Reality Checks? Job Openings Decline Does Not Alter Net Impact Of Actual Hirings And Firings

The Fed Wants More Unemployment. So Far It Isn't Getting It.

In keeping with the corporate media’s persistent refusal to consider any paragraph but the first in a Bureau of Labor Statistics news release, the media made a big deal about the apparent decline in job openings in the Job Openings and Labor Turnover Summary for February.

The number of job openings decreased to 9.9 million on the last business day of February, the U.S. Bureau of Labor Statistics reported today. Over the month, the number of hires and total separations changed little at 6.2 million and 5.8 million, respectively. Within separations, quits (4.0 million) edged up, while layoffs and discharges (1.5 million) decreased. This release includes estimates of the number and rate of job openings, hires, and separations for the total nonfarm sector, by industry, and by establishment size class.

That the seasonally adjusted number of job openings was below 10 million was deemed by the corporate media to be of major significance, even as the rest of the data was largely ignored.

Job openings fell below 10 million in February for the first time in nearly two years, in a sign that the Federal Reserve’s efforts to slow the labor market may be having some impact.

Of course, since almost all of those unfilled jobs likely never existed (or, rather, employers never really cared if the jobs ever got filled), the decline in job openings doesn’t really say anything at all. By far the more illuminating aspect of the JOLTS report is the characterization of hires and total separations as “little changed.”

The lack of net effect on hiring and firing means the Fed’s strategy of hiking interest rates is not working.

I would like to digress for a moment to touch briefly on the BLS’ seasonally adjusted metrics vs their unadjusted data.

When there is a discernible ebb and flow throughout the year to a particular data set, seasonal adjustments are a valid statistical method for removing those seasonal patterns from a data set, to allow more substantive trends to come to the fore.

Readers will recall that, in the past, I have expressed more than a little cynicism about how the BLS seasonally adjusts some of its jobs numbers, particularly in the monthly employment situation reports.

However, that the BLS arguably miscalculates—or perhaps misuses—seasonal adjustment factors for certain metrics does not invalidate seasonal adjustment methodologies overall, nor does it mean that no seasonally adjusted data from the BLS has any merit. It does mean that seasonally adjusted data should be scrutinized to ensure that seasonal adjustments are reasonable and supportable before relying on seasonally adjusted data.

When we examine the seasonally adjusted hiring metrics, for example, with the unadjusted data, we see that the seasonally adjusted metric is for the most part merely smoothing out the seasonal highs and lows, without significantly distorting the overall trend line.

Thus we may accept the seasonally adjusted data from the JOLTS report as a realistic elimination of seasonal influences to reveal the broader macro trends in hiring and firing. While on the one hand we should at least take note of the trends shown by the unadjusted data…

…The seasonally adjusted metrics allow us to work directly with the JOLTS assessment that hiring and firing were “little changed”.

