Powell's Paradox: Curing Inflation Will Create A Money Shortage

Can The Fed Control What They Do Not Comprehend?

While Jay Powell has dug in his heels on inflation, determined to crush inflation by any means necessary, economic recession be damned, a counter-intuitive fear has begun to build on Wall Street: the Fed’s anti-inflation strategy means there will not be enough cash money available to resolve market obligations when they occur.

That’s right. The Wall Street casino is fearful of not having enough cash on hand to settle up all bets when the market crashes—so it constantly wants more cash from the Fed (and gets it).

With the Fed doubling the pace at which its bond holdings will “roll off” its balance sheet in September, some bankers and institutional traders are worried that already-thinning liquidity in the Treasury market could set the stage for an economic catastrophe — or, falling short of that, involve a host of other drawbacks.

In corners of Wall Street, some have been pointing out these risks. One particularly stark warning landed earlier this month, when Bank of America BAC, -0.17% interest-rate strategist Ralph Axle warned the bank’s clients that “declining liquidity and resiliency of the Treasury market arguably poses one of the greatest threats to global financial stability today, potentially worse than the housing bubble of 2004-2007.”

The Fed Wants To Shrink Its Balance Sheet And Wall Street Is Scared

Specifically, Wall Street is terrified about what will happen as the Fed begins to shrink its ginormous balance sheet—which it has barely begun, with scant progress thus far.

Just the small reduction made this year is enough to give Wall Street a case of the vapors.

Short of an all-out blowup, thinning liquidity comes with a host of other drawbacks for investors, market participants, and the federal government, including higher borrowing costs, increased cross-asset volatility and — in one particularly extreme example — the possibility that the Federal government could default on its debt if auctions of newly issued Treasury bonds cease to function properly.

Waning liquidity has been an issue since before the Fed started allowing its massive nearly $9 trillion balance sheet to shrink in June. But this month, the pace of this unwind will accelerate to $95 billion a month — an unprecedented pace, according to a pair of Kansas City Fed economists who published a paper about these risks earlier this year.

The Federal Reserve has been printing money like mad since 2008, and went off the deep end with it in 2020, and the markets are worried there won’t be enough as the Fed tries to pull some of that back.

Just how much money does Wall Street need?

The Challenge: Liquidity

The crux of the issue is that, despite all the dollars the Fed has wished into being over the past 14 years, the markets are concerned about point-in-time dollar shortages known as “liquidity crises”.

To understand why this is, a couple of definitions are in order:

“Financial Liquidity”1 is the ability to turn an asset into cash (“liquidated”).

Regardless of how much cash money is in the money supply overall, if that cash is not where it needs to be when assets need to be a liquidity crisis develops. A “liquidity crisis”2 occurs when market actors do not have cash available to complete a transaction.

Regardless of how much money the Federal Reserve creates, if it’s not in the “right hands” at the “right time”, asset transactions cannot be completed, and financial markets lock up. That the banks which support Main Street businesses are the same banks playing on Wall Street expands that problem to Main Street.

Most economists view the 2008 Great Financial Crisis (GFC) as a liquidity crisis.

Even with these very divergent origins, the GFC and pandemic crisis impacted financial markets in some similar ways.

First, both resulted in an extraordinary increase in the demand for dollar liquidity. The demand arose out of both immediate funding needs and the desire to raise precautionary liquidity. The supply of liquidity was also curtailed as firms that normally lend instead stockpiled liquidity to meet potential future payment needs. During both crises, this surge in demand for U.S. dollars was global in nature and had significant spillovers to domestic funding conditions.

The concern within financial markets today is that, as the Fed tightens the money supply to control inflation, there will not be enough dollars at crucial points to satisfy dollar liquidity demands. In other words, there is a perceived risk on Wall Street that, as the Fed reduces the overall supply of money, that there will not be sufficient dollars available to participants in various asset transactions to allow those transactions to be completed.

It’s Not Just Stocks And Bonds. It’s Derivatives

Where liquidity demands wander, Alice-like, through the looking glass, is when investors move beyond the mundane buying and selling of traditional stocks and bonds, and apply more esoteric investment strategies revolving around what are called “credit derivatives”3. Credit derivatives are financial instruments that turn various forms of credit risk (i.e, the chance that you won’t get the money you loan out back), into a financial transaction and therefore a way to mitigate credit risk.

A credit derivative is a financial contract that allows parties to minimize their exposure to credit risk. Credit derivatives consist of a privately held, negotiable bilateral contract traded over-the-counter (OTC) between two parties in a creditor/debtor relationship. These allow the creditor to effectively transfer some or all of the risk of a debtor defaulting to a third party. This third party accepts the risk in return for payment, known as the premium.

