Real Estate Crisis, Banking Crisis...Political Crisis?

Is China's Bursting Property Bubble Triggering Wider Social Unrest?

China’s bursting property bubble is giving the world a master class on what “contagion” effects really are. What began as one firm—Evergrande—facing liquidity issues and ultimately bankruptcy has steadily progressed to involve more firms, then more debtor classes, and now is encompassing an ever wider portion of the economy—as Evergrande suppliers are joining homeowners in refusing to service their loans.

Some suppliers to China Evergrande Group 3333.HK said they will stop repaying bank loans to protest against non-payment from the distressed property giant, joining homebuyers threatening to stop mortgage obligations for unfinished homes.

A growing number of homebuyers across China have threatened to stop making mortgage payments for stalled or unfinished property projects, aggravating a real estate crisis that has already hit the economy.

With each successive expansion of the crisis, China’s banks have come under increasing stress. At the same time, the crisis in real estate is colliding head-on with a rural banking scandal in Henan province, where some $6 billion worth of bank deposits have gone missing—and the depositors want their money back.

This confluence of crises may even be developing more ominous political overtones, as India media outlets have reported on a series of videos gleaned from social media purporting to show the deployment of tanks and military assets to suppress further protests in Henan (Note: while the videos are being carried by India media outlets their origin on social media means there is almost no provenance to substantiate the claims made regarding what they show). While the accuracy of the videos cannot be reliably determined at this time, their appearance across a spectrum of India media outlets so soon after the June BRICS summit, wherein India and China, along with Brazil, Russia, and South Africa met to foster further economic cooperation and development, is hardly helpful to China’s international political ambitions—and if the videos are genuine, portend a coming crackdown on bank protests reminiscent of the 1989 Tienanmen Square Massacre.

It Helps To Know The History

To understand the events currently unfolding in the Middle Kingdom, I encourage readers to review some of my prior articles on this topic:

Through these articles (and a few others), I have attempted to chart the evolution and trajectory of the current situation unfolding within China’s real estate and banking sectors, and shed some light on what imperils the world’s second largest national economy (and, in Chinese real estate, the world’s largest asset class). As with most economic crises, the seminal events are generally little more than catalysts and signposts to the chaos, with the actual formation of the crisis having occurred more silently over a span of years. China’s twin crises did not emerge in a day, and they will not fade in a day, nor even a week, a month, or a year.

The latest turn of events has been the expansion of the “debt boycott” to include several Evergrande suppliers, who are refusing to pay on their outstanding loans as Evergrande has not yet paid them. An informal—and thus highly disruptive—”debt jubilee” is being declared by China’s debtor class.

Suppliers Pick Up On The Boycott Theme

As Evergrande defaults on billions in offshore debt (and quite possibly onshore debt as well), it has also failed to pay many of its suppliers, some of whom are now asserting their own financial hardships and refusing to make further payments on outstanding loans as a protest against the ongoing Evergrande default and bankruptcy.

Two suppliers confirmed to Reuters an online letter written by Evergrande's small suppliers in central China's Hubei province, dated July 15, in which they said they have to stop loan repayments because the developer owed them money, leading to debt problems of their own.

In the letter addressed to Hubei local authorities and banks, the suppliers said 6 billion yuan ($889 million) of funds in an escrow account had been misused by Evergrande, resulting in stalled projects and missed payments to them. They were being used as "financing tools" of the developers, they added.

The number of Evergrande suppliers now refusing to make payments on their own outstanding debt is unclear, although given the rapid expansion of the mortgage boycott, it is quite possible the supplier debt boycott is expanding as well. As of this writing, the mortgage boycotts involve at least 301 housing projects located in 91 cities.

If the supplier debt boycott does expand, an entirely new dimension of “moral hazard” for any developer bailout emerges: giving a lifeline of fresh loans and other forms of credit to over-leveraged developers without addressing the needs of other debtor classes such as suppliers and contractors to whom developers such as Evergrande owe literally billions of yuan is almost certain to be seen as rewarding the companies seen as the cause of the entire crisis.

The development underscores a dilemma for Xi Jinping’s government as it grapples with who to bail out as the country’s property crisis deepens: Relief for some borrowers could prompt threats of non-payment by a whole host of others. While bending to demands for support could put a strain on state finances, ignoring them might lead to a spiral of defaults as more and more borrowers refuse to meet their obligations.

In order to placate suppliers, Evergrande and other developers must make good on their outstanding debts. In order to placate homeowners, stalled housing projects must be completed. In order to accomplish either objective, developers will need new loans and fresh credit lines, thereby allowing them to escape insolvency—a beneficence not available to either suppliers or homeowners.

