Has The Banking Crisis Really Been Cancelled? Or Merely Postponed?

What Has Actually Changed Since SVB Imploded?

As March drew to a close, the prevailing wisdom (even on this Substack), was that a credit and banking crisis was looming straight ahead.

In what could be a replay of the 2007-2008 subprime mortgage crisis, commercial real estate debt could be facing a looming default risk as distressed CRE markets collide with 2023 interest rates.

As we move towards the end of April, however, a narrative is emerging in the corporate media that perhaps the crisis might be a bit slower in coming, or even avoided altogether.

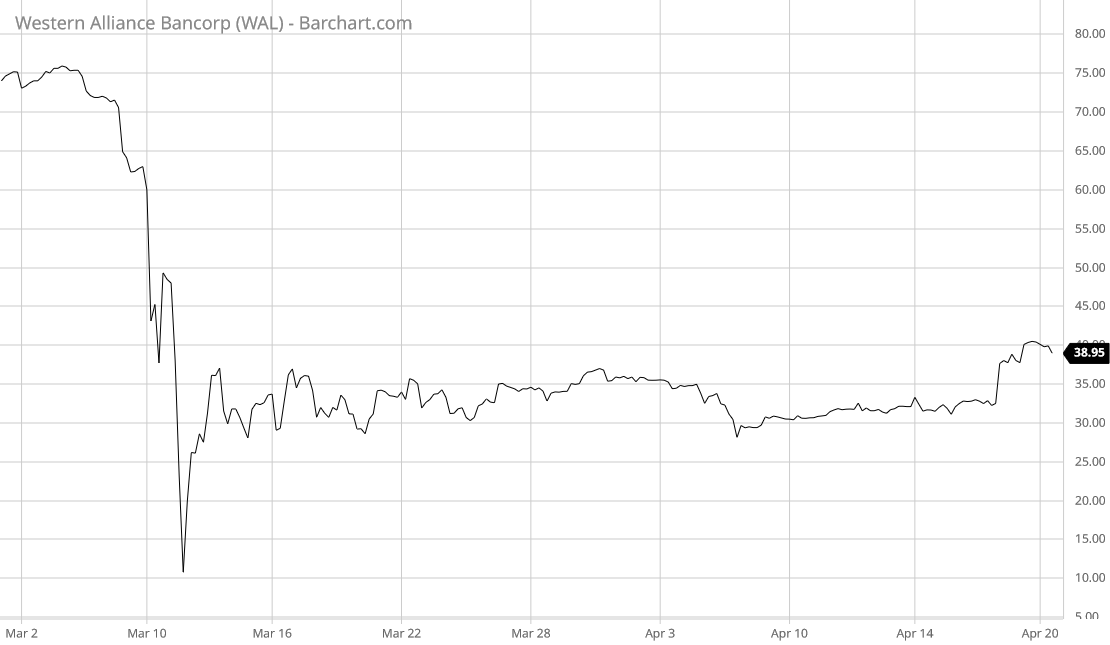

“We've returned to a lot more calm as it relates to depositors," Western Alliance CEO Kenneth Vecchione told analysts on a conference call.

Another disclosure that encouraged investors was that its percentage of deposits covered by the Federal Deposit Insurance Corporation had risen to 73% as of April 14, up from 68% at the end of the first quarter. The FDIC insures up to a limit of $250,000 per account.

What that means is Western Alliance is now less dependent on funding from depositors who are considered a greater flight risk during periods of uncertainty. Silicon Valley Bank was seized by regulators after its depositors pulled $42 billion in one day.

Has the space of a few weeks truly managed to heal the ruptures that were appearing in the financial system? Have we really gone from “crisis dead ahead” to “crisis delayed”, perhaps even to “crisis cancelled”?

Not exactly. Some things have improved, but the core drivers of credit crisis still remain.

The emerging “everything will be okay” narrative has two distinct features. The first one is that maybe—just maybe—Wall Street can tolerate interest rates and yields moving just a tad higher.

Another scenario might be that little changes: Credit markets could tolerate interest rates that prevailed before 2008. The Fed’s policy rate could increase a bit from its current 4.75%-5% range, and stay there for a while.

“A 5% interest rate is not going to break the market,” said Ben Snider, managing director, and U.S. portfolio strategist at Goldman Sachs Asset Management, in a phone interview with MarketWatch.

Certainly the Fed can raise the federal funds rate to 5%-5.25% at its next meeting. Wall Street absolutely anticipates exactly that happening.

Wall Street, despite many prior fulminations that such would be disastrous, seems almost resigned to the idea, comforting itself that many debtors used the Pandemic Panic period to refinance at low rates and so are positioned to ride out this wave of rising interest rates. Goldman Sachs analyst Ben Snider argues that many debtors from after the Pandemic Panic in 2020 have already refinanced their debt to lock in ultra-low interest rates.