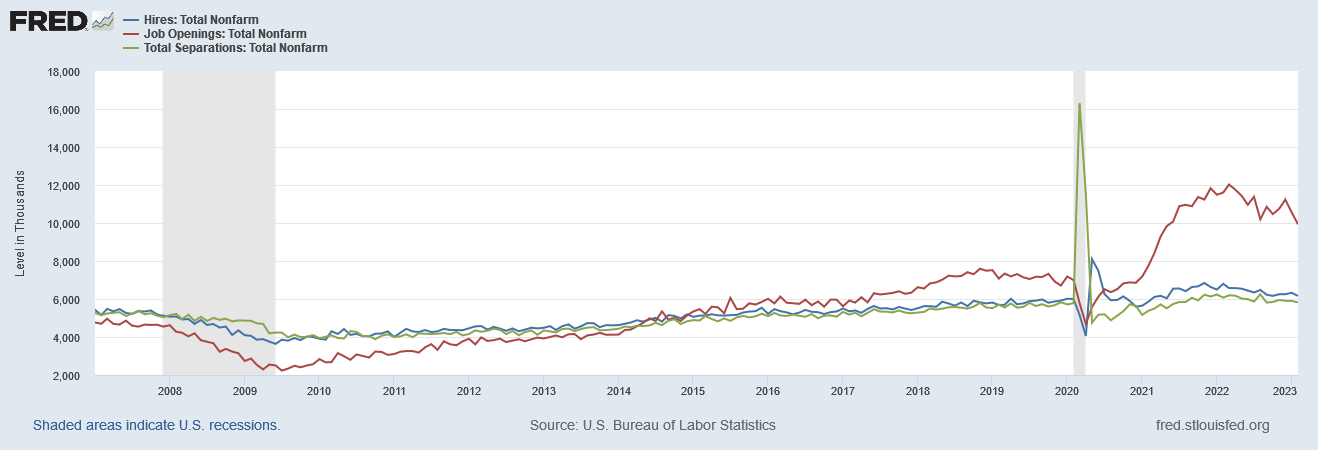

What is important here is to note the extent to which the hires and total separations data have almost always shown little change. Both before the government-ordered recession of 2020 and after, overall hiring and firing have largely remained within fairly narrow statistical boundaries.

Even if we look farther back, to before the 2007-2009 recession, while there is a significant decline in hiring and total separations during that recession, overall, the trend for both has never varied much either up or down.

Hiring and firing has, for the most part, been reported by the BLS as being fairly consistent.

What has not remained consistent are the number of job openings. Even prior to the 2020 recession, there was a shift from the number of reported job openings being less than the number of new hires and separations right after the 2007-2009 recession to being significantly more than the number of new hires and separations just before the 2020 recession.

Yet even with the pre-2020 rising trend in job openings, after the 2020 recession the number of job openings accelerated dramatically, completely out of proportion to the levels of job openings reported prior to the recession. We can see just how far out of proportion the job openings numbers have been by indexing the job openings, hires, and total separations metrics to January of 2017.

Not only did the explosion in job openings not occur until January of 2021, by midsummer of 2021 the number of job openings was running double the reported level in January, 2017.

This, of course, is one more reason to always doubt the headline numbers on jobs reports.

Given that the acceleration happened over six months after the 2020 recession had presumably ended, it is difficult to ascribe the acceleration in job openings to any aspect of post-recession “recovery” (particularly when the hiring levels showed no such recovery trend).

As a direct consequence of this, we are able to conclude just from the JOLTS data itself that the reported numbers of job openings is simply not realistic. Hiring and firing have been largely steady in the US for years (at least, the BLS has reported them that way). At no point since the 2020 recession do we see any upward trend in hiring reflective of the greatly increased numbers of available jobs. If there was a true pressure to hire more people, it is highly improbable that this pressure would not be expressed somehow in the rate of new hires.

The minimal shifts in either hiring or separations also is testament to the inefficacy of the Federal Reserve’s rate hiking strategy. The separations data in particular highlights this reality.

