Where Does The BLS Jobs Report Leave The Fed's Rate Hikes?

Will Jay Powell Drive the Narrative Or Continue To Be Driven By It?

As one of my readers pointed out, calling “BS” on the July Employment Situation Report by the Bureau of Labor Statistics was a fairly easy call. The numbers are so contradictory and so incoherent as to make rational defense of them all but impossible.

However, there is one entity that is without a doubt not going to challenge the jobs numbers openly: The Federal Reserve.

Regardless of what the individual Federal Reserve Bank Presidents might think of the Employment Situation Report, regardless of what Fed Chairman Jay Powell might think, the Fed overall has little choice but to take government statistics at face value. From their perspective, the Employment Situation Report is the reality of employment in the United States.

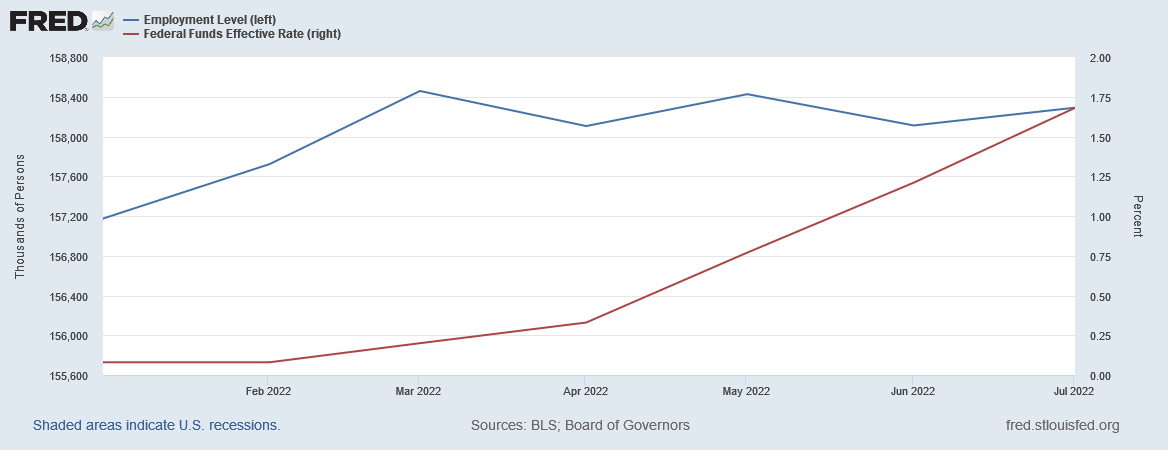

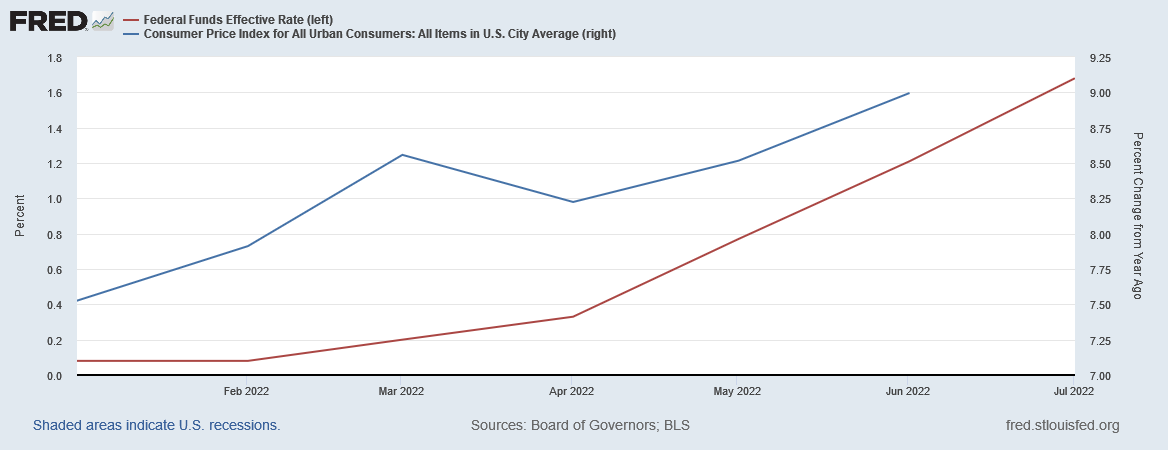

How does the Federal Reserve respond to half a million jobs nominally being created in July, when its goal for the interest rate hikes is to cool down employment, as well as engineering a bit of demand destruction to bring down inflation? By its own metrics for success—lower employment and lower consumer prices—pursuing a tighter monetary policy through a succession of hikes in the Federal Funds Rate1 is so far not working: inflation rose again in June and may very well do so for July as well.