If Beijing does not act, then not only are one-fifth of China’s developers likely to go bankrupt—thus jeopardizing trillions of yuan in onshore debt—but at least 2 trillion yuan worth of outstanding mortgages could ultimately default from the mortgage boycott, with an unknown number of billions (trillions?) of yuan in supplier debt. Thus has the real estate crisis become a banking crisis.

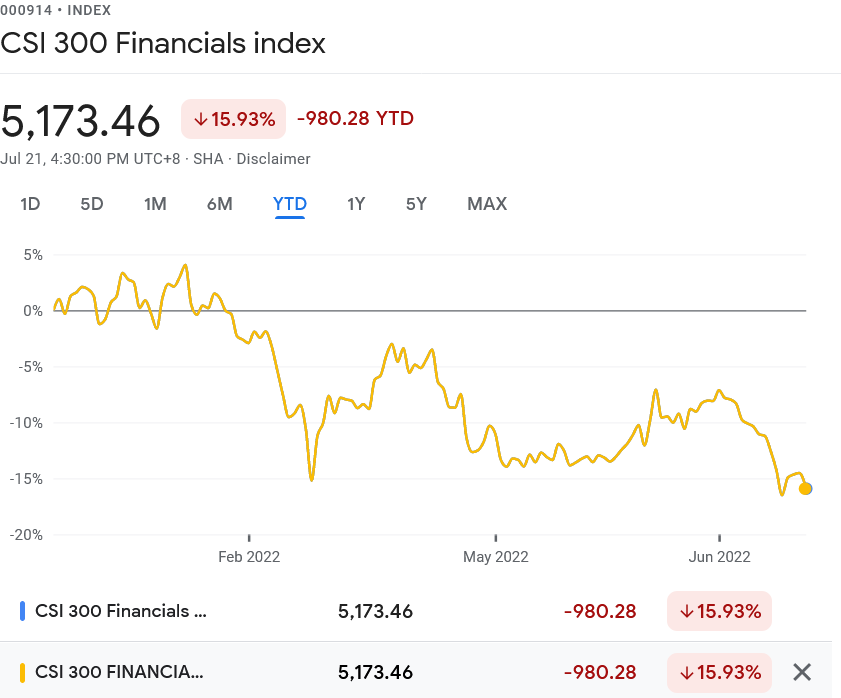

Bank Stocks Have Been Losing Value

While China’s banking sector has not (yet) reached a point of systemic calamity or collapse, there is no denying that China’s banks have had a rough year thus far. Real estate developer woes, combined with the disruptions and dislocations of the Zero COVID lockdowns (which may be returning once more), have pushed the CSI 300 Financials Index—a leading stock index tracking the performance of China’s banks—down more than 15% on the year.

Declining share price is a particular problem for banks, as it increases the amount of stock that must be issued in order to ensure sufficient bank capital is on hand to guard against loan losses.

Moreover, the sector has not been overly impressed with the policy steps announced by Beijing over the past week. Despite initial buoyant responses to Beijing’s efforts to shore up the real estate sector and resolve the mortgage boycott issue, bank stocks are still down for the week an additional 0.75% at least.

Investor sentiment is telling the hard truths that both the banks and the banking regulators do not wish to say out loud: the collapse in real estate is causing banks significant pain, and it will continue to get worse for some time to come.

Officially, the amount of mortgages at risk remains small. As noted in a Fitch Ratings report on the boycott, at Fitch-rated Chinese banks, the amount of mortgages impacted by the boycott is less than 0.01% of the overall total.

We do not believe the defaults will directly affect Fitch-rated Chinese banks, with most disclosing that affected mortgage loans amount to less than 0.01% of their outstanding residential mortgage loans. However, should defaults escalate, there could be broad and serious economic and social implications.

However, this number is at best wildly optimistic, and other estimates are far more grim.

Chinese banks say the risks from the housing loan nonpayments are controllable. So far, they have disclosed only 2.1 billion yuan ($311 million) of credit at risk. Still, GF Securities Co. expects that as much as 2 trillion yuan of mortgages could be impacted by the boycott.

Overall, Chinese banks sit on 38 trillion yuan of outstanding residential mortgages and 13 trillion yuan of loans to the country’s beleaguered developers.

2 trillion out of 38 trillion equates to ~5% of outstanding mortgages potentially impaired by the boycott—a number which is likely to grow should the boycott continue to spread. With a large and as yet indeterminate percentage the 13 trillion yuan of developer loans at risk, in addition to the potential for non-performing loans among the developers’ suppliers, China’s banks are facing enormous default stresses, far larger than has been officially acknowledged—a fact investors realize all too well.

