If China's "First Wave" Of COVID Is Almost Over, What Happens Now?

How Does Beijing Restart A Stalled Economy?

Anyone who has paid any attention at all to China’s economy already knows that getting past their current COVID infection wave was only step number one. Once cases, hospitalizations, and deaths are trending down, China still has the problem of how to restart a stalled economy.

The Chinese economy stumbled in 2022, numbers released Tuesday show, in one of its worst performances in decades as growth was dragged down by numerous Covid lockdowns followed by a deadly outbreak in December that swept across the country with remarkable speed.

While the corporate media finds it convenient to blame China’s economic woes on Zero COVID and the subsequent “first wave” of infections once Zero COVID was ended, China’s economic ills stretch back well before the world even heard of COVID, or the Wuhan Institute of Virology.

China’s rise to economic prominence had been powered by exports of all manner of manufactured goods, with the value of Chinese exports having risen from a few billion USD in 2000 to well over 200 billion USD in 2015—at which point export growth largely stalled out until after the 2020 COVID lockdowns.

China’s index of new manufacturing orders in fact had peaked before the 2008 Great Financial Crisis, and has never reached similar highs since.

In fact, China’s growth in industrial production peaked in 2010, and had been slowing from then up until the COVID lockdowns of 2020.

Long before SARS-CoV-2 made its entry onto the world stage, China’s economy was showing signs of gradual stagnation and decline—in 2019 there was no denying that China’s best economic years were already behind it.

It is against this backdrop of gradual long-term decline that China’s current economic conditions must be assessed. Beijing has to not only resolve how to address the immediate dislocations brought on by Zero COVID and the pandemic, but also how to contend with an economic model that has been working less and less well for years.

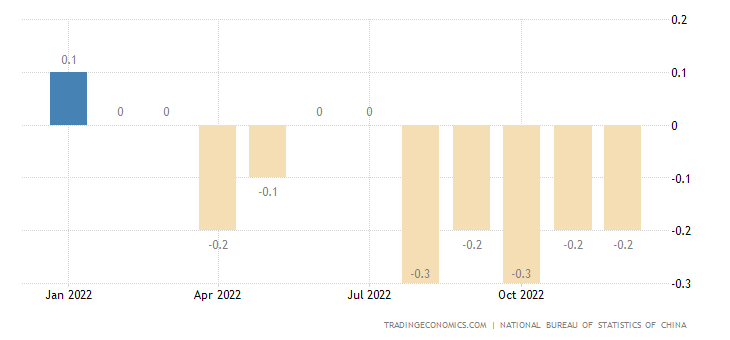

It was easy to blame November’s slump in industrial production and retail sales on Zero COVID policies. People who are locked down cannot go to work nor can they go shopping.

Certainly the prevailing message of the corporate media is that the poor November data was the result of Zero COVID.

China's economy lost more steam in November as factory output slowed and retail sales extended declines, both missing forecasts and clocking their worst readings in six months, hobbled by surging COVID-19 cases and widespread virus curbs.

This does not explain, however, the additional declines posted for these sames statistics in December, when retail sales dropped 0.14% from November’s tally, and showed a 1.8% decline year on year.

For most of December, zero COVID restrictions no longer applied.

We should note, however, that although the formal restrictions were removed, it has been reported that many Chinese citizens were reluctant to emerge from their homes into a brave new world without Zero COVID policies in effect, thereby keeping people out of shops and hindering sales.

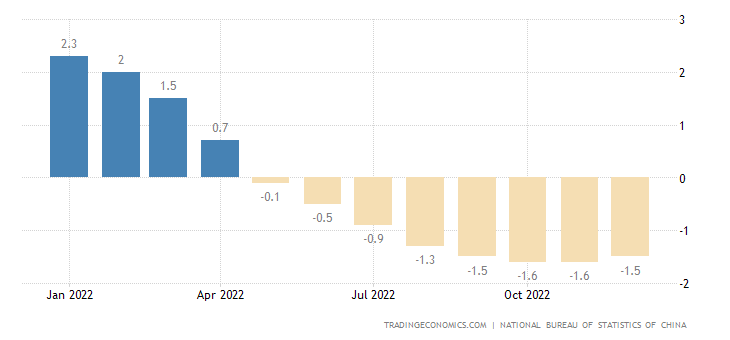

The reluctance of the Chinese people to “return to normal” does go a long way towards explaining December’s drop in industrial output, which further slowed from November’s 2.2% growth to 1.3%.

That reluctance will fade, however, and already China’s steel industry is reporting greater activity for January.

China's major steel mills saw their average daily output of crude steel grow 0.51 percent in early January from that recorded in late December 2022, industrial data showed.

Signs of economic life extend beyond the steel industry, as electrical power generation—a proxy for overall levels of economic activity—rose in December.

China's power generation rose 3 percent year on year to 757.9 billion kilowatt-hours in December 2022, data from the National Bureau of Statistics (NBS) showed.

