Last month’s inflation report was viewed by some as a leading indicator that the Federal Reserve may yet pull the proverbial rabbit out of the hat by succeeding in crafting a “soft landing” for the US economy, where Fed-caused demand destruction is pushing the economy deeper into recession.

Wall Street’s biggest hedge funds and money managers, however, are almost uniformly unimpressed, with almost all of them quite accurately predicting recession and stagflation for the near term.

On the most optimistic corners of Wall Street, promising inflation data over the past week or so suggest the Federal Reserve may accomplish a soft landing after all.

Yet no such belief prevails among the big money managers, who are betting that an economic downturn riddled with still-hot price pressures will define trading next year.

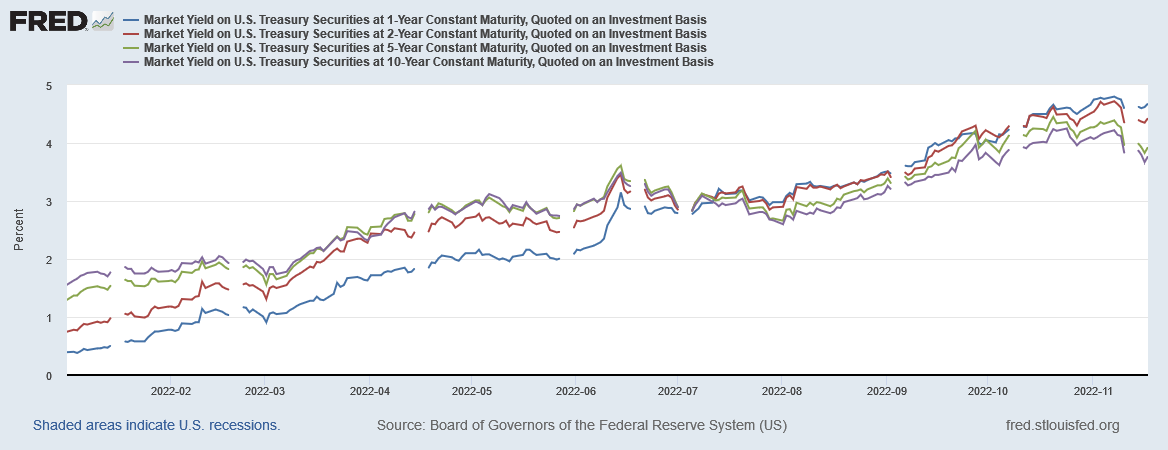

With a closely watched section of the Treasury yield curve sending fresh recession signals, stagflation is the consensus viewpoint among a whopping 92% of respondents in Bank of America Corp.’s latest fund-manager survey.

Wall Street may at last be catching up to the reality that the US economy is already in recession, even as inflation stubbornly refuses to retreat but a few steps from 40-year highs.

That stagflation was the most likely scenario for the US economy has been apparent for months, even as Wall Street has tried mightily to pretend that it is not.

Instead of a “Powell put”, or a “Powell pivot”, where the Fed backs off rate hikes and turns to looser monetary policy in order to support Wall Street, the prevailing Wall Street prognostication is of a “Powell push”, where the Fed continues to hike rates long past the point where they’re doing anything to bring down inflation.

At the same time, Citigroup Inc. is painting a scenario of the “Powell Push” in which the Fed will be compelled to hike even if growth plunges, while BlackRock Inc. sees no prospect of a soft landing either in the US or Europe.

Yet even this should have long been understood to be the coming reality on Wall Street. The lower part of the Treasury yield curve has been inverted—where shorter term maturities paradoxically command higher yields than longer term maturities—for several months at this point.

Moreover, the reality of a contracting US economy has been apparent in the macroeconomic data for the past several months as well, with manufacturing PMIs showing steady decline since the middle of 2021.

Service PMIs have not fared any better.

Declining US manufacturing capacity utilization has also been an indicator of a contracting US economy.

Almost as soon as the Fed begain raising rates, manufacturing in the US began to contract—grim evidence of just how fragile the US economy has been all along.

The question ultimately is not whether Wall Street finally realizes that the Fed is not going to ease up on inflation any time soon, but whether Wall Street will demonstrate the financial discipline to unwind derivative positions which are going to be at ground zero of the coming liquidity crunch and credit crisis.

The US is in a recession. The Fed’s rate hikes are making that recession worse not better. Wall Street appears to be making peace with that fact, although it remains to be seen if Wall Street will take any measures on their own to ease the inevitable pain.