Moreover, the Fitch analysis has already been overtaken by Beijing’s efforts to prop up the developers. While Fitch quite rationally extrapolated tightening escrow requirements and oversight in response to the boycott, Beijing has already begun pressuring local authorities to ease developer access to escrow funds, in order to get stalled projects restarted. As noted above, in order to fully placate homeowners the housing projects must be completed—most if not all other considerations are secondary.

Bank Runs: The Depositor’s Vote Of No Confidence

The twin crises of developer liquidity plus mortgage and supplier debt boycotts continue to shine spotlights on the festering Henan “village bank” scandal, where an apparent scam has resulted in some 40 billion yuan in “missing” bank deposits.

Henan’s provincial capital Zhengzhou is ground zero in the mess, where a banking scam by local fraudsters has combined with a mortgage boycott by disgruntled homebuyers. The scam has run up a tally of 40 billion yuan (US$6 billion) in missing bank deposits and a rare protest by nearly 1,000 depositors. Henan, the home province of China Evergrande Group’s founder Xu Jiayin, also had more unfinished residential projects than anywhere else in China, according to mainland Chinese media.

In an effort to placate depositors and shore up confidence in the “village banks” that comprise nearly 30% all Chinese banks, local regulators are starting to return depositor funds to them, with a second round of depositor refunds having been just announced.

In their bid to shore up confidence among depositors, Henan and Anhui provinces started making repayments to smaller depositors on July 15, following investigations by authorities and arrests of suspects.

On Thursday, financial authorities in Henan said they would commence the second round of repayments to clients on behalf of the four rural banks there from July 25.

Beijing has few good alternatives, as ignoring the protests would only encourage further unrest as well as runs at other local banks, not only in Henan but across China. Simply telling depositors to “be patient” is on its own wholly inadequate to the situation. The protests mean depositors are out of patience.,

Deposits are the lifeblood of all banking activity—no deposits means no loans, no financing activities, and, ultimately, no bank. The bank runs cum protests in Henan are the ultimate depositor vote of no confidence.

A collapse of confidence in China’s small regional and local banks would be a systemic crisis even if the larger banks were not initially affected. It is this looming threat which many analysts are overlooking in their optimistic projections of a “soft landing” for the banking sector.

The obstacles aren’t insurmountable. [Tianlei] Huang says the property crisis will impact banking profits, but he doesn’t expect a system-wide calamity. He points out that down payment requirements in China are high—typically 30% for first time buyers—which means that people are unlikely to walk away from mortgages unless property prices see a seriously sharp decline.

This assessment ignores the reality of unfinished housing projects. If the homes are not delivered, the mortgages are effectively walking away from the people, as the end result is the same total loss of the investment. Falling property prices only bring forward the inflection point where homeowners throw in the proverbial towel and join the boycott.

Tanks In The Streets?

The bank runs and protests in Henan, coupled with the spreading mortgage and supplier debt boycotts, are unquestionably becoming a threat to social stability in China. There is little doubt that Beijing sees this threat, which is why it is proving unusually accommodative to protesters, allowing for grace periods and promising refunds of deposits.

Which makes the reported appearance of tanks on the streets of Chinese cities all the more disturbing—and yet that is exactly what is showing up on several media outlets in India.

The Financial Express had this to say:

Visuals of tanks on the streets of Chinese provinces in the midst of a worsening banking crisis have led to alarms from Beijing-watchers on the Internet. The numbers already show a bleak scenario. Latest GDP data reveals China’s slowest economic growth since early 2020. Several clips of tanks being deployed outside banks in Henan province have brought back memories of the brutal crackdown of 1989 – The Tiananmen Square Tragedy – for many. While Beijing is silent on the tanks, some media reports claim that the local administration has asked depositors to ‘remain patient’.

India Today led with the conclusion that this was explicit effort to suppress further protests against the banks.

Army tanks rolled on the streets of China’s Henan province to deter protesters who have been demanding the release of their savings after banks put a freeze on withdrawals.

NDTV had this to say:

A video showing tanks lined up on a road in China has shocked the internet. Quoting local media outlets, users on Reddit say that the footage is from Rizhao, in Shandong Province and the tanks have been deployed to protect the local branch of a bank at the heart of a scandal.

Independent journalist Jennifer Zeng, whose “Inconvenient Truths” videos highlight the darker truths of CCP-controlled China, also shared the videos on Twitter:

The videos themselves first appeared on Reddit (links here and here), and subsequently went viral, even showing up on YouTube.