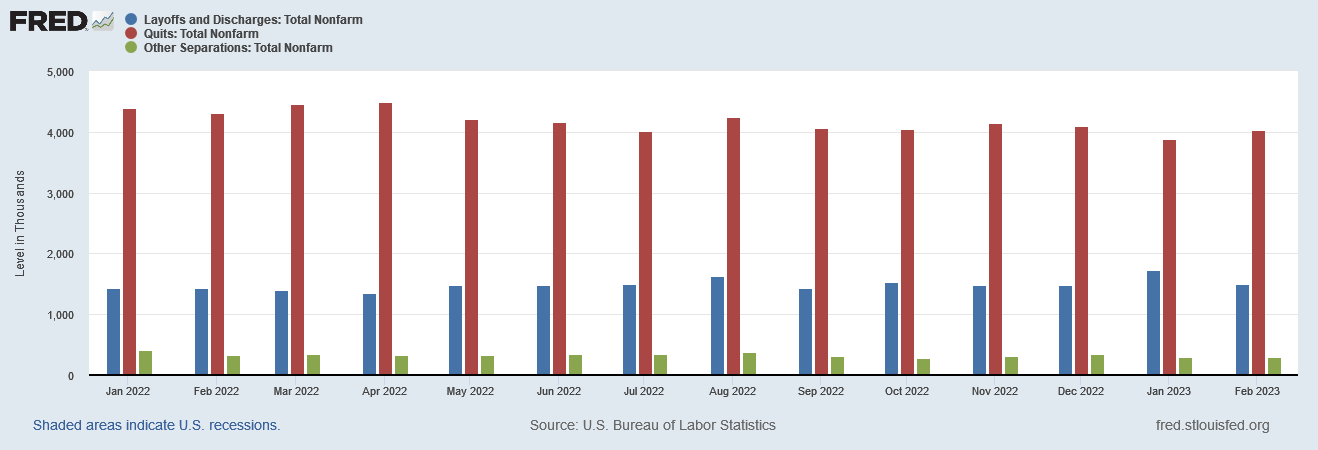

Contrary to what the Fed has hoped to see, not only have total separations remained largely consistent, but even the breakdown between layoffs, quits, and other separations has largely stayed the same.

In every month since January 2022 and before, more than twice as many people have quit their jobs as were laid off. The “Great Resignation” that began prior to the 2020 recession is still very much in effect.

Keep in mind that reduced hiring and increased layoffs have been an explicit goal of the Federal Reserve’ rate hiking strategy from the outset.

With quits continuing to be the dominant form of job separation, and with the magnitude of reported layoffs continuing to remain relatively low, a full year of Fed rate hikes has simply not had the chilling effect on labor the Fed has sought.

Moreover, while the pace of hiring has declined throughout 2022—the effect the Fed has wanted to see—the pace of separations has declined even more.

That separations have slowed faster than hiring has resulted in a net effect which is the polar opposite of the Fed’s explicit goal of reducing employment.

It is worth noting that, during the 2007-2009 recession, the slowdown in hiring significantly outpaced the slowdown in separations.

During that recession, quits declined, while layoffs rose and became the dominant form of job separation.

Throughout the execution of their rate hike strategy, the Fed’s explicit desire to see a reduction in employment has always translated in effect to wanting to see these labor conditions of the 2007-2009 recession repeated.

However, despite the economy having been mired in a recession for quite some time, the Federal Reserve has completely failed to replicate the labor conditions of 2007-2009.

Arguably, it has been this failure that has misled the Federal Reserve to mischaracterize labor markets in the US as “tight”, when the reality is they are quite toxic.

No metric demonstrates this toxicity more dramatically than the count of people not in the labor force. After spiking during the 2020 recession, with millions of workers literally forced out of their jobs and out of the labor force, only a partial recovery has ever really happened, with most of that happening in the three months following the April, 2020, end of the recession.

To illustrate the minimal change within this particular labor demographic, if we index the number of people not in the labor force to July, 2020—at the end of that 3-month recovery period—we see that the overall decline of workers not in the labor force from then until now has been a paltry 0.4%.

Nearly three years after the 2020 recession, almost 5 million more workers remain outside the labor force than immediately prior to the recession.

The failure of employers to pull those 5 million workers back into the labor force skews the proper apprehension of labor statistics. Because the Fed (and the rest of the economic illiterates in the government) ignores this awkward labor force metric, the minimal changes that have been seen in the labor force itself are mistakenly interpreted as signs of a tight labor market, one which must be “cooled” in order for inflation to come down.

The strategy has failed for the simple reason that the labor markets were never “tight” in the first place.

Had those ~5 million displaced workers been pulled back into the labor force, not only would their addition force a resolution to the artificially high job openings numbers, a labor force expanded by those 5 million displaced workers would almost certainly show greater pliability, and thus the increased unemployment metrics the Federal Reserve has been hoping to achieve likely would have been achieved more than a few rate hikes ago.

Without those displaced workers, the labor force simply is not behaving the way the Federal Reserve expects, leaving the Fed perpetually confused by the lack of impact its rate hike strategy has had on employment.

Since the very first hike in the federal funds rate in March, 2022, the Fed has wanted to see a major disruption in the labor force. In particular, the Fed wanted to see a dramatic upturn in unemployment. It hasn’t gotten it, and the February JOLTS data only confirms that it is not likely to get that any time soon.