Snider pointed to many highly rated companies which, like the majority of U.S. homeowners, refinanced old debt during the pandemic, cutting their borrowing costs to near record lows. “They are continuing to enjoy the low rate environment,” he said.

“Our view is, yes, the Fed can hold rates here,” Snider said. “The economy can continue to grow.”

The degree to which this is true largely depends on how responsive Wall Street chooses to be over interest rates and debt yields. While interest rates have moved up in recent days, for the past several months Wall Street has repeatedly rebuffed the Fed’s efforts to push interest rates up by raising the federal funds rate.

The Fed might be able to raise the federal funds rate to the 5.00%-5.25% range, but that is hardly an assurance that market interest rates will follow suit.

Even Europe is experiencing a flush of optimism over the trajectory of its own ongoing recession:

"I certainly think the situation in Europe is considerably better than I would have predicted a few months ago," said Jacob Kirkegaard, a senior fellow at the Peterson Institute For International Economics.

The International Monetary Fund (IMF) warned last week that inflation has remained persistent globally and downgraded its outlook for economic growth. But it slightly upgraded its growth forecast for the US and Europe in 2023.

Petya Koeva-Brooks, deputy director of the IMF Research Department, told Euronews last week she was surprised that euro area economies have adjusted to the economic shock and that the IMF is expecting a pick up of growth in 2024.

The second element of this narrative comes from how bank stocks have moved in recent days and weeks.

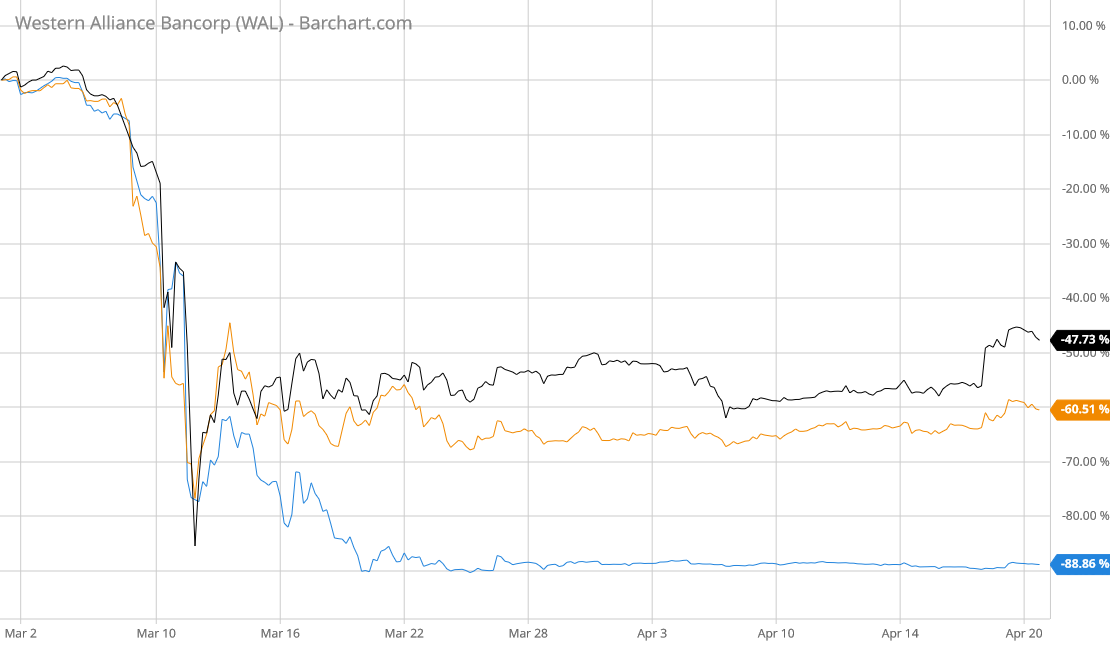

Western Alliance, the bank holding company whose shares have been under significant duress recently, managed to score a dose of upward momentum in its share price after announcing that bank deposits had actually grown recently, as well as the proportion of bank deposits covered by the FDIC.

Western Alliance’ stock was able to take fellow regional bank Pacwest Bankcorp along for the ride.

Even beleaguered First Republic Bank, while not seeing their stock rise, at least has not seen their stock fall—which is saying something, given the epic freefall the bank experienced in March.

While all three stocks have lost eyewatering amounts of share price and market capitalization since the beginning of March, all three appear to have at least found a market bottom—which suggests that the next moves will be upward.

Even the S&P 500 Financials index has been trending up in recent weeks.