Does this compel the Fed to pursue even larger rate hikes? Will the Fed try to “jawbone” interest rates still higher between now and the September meeting of the Federal Open Market Committee—the rate-setting body within the Federal Reserve?

Wall Street Uncertain

Wall Street remains ever hopeful that the Fed will lose its collective nerve and back off any more interest rate hikes. Interest rates tend to push stock prices lower—Jay Powell’s last effort at raising interest rates in this country, right before the COVID pandemic, briefly triggered a bear market before he relented in 2019. Asset price inflation is the sort of inflation Wall Street dearly loves, and it flourishes when interest rates are low.

Consequently, the stock market indices had a mixed reaction to the BLS jobs report, with the Dow and the Russell 2000 Index slightly up on the day, while the S&P 500 and the Nasdaq finished the day in the red.

Treasury yields jumped immediately on the jobs report release, as the 1 Year, 2 Year, 5 Year, and 10 Year Treasury Bonds all opened 20bps higher than yesterday’s close.

Despite the jump, the 10 Year Treasury remains stubbornly inverted against the 2 Year Treasury, with the inversion2 gap between their yields increasing on the day. Yields have been inverted across the entire lower end of the yield curve, and the jobs report did nothing to change that.

Wall Street’s immediate reaction to the jobs report has been to raise its expectation that come September the FOMC will issue another 75bps rate hike, rather than the 50bps hike that was projected as late as Thursday.

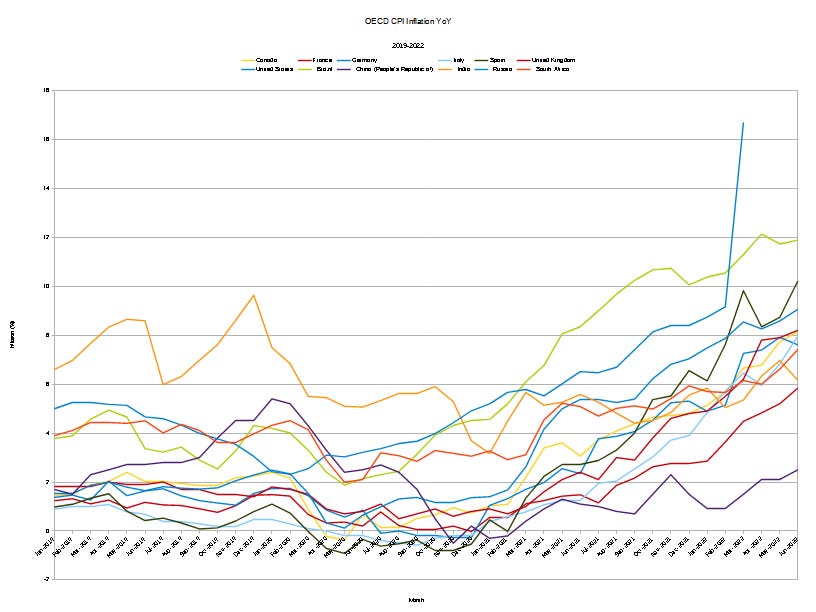

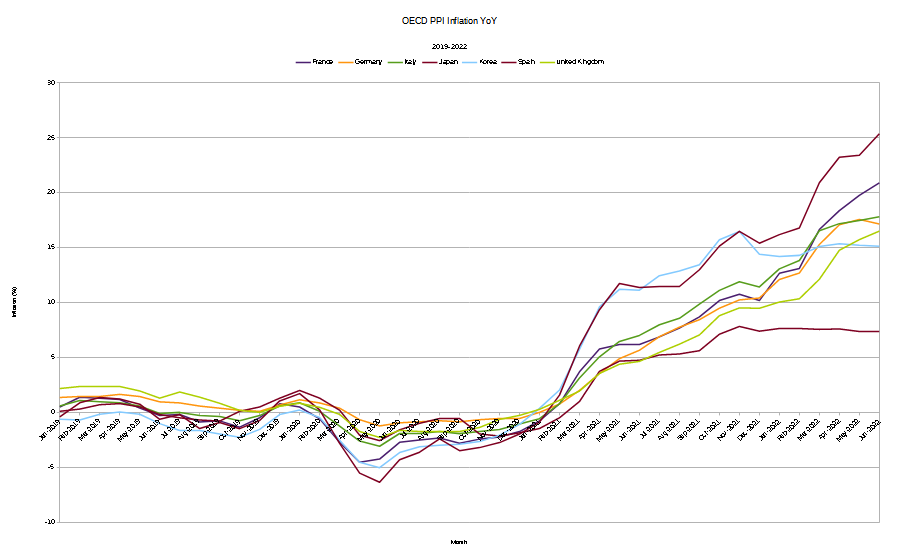

Inflation Remains A Global Issue

In one respect, the Federal Reserve has few options besides raising interest rates. Inflation is not merely an American issue, as virtually all the leading economies within the OECD have been grappling with rising inflation for most of 2022.