Power generation actually rose 13.7% month on month from November.

That economic activity is increasing in China post-Zero COVID seems fairly well demonstrated, and while some of that activity may be paused for the Lunar New Year holiday, it seems reasonable to anticipate that China will continue to see a return of economic life once the holiday has passed.

That economic life is returning is not to say that economic health will be returning as well. China’s real estate bubble remains burst, and prospective Chinese homebuyers remain skittish and skeptical of the housing market as a whole, with the home price index dropping another 0.2% in December, replicating November’s decline.

The year’s worth of declines shows up in the year on year numbers as well, with December being the 8th consecutive month new home prices declined year on year.

Despite falling home prices, total new home sales for December were the worst for that month since 2017.

Now that Chinese homebuyers have seen the effects of an economic bubble on housing prices, they are understandably gun-shy about buying—and China’s stimulus efforts in the housing sector are not likely to change that. Consequently, further declines in housing are anticipated through the first six months of 2023.

"China's real estate market is expected to bottom out in the second quarter of 2023 and major cities are likely to take the lead in market stabilization," said Lian Ping, chief economist at Zhixin Investment and head of the Zhixin Investment Research Institute.

"The overall housing finance policy will further rebound this year to boost housing demand. Mortgage rates are expected to remain at a record low and commercial banks will accelerate mortgage loan extensions," Lian said.

That it will take more than six more months for government stimulus policies to have a stimulative effect on housing markets says quite a bit about Beijing’s ultimate helplessness where the housing crisis is concerned.

China’s property industry was among the biggest drags on growth. Investment in the sector fell 10.0 percent year-on-year in 2022, the first decline since records began in 1999, and property sales slumped the most since 1992, NBS data showed, suggesting that the Chinese regime’s support measures were having minimal impact so far.

The real estate market will move back up when it wants to, and not one moment sooner, it seems.

While real estate continues to sag, Chinese exports are also in a slump, having declined 9.9% year on year.

Chinese officials announced on Friday that exports fell 9.9 percent in December compared with the same month a year earlier, including nose-dives of 19.5 percent to the United States and 17.5 percent to countries in the European Union.

China’s high-water mark for exports came in November of 2021, and the long-term trend has been down ever since.

Without a rise in exports, China’s “reopening” will come to naught. It does not help an economy to produce goods that are not then sold.

Moreover, China is facing increasing pressure from other developing economies such as Mexico, which have been making inroads into China’s export volumes in recent years, a trend accelerated by the COVID pandemic.

During the first 10 months of last year, Mexico exported $382 billion of goods to the United States, an increase of more than 20 percent over the same period in 2021, according to U.S. census data. Since 2019, American imports of Mexican goods have swelled by more than one-fourth.

In 2021, American investors put more money into Mexico — buying companies and financing projects — than into China, according to an analysis by the McKinsey Global Institute.

China is reopening into a world of increased regional competition, competition which will eventually end China’s status as “the world’s factory.”

Government stimulus along cannot change those macroeconomic trends. Despite Xi Jinping having abandoned all of his signature economic policies, from “common prosperity” to the infamous “three red lines” for property developers, the Chinese economy is still moribund and stagnant.

The much looked-for economic “surge” has yet to happen.