That the financial sector has been strengthening of late can only mean that things are getting better and not worse, and that the credit crisis foretold in March may not come to pass after all….right?

Yeah….about that….

While there has been some good news on the banking front of late, and Wall Street is certainly feeling more optimistic about banks, as evidenced by the S&P 500 Financials index, not everything has simply turned the corner on crisis.

Bank portfolios of both government securities and mortgage-backed securities are still losing value.

If we look at the iShares US Treasury Bond Exchange Traded Fund, using that as a proxy for gauging current market value of US Treasuries overall, we see that the steady appreciation in value experienced during March has given way to renewed decline in April.

Similarly, the iShares CMBS Exchange Traded Fund, after recovering a portion of its value at the end of March, has been trending down in April.

The SPDR Mortgage Backed Bond ETF, which tracks residential mortgage-backed securities, has also followed this pattern.

Clearly, the valuation problems—and thus the unrealized loss dilemma which very nearly brought First Republic to its knees in March, has not gone away.

Nor is there any mystery why these valuation problems persist: Banks are carrying large books of real estate and commercial loans, many made when interest rates were far lower than today, and many of which are coming due, either to be repaid, refinanced, or face default.

With the bulk of outstanding bank real estate loans being in commercial real estate, the ongoing woes of the commercial real estate market, coupled with rises in interest rates over the past year offer easy understanding why Wall Street is skeptical of banks’ CMBS portfolios.

Despite Wall Street’s optimism, these things have not gone away.

What arguably has changed is the perceived pace and imminence of the coming crisis. Looking at the broad market value of Real Estate Income Trusts, as measured by the Dow Jones Equity All REIT index, the coming debt crisis is having a far more muted impact on perceived valuations of real estate portfolios than before.

With the index having recovered more than half of the value lost during March and then stabilizing, there is clearly a sentiment on Wall Street that commercial real estate loan defaults are not going to be as bad as previously feared.

A quick look at corporate interest rates tells us why Wall Street thinks that. Through mid-April, despite the turmoil of March, corporate high yield debt has been moving down in yield, rather than up.

Even investment grade debt yields are proving stubbornly resistant to the Fed’s rate hikes.

If rates trend down despite the Fed pushing the federal funds rate up, it necessarily follows that the magnitude of any credit crisis catalyzed by rising interest rates will be similarly muted.

At the same time, this past week, bank deposits increased substantially—and not just at Western Alliance.

Over the past week banks added more than $60 Billion in deposits, a dramatic change from the steady erosion of deposits that has been ongoing for the past year. Not only is Wall Street having greater confidence in banks and their capital structures, Main Street is as well.

However, increased confidence should not be taken to mean that Wall Street has figured out how to deal with the disconcerting challenges on bank balance sheets.

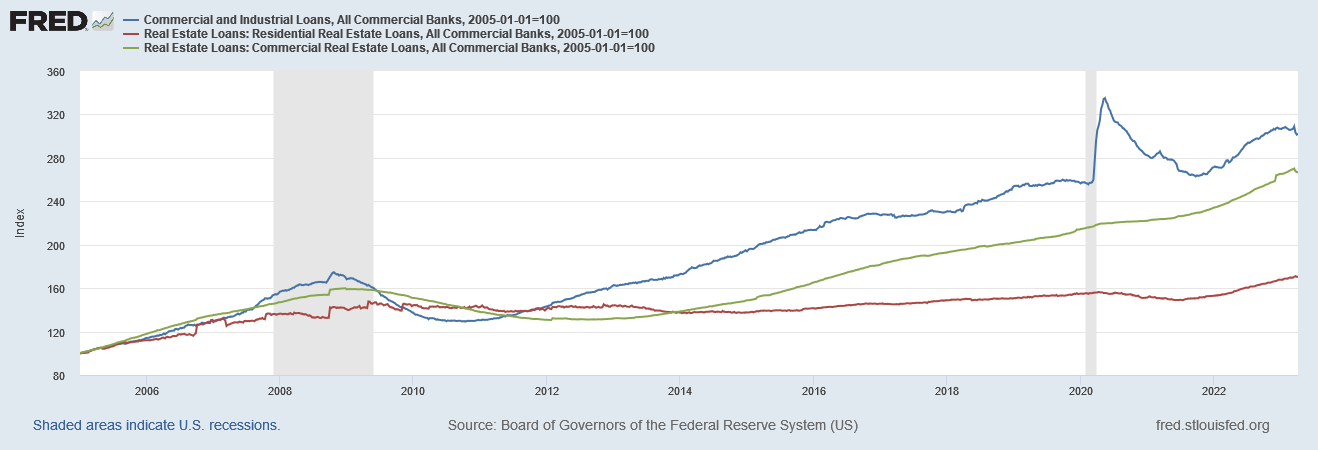

The unalterable economic reality is that commercial and commercial real estate loans have been growing proportionately faster than residential real estate loans. Even if we look back to the housing bubble era of the early 2000’s, and indexing the outstanding amounts of these loan categories to 2005, we see that even during the housing bubble commercial and commercial real estate loans grew at a faster pace than residential loans.