With producer price inflation (PPI) running higher than consumer price inflation globally, there is a strong probability peak inflation has not yet arrived.

The omnipresence of inflation around the globe is prompting not just the Federal Reserve but the European Central Bank and the Bank Of England to raise interest rates and yields significantly. Tighter monetary policy is very much in vogue among the world’s central bankers.

This global coordinated pursuit of tighter monetary policy puts significant pressure on the Federal Reserve to stay the course, if only to preserve the dollar’s relative strength against other currencies such as the euro, which is one of Jay Powell’s few successes.

Does The Fed Understand The BLS Employment Situation Report Is Broken?

While the global pressure for the Fed to continue tightening is significant, the jobs report not only pushes the Fed towards tighter policy (i.e., more rate hikes), but also towards larger rate hikes. Whereas before the expectation was that in September the FOMC would raise rates 50bps, now the expectation is 75bps.

The Fed is in no position to dispute the BLS’ jobs numbers. Still, it remains for the Fed and the FOMC to decide how large a rate hike is warranted, based upon the jobs numbers, among other data. The problem with this, of course, is that the BLS report is clearly and demonstrably broken; the Fed will be basing its policy response on faulty data and faulty assumptions.

If the Fed accepts the 528,000 jobs created number, instead of considering the far more relevant declining overall employment level charted by the BLS, it raises the risk of a serious policy error, and potentially tightening too far or too fast, so that the economy slips from what is shaping up to be a long and difficult recession to an even longer and even more difficult depression. While the decline has been marginal thus far, overall employment has proven more responsive to the Fed’s rate hikes than inflation has.

The potential for a serious policy error is increased when one considers that, in relative terms, Jay Powell has already been far more hawkish than Paul Volcker was during his early 1980s fight against inflation. Volcker merely doubled interest rates to get ahead of inflation; since rates were already near zero when Powell began tightening, he has already increased rates by a multiple of more than 20—many times what Volcker contemplated.

Is the relative rate of tightening more imperative than the absolute interest rate itself? During the remainder of 2022 we are likely to get an answer to that question, whether we wish it or not.

Jay Powell Is No Paul Volcker

One question, however, seems already to have been answered: No matter the rhetoric, Jay Powell is no Paul Volcker. While Volcker was, for better or worse, willing to set the tone for any discussion about monetary policy, rather than be led or influenced by events, Powell is constantly in reaction mode. Even when his rhetoric takes a hawkish turn, it is in response to Wall Street not taking his remarks seriously.

Nor is Powell exploring alternative strategies for tightening. He is not, for example, seriously pursuing a strategy to more rapidly shrink the Fed’s bloated balance sheet, which arguably would do more to tighten and shrink the overall money supply than interest rate hikes. Interest rates, job loss, and demand destruction appear to the sum total of his inflation-fighting toolbox—whether they work or not.

As the length of time between the stagflation faced by Paul Volcker and the stagflation Jay Powell faces now demonstrates, these circumstances are a once-in-a-generation event. As such, there are no sure rules, and barely even any guiding principles for what is the optimal strategy—and even if there were, the differences between the economy in Volcker’s day and today make any doctrinal adherence to Volcker’s ideas and strategy problematic in the extreme.

Volcker, through his sudden and extreme rate hikes, even at the expense of a recession, seemed to understand this, and accepted the call to craft his own strategy, without regard to what had been done in the past. Powell, however, has been unable to break out of the institutional mindset of the Fed, and thus reflexively views all price rises and inflation as something that require interest rate hikes to correct, without regard to the multiple externalities and policy-driven supply-chain disruptions driving much of the current inflation, externalities which will not be moderated by any amount of interest rate increase.

To be like Paul Volcker, Jay Powell has to find the courage and the creativity to change the narrative, and then to drive it. So far, he is being driven by the narrative, and while Wall Street financial markets may approve in the short term, the Main Street economy is not likely to be so generous in the long term.

The Federal Funds Rate is set by the Federal Open Market Committee and is used to benchmark and influence other interest rates within US financial markets, especially treasury yields and mortgage rates.

Inverted yields between short-term and long-term maturities are generally considered a recession leading indicator, as they indicate greater investor pessimism about the near term than the longer term.