Credit derivatives were the instruments at the epicenter of the 2008 Great Financial Crisis. As financial commentator and blogger Michael Snyder puts it:

Most Americans don't realize it, but derivatives played a major role in the financial crisis of 2007 and 2008.

Do you remember how AIG was constantly in the news for a while there?

Well, they weren't in financial trouble because they had written a bunch of bad insurance policies.

What had happened is that a subsidiary of AIG had lost more than $18 billion on Credit Default Swaps (derivatives) it had written, and additional losses from derivatives were on the way which could have caused the complete collapse of the insurance giant.

So the U.S. government stepped in and bailed them out -- all at U.S. taxpayer expense of course.

There were more parties involved than just AIG, but the essential dynamic was that entire categories of derivative contracts were turning toxic as a result of the 2005-2007 housing bubble and attendant subprime mortgage crisis.

The GFC was precipitated by a housing market shock that was amplified by weak underwriting standards and highly leveraged financial intermediaries—in particular, in subprime mortgage finance. The crisis unfolded over an extended timeline, punctuated by events that revealed significant vulnerabilities among financial institutions, including in the banking sector.

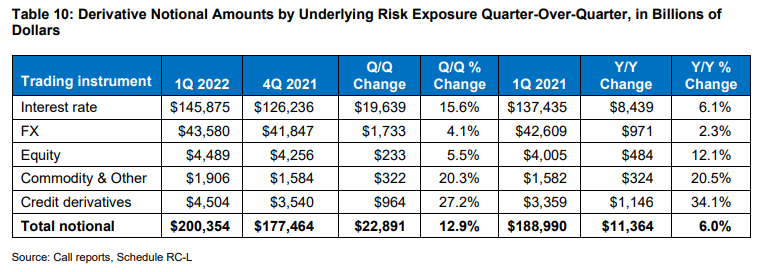

How big are these categories of derivative contracts? According to the Office Of the Comptroller of the Currency, as of the first quarter of 2022, the notional value of all credit derivative contracts within its purview was 200 Trillion dollars.

Worldwide, the total notional amount of dollar-denominated derivative contracts is estimated by some to be over a quadrillion dollars.

Nobody knows for certain how large the worldwide derivatives market is, but most estimates usually put the notional value of it somewhere over a quadrillion dollars. If that is accurate, that means that the worldwide derivatives market is 20 times larger than the GDP of the entire world.

As of July, the amount of dollars calculated to be in the M2 Money Supply is just over 21 Trillion dollars.

If just the amount of derivatives tracked by the OCC had to be settled all at once, there is only about 10% of the number of dollars necessary to complete all those transactions at the notional level. That inability to convert all those derivative assets into their cash equivalents is what produces a “liquidity crisis”.

This example is, obviously, an extreme and highly improbable case, but one of the lessons Wall Street took from 2008, rightly or wrongly, is the presumed need for sufficient cash to be available to settle derivative contracts en masse in the event of a financial shock vis-a-vis the housing bubble and subprime mortgage crisis.

Money Supply Increases Balanced By Velocity Collapse

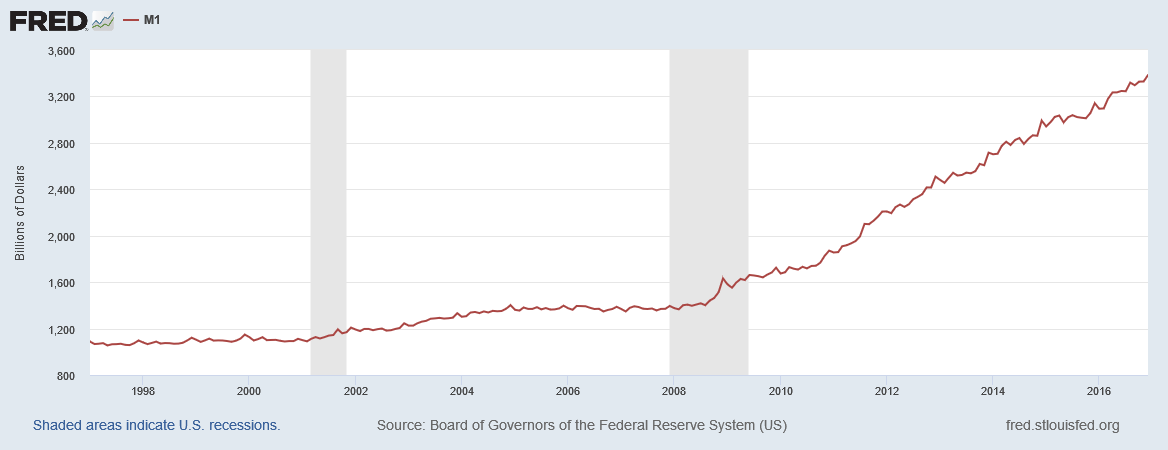

The Federal Reserve responded to the liquidity crisis of 2008 with what was then an unprecedented injection of liquidity into financial markets. Dollars were literally created ex nihilo to allow an orderly unwinding of the collapsing derivative markets, resulting in an increase in the pace of M1 money supply expansion that continued well after the crisis had passed.

