Backing Into Stagflation

May PCE Report Adds To The Evidence The Fed's Policies Aren't Working

The May Personal Consumption and Outlays Report is for the most part a rehash of the April report—and highlights the same takeaway: the Federal Reserve’s policies for fighting inflation are not working now, have never worked, and are not likely to work in the future.

From the preceding month, the personal consumption expenditures (PCE) price index for May increased 0.1 percent. Food prices increased 0.1 percent and energy prices decreased 3.9 percent. Excluding food and energy, the PCE price index increased 0.3 percent. For a comparison of PCE prices to BLS consumer price indexes, refer to NIPA Table 9.1U. Reconciliation of Percent Change in the CPI with Percent Change in the PCE Price Index.

From the same month one year ago, the PCE price index for May increased 3.8 percent. Prices for goods increased 1.1 percent and prices for services increased 5.3 percent. Food prices increased 5.8 percent and energy prices decreased 13.4 percent. Excluding food and energy, the PCE price index increased 4.6 percent from one year ago.

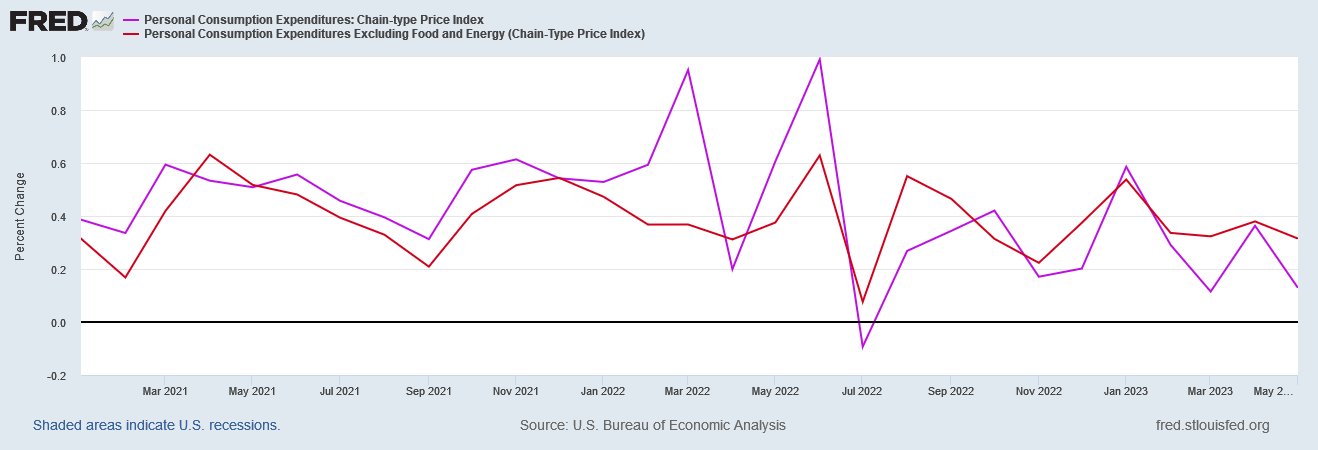

While headline inflation via the PCE Price Index dropping to 3.8% is a good thing, it is about the only good thing in the report, along with the 13.4% energy price decline. That “core” inflation has scarcely moved since before the beginning of the year, hovering between 4.6% and 4.7% , is a very bad thing.

The lack of progress on core inflation, remember, is the strongest proof there is the the Federal Reserve’s rate hike strategy on inflation is not working. In order for any strategy to make progress against inflation one must see progress against inflation. We don’t.

That the Fed has failed utterly on inflation has not stopped Dementia Joe from taking his usual undeserved Twitter victory lap, proving once again that his handlers have no grasp of economics.

For its part, the corporate media did its level best to put lipstick on the pig.

Household spending, meanwhile, rose at a more modest pace after surging in April. If fewer dollars are chasing after purchases, that could remove more pressure on inflation.

However, even corporate media does not believe the Fed is going to view these numbers that way, as the expectation remains that there will be a rate hike in July.

"Overall, there is little here to stop the Fed from hiking rates again at the late-July (Fed) meeting," says economist Andrew Hunter of Capital Economics. "But, with consumption growth and core inflation losing momentum, we still think that hike will prove to be the last."

Wall Street seems to concur, with the probability of a 25bps hike next month dropping only slightly, while remaining still elevated.

That the Fed’s rate hikes have not helped inflation thus far never enters into the equation.

To appreciate the totality of the Fed’s failure on inflation, one must understand that core inflation has been largely stable in the same general range since the fall of 2021—a full six months before the Fed began pushing up the federal funds rate.