New Zealand native Andy Boreham, affiliated with the Shanghai Daily, went on Twitter to claim the videos showed a “standard training exercise”.

Newsweek, however, has reported on the videos without either confirming or rejecting the “training exercise” explanation.

While the actual purpose for the tanks on the streets is far from clear, the video clips do raise a few questions:

Why are the tanks even on the streets? Tanks and similar tracked vehicles are notoriously unfriendly to pavement, and are generally transported rather than driven through cities and on highways. “Training exercises” are generally not carried out among the civilian population.

Why are they there at night? Parades and other benign exhibits of military hardware generally take place during the day.

Why are the tanks just sitting there? The claim that they are thwarting an obviously agitated crowd seeking only to gain access to their deposits is hardly supported by the videos. The crowds are peaceful, with no chants, placards, banners, or other outward signs of a protest gathering.

While few if any media outlets anywhere in the world have an unblemished reputation for journalistic accuracy, the India outlets themselves largely span the political spectrum within India: The Financial Express is rated as “right-center” by “media bias resource” Media Bias Fact Check. India Today is similarly tagged as “right-center”. NDTV is considered “left-center”. All three outlets are considered to have “medium credibility” with a “mixed” grade on factual reporting.

How reliable the factual reporting and credibility assessments are is problematic, given that MBFC also gives the New York Times high marks for both credibility and factual reporting. Still, that the putative bias of these outlets tilts in both directions cuts against the idea of the videos being the stuff of mere “conspiracy theory.” While tabloid sensationalism cannot be ruled out, neither can the existence of what the videos purport to show: tanks on the streets of a Chinese city, apparently in the aftermath of a large gathering (a protest?). While some comments on the social media sources for these videos have attempted to debunk them by ascribing the tanks’ appearance to “PLA Day” activities, PLA Day is celebrated on August 1, ten days from now.

Nor should India’s fractious history with China be overlooked. While India and China do engage economically and politically through the BRICS summits, they have also had a few conflicts over the years, the most recent being a border clash in the Galwan Valley, with fatalities on both sides.

Also, despite media aggregator sites such as MSN and Yahoo! News carrying reports of these videos, none of the major “fact checking” sites are attempting to debunk them.

Does this mean the videos authentically show efforts by Beijing to quell bank protests by force? Not necessarily. The videos show tanks in the streets of a Chinese city, for reasons not fully known. Given the appalling history of the Tienanmen Massacre, such images coming from China are inherently disturbing. Beyond that, the videos are a source of questions, not answers.

What the reporting by Indian media outlets does indicate is a growing narrative of social unrest within China. Given China’s myriad economic woes, and the recent dystopian disaster of the Shanghai “Zero COVID” lockdown, it is a narrative that arguably lends political rationale to Beijing’s seeming willingness to accommodate the mortgage protests while working to make depositors from the failed Henan banks whole.

That narrative, coupled with the new wrinkle of the Evergrande supplier debt boycotts, strongly suggests the pace of China’s real estate collapse and accompanying banking crisis is increasing. Events appear to be accelerating, placing an increasing challenge on Beijing to keep up.

Beijing has already lost control over its real estate sector. If current trends continue it may lose control over a good deal more—both economically and politically.

Been wondering how the recent sale (for how much?) of oil to China plays into this

". . . giving a lifeline of fresh loans and other forms of credit to over-leveraged developers without addressing the needs of other debtor classes such as suppliers and contractors to whom developers such as Evergrande owe literally billions of yuan is almost certain to be seen as rewarding the companies seen as the cause of the entire crisis."

Indeed. It is reasonable to expect that the contagion will grow.

One way of looking at this is that each population - from band, to village, city, to fraction of a continent and to entire continent - in order to function reasonably peacefully and productively, have a spot on which a thing called a "government" grows. The deal is that this thing, which is not productive in itself, returns to the host which it parasitises significant benefits which cannot be attained by any other arrangement (other than joining a larger population with its own government-thing growing on it). The benefits include a coordinated defense of the land and possibly means of forcibly acquiring further land, resources and influence over other populations. The government thing is also well placed to regularise behaviour in the population by way of laws and their enforcement. The government explicitly taxes and may to some extent (subject to numerous corrupting influences from the government itself, political parties and wealthy individuals and companies) subject itself to selection by a democratic process.

Except in the cases where the government uses a currency it does not control (all sub-national governments, and those national governments which use the Euro or some larger country's currency) the government thing also has the power to create currency without being subject to anti-counterfeiting laws and punishments.