As the M1/M2 money supply chart near the beginning of this article illustrates, the Fed responded to the 2020 pandemic lockdown and ensuing recession with a veritable torrent of liquidity, more than doubling the M1 money supply almost overnight. The rationale was the same as for the 2008 Great Financial Crisis—to ensure that markets had enough dollars to unwind disrupted and dislocated markets reeling from the multiple exogenous shocks of the near total shutdown of the global economy.

How did these mass injections of liquidity—mass “printing”4 of dollars not produce extreme hyperinflation at the time? In a word: velocity.

Corollary to the money supply is the velocity5 of money—the number of times money changes hands within an economy. The simple formula for money velocity is GDP divided by the total supply of money (M1 or M2).

As the Federal Reserve was creating dollars to meet Wall Street’s liquidity demands, those dollars were quite literally piling up on Wall Street. They were not changing hands into the broader economy. As a consequence, the velocity of money, which for the M1 money supply metric peaked just before the 2008 GFC, began a decline which persisted until the 2020 pandemic and lockdown induced recession, when it simply fell off a cliff.

Because the money created never left Wall Street, it never resulted in any inflationary pressure. Thus the Fed felt free to create money in an unrestrained fashion, because the inflation accepted wisdom said would arise from such profligacy never materialized.

Until now.

A Financial Pressure Cooker

Because the liquidity demands of Wall Street have since the early 2000’s been met by an accommodating Federal Reserve, which as expanded the money supply while reducing money velocity, a financial “pressure cooker” has emerged. After bottoming out in the 3rd Quarter of 2021, money velocity has been trending up ever since. If money velocity continues to increase, with the M1 and M2 money supply metrics still at record levels, the expected result within monetary theory is greatly increased inflation.

While the thesis that money supply alone explains the rise of inflation from 2021 onward is problematic at best—and certainly the complete impotency of Powell’s interest rate hikes to date call this thesis into question at the very least—over the longer term rising money velocity combined with record money supply levels will unquestionably have a general inflationary impact on the US economy.

The proximate source of the current rounds of inflation being experienced in the US and around the world are demonstrably exogenous supply shocks—China's Zero COVID, drought, the Russo-Ukrainian War, et cetera—which greatly decrease the supply of critical goods everywhere. Yet while these supply shocks require us to take a more nuanced view of the Friedmanite concept that inflation is a monetary phenomenon, they do not eliminate the potential for money supply excess coupled with velocity increases to add further inflationary pressure.

Thus the Federal Reserve is face with a paradox: to corral inflation with the limited theoretical understanding and tools at its disposal, it must raise interest rates to reduce demand and shrink the money supply, yet if it succeeds in shrinking the money supply it will precipitate a replay of the 2008 Great Financial Crisis, only at much greater notional dollar volumes ($200 Trillion and counting).

While not tampering with interest rates would avoid an immediate catalyzing of the crisis, if the Fed does not reduce the money supply it must suppress money velocity, or else risk long-term structural inflation. If the Fed does reduce the money supply, credit derivatives markets are left exposed to an eventual liquidity crisis, which with the current unstable geopolitical situation is likely to happen sooner rather than later.

Can the Federal Reserve resolve these contradictory demands and navigate to a safe and soft landing for the US economy? It is possible, but I suspect it is highly improbable. To do that the Fed would have to first understand the paradox in which it finds itself, and thus far there is no indication from Jay Powell or anyone else within the Federal Reserve of such comprehension.

Mueller, J. Learn About Financial Liquidity. 19 July 2022, https://www.investopedia.com/articles/basics/07/liquidity.asp.

Investopedia Team, and T. Walters (Ed.). Liquidity Crisis Definition. 6 Dec. 2020, https://www.investopedia.com/terms/l/liquidity-crisis.asp.

Chen, J. Credit Derivatives: How Banks Protect Themselves If You Default. 5 Apr. 2022, https://www.investopedia.com/terms/c/creditderivative.asp.

In this age of electronic commerce, dollars are not created via an actual printing press, but are summoned into existence electronically, as bits and bytes in a bank computer.

Chen, J. Velocity of Money Definition. 30 Oct. 2021, https://www.investopedia.com/terms/v/velocity.asp.

AIG wasn't in trouble because they had written a bunch of bad insurance policies?

Uhm, credit default swaps, interest rate swaps, and other such derivatives are essentially unregulated insurance policies that lack any meaningful capital to back them.