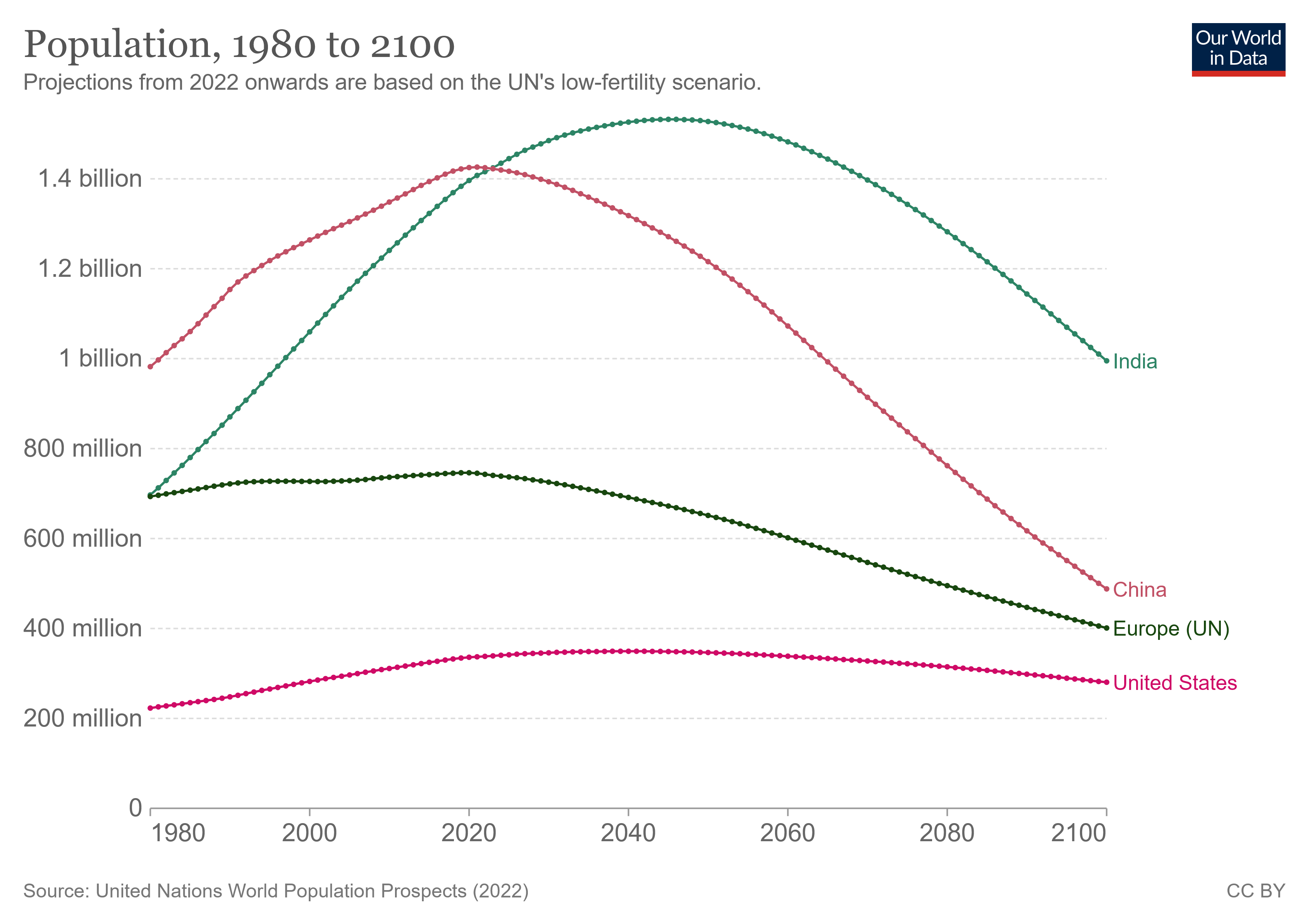

The degree to which it can happen at all is itself an open question. Hanging over all of China’s negative economic data is its severely negative demographic data: China is losing people.

On Tuesday, China reported that its population fell in 2022, for the first time in generations. At the same time, the government announced that the growth rate of the Chinese economy slowed sharply in 2022, even before an end to the country’s zero-COVID strategy unleashed a wave of infections that is tearing through the population.

Neither shifts in immigration nor emigration can account for the loss of 850,000 Chinese people in 2022. This decline is solely the result of deaths exceeding births.

One result of this demographic shift is that China’s population is getting older, with more and more citizens aging out of the “working” demographic over time. China has one of the most rapidly aging populations in the world, with its median age having overtaken that of the United States as of 2021, and will soon surpass Russia and the United Kingdom as well, leaving only Japan with a higher median age.

With one of the lowest fertility rates in the world, China’s population could shrink by more than half by the end of the century (depending on future fertility rates), a greater relative decline than either Europe or the United States would undergo over the same time frame.

As the Chinese population shrinks, it will also continue to age, with the result that by 2040 China will have the same proportion of population 65 years and up as Europe, with a smaller proportion of population 15-24 years of age than the United States.

The number of workers available to spur any level of economic resurgence is shrinking. The number of workers to assemble iPhones and produce steel and all manner of other exports is shrinking. The fewer the number of workers, the less amount of economic surge is possible, and every year at least through the end of the century, China will have to make do with a smaller and smaller number of workers.

The corporate media narrative is that once China fully “reopens”, and once its COVID waves recede, the Chinese economy will experience something of a post-pandemic boom, which will in turn lift the global economy.

While there is almost certainly going to be an increase in economic activity, the degree to which the Chinese economy is likely to surge in any sort of economic boom is highly problematic. Zero COVID was never the only impediment hindering the Chinese economy. COVID itself was never the major impediment hindering the Chinese economy.

By far the major impediment to economic growth in China has been—and likely will continue to be—government policies and economic interfence. It was the infamous “One Child” policy that created China’s current demographic crisis. It was government “stimulus”—state support of easy lending to property developers—that created China’s property bubble. China’s current economic woes are, in almost every regard, self-inflicted wounds.

Thus far, Beijing has shown little indication that it has learned its lesson—or that it can ever learn the lesson that governments are the worst possible economic actors around. Whenever government meddles in economic matters, the economy itself suffers. Yet China continues to be the major economy in the world with the greatest degree of government meddling, micromanaging, and control.

China is indeed “reopening”. However, the economic potentials attendant upon that reopening are a good deal smaller than the corporate media hopes, or than the corporate media hypes. China’s economy is not likely to continue to collapse, but neither is it likely to experience significant expansion such as it has enjoyed in the past.