In the past there were efforts to run countries with actual money - tokens which have intrinsic value, such as due to being made of gold or silver. Then paper money was used for convenience and divisibility - backed up 100% by gold of equivalent value for each issued note or coin, held by the government thing. (I recall this was the case for the USA in the early 20th century.) Then the 100% was diluted to 25%. Then the holding went to zero, but the government would swap an ounce of gold for USD$32, with the USD$ being a stable reserve currency and the Bretton-Woods agreement ingeniously pegging many other currencies to it by a relatively stable system of occasionally adjusted country-currency specific exchange rates with the USD$. President Nixon ended this (I recall) because the Europeans were taking advantage of this gold window by buying gold there, and because he wanted to create more currency (not money) to fund the military-industrial complex which benefited him and his campaign financially, by expanding the Vietnam War.

Since then, there has been no over-arching mechanism to reduce the temptation of each currency's government thing to create more of it. By doing so, the government thing and those it serves can cause its citizens and the citizens of other countries to do useful work for them, without providing anything in return but freshly - and cheaply - generated currency.

My eyes glaze over past a certain point with finance, debt, complex investment vehicles etc. I don't fully understand what all this "debt" really means. The concept is all tangled up in flows of currency (paper notes and coins, or its electronic equivalent) and people's belief about the real value of the currency they hold, or are promised by owning an investment instrument. This is hard to relate to actual flows of genuinely valuable goods and services.

Everyone and his dog is in debt. The complexity of industrial production, especially electronics - with components coming from many countries and companies (sometimes just a single source, no other company produces the component) - means that the world is extraordinarily dependent on webs of commerce no-one really understands, which must work reliably almost all the time. So there is great potential for whole industries grinding to a halt, or at least slowing down significantly, due to the supply chains being unable to provide every needed component in time. This happened with motor vehicles, largely due to the pandemic driving the demand for laptops etc. sucking semiconductor production from the devices needed for cars. (I wonder if current leading-edge CPUs will never be bettered. The transistors get smaller and so more subject to degradation over time by molecular diffusion. I am less inclined to discard my older machines . . . )

What else is the CCP to do but crank out more currency to prop up these banks - so diluting the value of everyone's currency holdings? This cannot end well. The same is true of most countries, where the government thing has been cranking out currency to satisfy their own needs, the short-term desires of the population, and the needs of those who corruptly bounce it back to support those currently running the government thing, while dooming the whole population to ruinous inflation, instability, crisis and loss of productivity and security.

The enormous burden of debt (whatever it is) means there must be a reckoning, since at best only a small fraction of it can be repaid by genuine productive effort. This means those holding the debt (such as pension funds and the individuals who are expecting to receive said pensions) - who currently think of it as an investment asset - will be left with little or nothing.

This looming disastrous failing, and the present day disastrous failings such as the US "healthcare" system, and almost every government's (Uttar Pradesh and a few others excepted) disastrous failure to respond properly to COVID-19, shows that in the ongoing battle between populations and the government thing parasites which grow on them, the parasitic elements of the government and those outside it who profit from its corrupt behaviour, are winning.

This millennia-old battle is accompanied by an arms race. The invention of print and broadcast media and now Internet based mass media and social media - and websites in general - have been powerful new weapons which could, in principle be used to support efforts to protect the population from corrupt, parasitic, government actions, or to convince many in the population that these actions are to their benefit.

The uncensored and potentially high signal-to-noise ratio of this and other Substacks is a win for the population, but too few have the time, inclination or discerning intellect to make good use of these and other such positive developments. Much more common is the ability of the fear and anger driven social/mass media to distract and mislead the majority. The Bad Cat (apologies for the capitalisation) has a great essay on this: "generating a sense of crisis so people will demand 'solutions' is not a basis for government": el gato malo 2022-07-17 https://boriquagato.substack.com/p/generating-a-sense-of-crisis-so-people .

This can be boiled down into the observation that the population, collectively, lacks the intellect and inclination to rein in the parasitic tendencies of their government things. Part of this is that limited quality of people who seek to run these government things. A few, such as Paul Keating and Malcolm Turnbull here in .au looked like they had what it takes. But they did not last long. Imagine a world where governments were frequently run by people as bright, communicative and highly principled as

Kemi Badenoch!

I am inclined to believe the benign explanation for the Chinese tank video - but why indeed are they wearing out their engines, transmission, tracks and the road itself when they are normally transported on low-loader trucks or by rail? Maybe it is a show of force. The fact that many in the Twittersphere and MSM are panting breathlessly about the tanks being in Henan is strong support for el gato malo's hypothesis.