If we zero in from 2020 onward, we see that not only do commercial loans outpace residential loans, but the aftermath of the government-ordered Pandemic recession in 2020 saw a tremendous spike in commercial loans, with commercial real estate taking top honors

As the debts have not gone away, neither has the potential for a credit crisis and then a banking crisis. These are still on bank balance sheets and, if there is a wave of defaults, bank balance sheets will still take it on the chin.

As for why we should anticipate a correction in commercial real estate debt, we must realize that, in the aftermath of the 2007-2009 Great Financial Crisis residential real estate debt stabilized for a number of years, but commercial debt as well as commercial real estate debt did not.

Just before the 2020 recession, the value of both commercial loans and commercial real estate loans exceeded that of residential real estate loans. Unlike as with residential real estate, the pace of commercial indebtedness corrected briefly in 2010, and then largely resumed the same trajectory and pace as had been observed before the GFC. Arguably, an important lesson in humility was learned by holders of residential real estate debt but not holders of commercial real estate debt.

That commercial loans spiked just after the 2020 recession has not helped the situation.

While not the frothiest of bubbles, this rise in commercial indebtedness—in especially commercial real estate indebtedness at the same time commercial real estate values themselves were being demolished by the sudden imposition of remote working and lockdown policies—presents a fairly definite disequilibrium that, eventually, must correct. There simply is too much commercial and commercial real estate debt floating around bank balance sheets, debt that will be hard to refinance and extend in an environment of rising interest rates.

There is a credit crisis coming. With a correction in commercial indebtedness “baked in” to the finance sector, a credit crisis is unavoidable. It will happen.

What is as yet unknown is how large the correction will need to be, and how quickly it will arrive. These aspects will be determined by where interest rates move, both in the run-up to the next Federal Reserve rate hike in May and beyond.

This is a murkier question than the media presents, for the simple reason that, as has been noted many times on this Substack, interest rates have not been following the lead of the federal funds rate for several months now.

Largely in response to the failure of Silicon Valley Bank and the onset of the media pearl-clutching over bank balance sheets in early March, Treasury yields self-corrected by as much as a full percentage point, and have only gradually moved to recover since.

While the financial media may enjoy speculating that there would not be a meltdown if “interest rates” reached 5%, in fact there is a very good reason to suspect that there would be something of a meltdown: we already had one in early March. Granted, yields dropped, the government stepped in with bandaids and hugs for crying bankers over their skinned knees, and everything was made magically better, but that does not change the fact that Wall Street did have a moment when it lost confidence in the banking system overall. Nor does it change the fact that, even with the bandaids and the hugs for crying bankers over their skinned knees, Wall Street confidence has not fully recovered: the S&P 500 Financials index is still down over 6% from where it was at the beginning of March even with recent appreciation trends.

Even more telling is the fact that the S&P 500 Financials Index is down over 15% since the start of 2022.

Interestingly enough, the index also began appreciating right around the time that market interest rates stopped rising last fall, and reversed when market rates briefly moved up in February, and began appreciating again after the March correction in market interest rates.

Regardless of what Wall Street analysts choose to believe, banks and bank stocks have not fared well when market interest rates move much above the 5% threshold.

As of market close yesterday, yields on 1-Year Treasuries stood at 4.77%.

Yields on 2-Year Treasuries stood at 4.18%.

Yields on 10-Year Treasuries stood at 3.55%.

If recent financial history decides to rhyme, should 1-Year and 2-Year Treasury yields move above 5%, and should 10-Year Treasury yields move above 4%, there will be fresh blood in the financial waters, and fresh turmoil. If recent financial history decides to rhyme, should these things happen there will be a new banking crisis.

No matter how the narrative in the financial media goes, things have changed very little since SVB’s failure in early March. No matter what the financial media chattering class wants to believe, the banking crisis has not been cancelled, but merely delayed. When market interest rates rise high enough—and not too much higher than where they are now—the banking crisis will return with a vengeance.

I agree about the delayed banking crisis. If bank portfolios are still losing value, how could there *not* eventually be a crisis? I get the sense that it’s been postponed *only* because “government stepped in with bandaids and hugs for crying bankers over their skinned knees” (I laughed out loud at that phrasing - thanks!).

Great article. BRAVO

I'm just glad to have a mortgage free home now that I'm retired. And reasonable tax rates (if any tax could be called reasonable) at last count (but they did go up almost 30%).