Even headline inflation per the PCE Price Index had largely peaked by the time the Fed began raising the federal funds rate (blue vertical line on the chart).

The impotence of the Fed rate hike strategy against core inflation per the PCE Price Index is simply a confirmation of what core inflation per the Consumer Price Index shows—no impact, no mitigation of core inflation as a result of the rate hikes.

It is not possible to argue impact on inflation when there is no discernible impact on inflation—and trend lines which go horizontally mean there is no discernible impact. By either inflation gauge, core inflation had peaked by the time the Fed decided to take action, and where it peaked is where it has for the most part remained.

When we look at core inflation compared to food and energy price inflation, we quickly see that all of the progress made on consumer price inflation as shown by the headline metric can be attributed to the recent energy price deflation as well as a significant moderation in food prices.

This is yet more affirmation of the Fed’s failure, as the Fed prefers to focus its inflation thoughts on core inflation as measured by the PCE Price Index Less Food And Energy, as it is far less volatile, and far less influenced by random exogenous events.

Even when viewed month by month, core inflation per the PCE Price Index has only managed to move sideways since the beginning of 2021.

Simply put, the only places where inflation has improved is in the areas the Fed claims little influence and no credit whatsoever.

Moreover, while inflation on goods has all but disappeared at this point, inflation on services has been steadily rising since before inflation was even admitted to be a problem until February of this year. Through each and every federal funds rate hike, services inflation has been getting steadily worse until that time.

Within goods inflation, the influence of the Fed has been problematic, as inflation for durable goods peaked just before the Fed began raising rates. The inflation rate for non-durable goods peaked a few months after the Fed began raising rates.

While price inflation for goods has largely disapeaared, it is a stretch to give the Fed much if any credit for the decline.

We see even more evidence of the failure of the Fed to have any influence on inflation or its consequences when we look at personal consumption expenditures. While expenditures have reason in nominal terms since the end of the government-ordered 2020 recession, in real terms they effectively plateaued in March of 2021, with minimal increase after that time.

In other words, the Fed’s rate hike strategy has not impacted consumer spending in real terms at all, as it had reached an equilibrium a full year before the Fed began raising rates.

If we index expenditures to March, 2021, we see that since that time expenditures have risen some 16.9% in nominal terms, but have only risen 4.6% in real terms.

Bear in mind that constraining personal expenditures—what the Fed calls “revenge spending”—has been a specific policy objective of the Federal Reserve all along.

Even by its own criteria, therefore, their strategy has failed. For the strategy to have succeeded personal expenditures would need to have come down in real terms, and they have not done so.

When we look at the breakdown of income and outlays overall, we again see a distinct lack of Federal Reserve influence.

While personal income and personal expenditures have broadly risen since April of 2020, personal savings has actually declined.

Disturbingly for the Treasury, personal tax payments have also declined, especially since the beginning of the year.

Disturbingly for consumers, when we index personal income and expenditures data to April of 2020, we see that personal tax payments for a time were the fastest growing personal outlay category.

In order for inflation to come down, money velocity has to come down, and that means that spending has to decrease. As long as consumer spending remains more or less the same, core inflation willl remain more or less the same—just as it has done.

Despite the best efforts of the media to portray the PCE report as showing “cooling” inflation, the reality is that it shows no change at all on the core inflation which the Fed watches most closely. After fifteen months of rate hikes, with another rate hike seemingly all but certain next month, and the Fed has made no progress on core inflation.

The Fed has not stopped consumer spending.

The Fed has not incented consumer saving.

The Fed has not impacted core prices.

The Fed has not stopped consumer price inflation.

Meanwhile, there are still few reliable indicators of healthy economic growth.

What signs we do have are marginal upticks that need to go a lot farther before they show any meaningful change in the economy’s trajectory.

With economic stagnation on the one side, and continued inflation on the other, the overall takeaway from the May PCE report is a continued slide into a stagflationary recession, possibly heading towards a “lost decade” of lengthy economic weakness.

That’s what the Fed has to show for fifteen months of its failed inflation strategy: stagflation, recession, and lasting economic weakness.

It's almost like the FERAL Reserve is NOT nearly as omnipotent, omniscient, or omnibenevolent as they think they are.

Well at least the Supreme Court put a stop to the student bailout. I didn't "qualify" for any loans, giveaways, or anything being from a poor white family who lost its source of income in 1972, although I did exempt the first year of math with a couple a simple exams. This was in 1974.

I put the entire college experience down to them not raising rates (much) until I was about to graduate, and the two jobs I held during all but the last semester (not possible).

Spend Y, collect X, and print the rest, Z, right.

Z can be any number, greater than X, even.

Unless you want inflation to come down.

They don't.