contain systemic risks through active monitoring and engagement in the U.S. and abroad;

promotes the safety and soundness of individual financial institutions and monitors their impact on the financial system as a whole;

fosters payment and settlement system safety and efficiency through services to the banking industry and the U.S. government that facilitate U.S.-dollar transactions and payments; and

promotes consumer protection and community development through consumer-focused supervision and examination, research and analysis of emerging consumer issues and trends, community economic development activities, and the administration of consumer laws and regulations.

Everything the Federal Reserve sets out to do is notionally about facilitating people pursuing something other than money. Even the much-flawed FedNow service about to be initiated is outwardly a facilitation of transactions, and the reasons for opposing it arise from the inevitable ramifications of having a central bank provide that particular mode of facilitation.

CBDCs depart from this basic structure of central banking. CBDCs are not a facilitation of transactions, but an intrusion into them—CBDCs make money an end rather than merely a means. Far from providing any sort of “frictionless” payments, CBDCs are a source of friction. Anything that creates problems in finance is a source of friction, and CBDCs are an endless source of problems for finance.

While it may seem counterintuitive to tell a bank, even a central bank, not to “love” money, the unavoidable truth is that if central banks focus not on the money but on the exchanges money facilitates, on actually making it easier for people to trade and transact business, that is where even a central bank would deliver a real benefit to people.

Even for a bank, money is merely the means. Even for a bank, money is never the end. Even for a central bank, these things are true. Because these things are true, anything that puts the focus on money is inevitably false. Because these things are true, CBDCs are inevitably a false promise for any central bank to make.

University Of Minnesota Libraries. “The Nature And Creation Of Money.” Principles Of Economics, University Of Minnesota, 2016.

Ibid.

Ibid.

The Investopedia Team. “Gresham’s Law: Definition, Effects, and Examples”, Investopedia. 8 Feb. 2023, https://www.investopedia.com/terms/g/greshams-law.asp.

Board of Governors of the Federal Reserve System. Money and Payments: The U.S. Dollar in the Age of Digital Transformation. 20 Jan. 2022, https://www.federalreserve.gov/publications/files/money-and-payments-20220120.pdf.

Norris, E. “Managing Interest Rate Risk”, Investopedia. 9 June 2022, https://www.investopedia.com/articles/optioninvestor/08/manage-interest-rate-risk.asp.

Friedman, M. “Inflation: Causes and Consequences. First Lecture.” Dollars and Deficits, Prentice Hall, 1968, pp. 21–46. Retrieved online from https://miltonfriedman.hoover.org/internal/media/dispatcher/271018/full

Board of Governors of the Federal Reserve System. Money and Payments: The U.S. Dollar in the Age of Digital Transformation. 20 Jan. 2022, https://www.federalreserve.gov/publications/files/money-and-payments-20220120.pdf.

Ibid.

Ibid.

Kagan, J. “What Is a Deposit? Definition, Meaning, Types, and Example”, Investopedia. 26 Jan. 2023, https://www.investopedia.com/terms/d/deposit.asp.

Kenton, W. “What Are Fungible Goods? Meaning, Examples, and How to Trade”, Investopedia. 18 Apr. 2022, https://www.investopedia.com/terms/f/fungibles.asp.

University Of Minnesota Libraries. “The Nature And Creation Of Money.” Principles Of Economics, University Of Minnesota, 2016.

I read the fear over CBDC controlling carbon footprint, wrong opinion = can't buy food, etc. However, Canada was able to freeze bank accounts, revoke licenses, etc. during the very peaceful trucker protests. Interesting times....

Thank you for the Scripture, it's in within a great context and I'm grateful for the reminder to be content:

1 Timothy 6:6-11

But godliness with contentment is great gain, for we brought nothing into the world, and we cannot take anything out of the world. But if we have food and clothing, with these we will be content. But those who desire to be rich fall into temptation, into a snare, into many senseless and harmful desires that plunge people into ruin and destruction. For the love of money is a root of all kinds of evils. It is through this craving that some have wandered away from the faith and pierced themselves with many pangs. But as for you, O man of God, flee these things. Pursue righteousness, godliness, faith, love, steadfastness, gentleness.

"Money, simply put, is anything people use to pay for goods and services."

There may have been times when money was only used for this purpose. But since the arrival of FIAT money, the rules of the game have changed. This is because FIAT-money actually comes into circulation when a central bank, which can issue (create) FIAT-money, then credits (promises) an amount of it against a promise of repayment and then, if necessary, hands it out. And this means that the debtor, who can dispose of this money for a limited period of time, has to start offering (produced) goods (or services) in order to acquire the money to repay the debt. This is what is happening on the markets for produced goods today, namely that the suppliers of these goods see them not as value but as a means of attracting FIAT money. After all, it is not a matter of course that produced goods are sold for an intrinsically worthless object.

And then the arbitrariness of money (...is anything...) is over, because sellers of goods do not want just anything, but exactly the money they need to pay off their debts. In addition, they have to pay the turnover tax due on a sale in a certain kind of money, so that the range of possibilities is very quickly limited to exactly the legal tender money. (By the way, "cigarette money" was not so much a medium of exchange as a standard of value for determining current prices in local currency in order to then pay with the mostly (hyper-)inflationary money. Cigarettes were rarely exchanged directly).

The concept of interpreting FIAT money as a means of covering debts for producers or sellers of goods also explains why it is completely unnecessary to give FIAT money an intrinsic value. On the contrary, this would even be detrimental if the price calculation for goods is also disturbed by an intrinsic value of the means of payment. From the point of view of the instrument for debt repayment, the "legal tender" formulation is in itself meaningless, because the entrepreneur's interest consists precisely in receiving this money for goods to avoid default and losing collateral (acceptability is automatically built into it). The "legal tender" rule has more of a historical significance when it came to replacing the metal currency and people did not want their claims to be paid in (for them) worthless paper money. A lot of help had to be given, but those days are long gone.

And the CBDC? They are just as much "book money" as the deposits at a commercial banks, namely option rights that give the holder the right to instruct (!) the payment service provider either to pay out money (withdrawal) or to bring about a debt relief success vis-à-vis a precisely designated person who has a claim. The only difference is that the rights vis-à-vis a central bank are not at risk of default - a not insignificant difference. At the end of the day, CBDCs are an alternative to the "book money" of banks but not to cash.

There exists currently no alternative to cash, when cash is defined as a medium for final payment without need for a payment service provider. CBDCs are not what is claimed they are, because they are debt relationships. And debt relationships are not means of payment, as we can clearly see from bank failures: there are too many debt relationships (deposits - a liability for the bank) awaiting to be settled (in central bank money), but means of payment (cash and reserves - an asset for the bank) are the element that is missing. The digital innovation that can actually replace cash has not yet been found.