OPEC Extends Production Cuts, Oil Prices Stay Put

Less Production At Same Price Level Equates To Less Demand

It must be mystifying to be an OPEC oil analyst—nothing OPEC does to boost oil prices ever gains much traction, and the most OPEC has been able to do is put a problematic floor under oil prices (for now). OPEC along with Russia have cut production repeatedly, yet oil prices have stubbornly refused to rise, hovering in the same price ranges where they have been for months.

Case in point: on the one hand, there are media reports that Russian oil production cuts are impacting India’s imports of Russian crude.

The production cuts announced by Russia in a bid to arrest the decline in international crude oil prices have started to impact its seaborne trade with India, which is expected to continue in the coming months.

Besides, the scenario could also lead to the world’s top two oil consumers — China and India — vying fiercely for the highly sought-after discounted barrels from Russia.

As per energy intelligence firm Vortexa, India’s crude oil imports from Russia fell by a steep 8 per cent M-o-M to 1.798 million barrels per day (mb/d) in June 2023 from a record 1.96 mb/d in May, which is being attributed to voluntary production cuts by the world’s second largest crude oil producer.

On the other hand, the prospect of China and India competing for increasingly limited Russian crude has not produced any reports of significant shifts in the price of Russian crude. Given that oil is ultimately just another commodity, where there is increased competition for the same resource there should be increased price to reflect that.

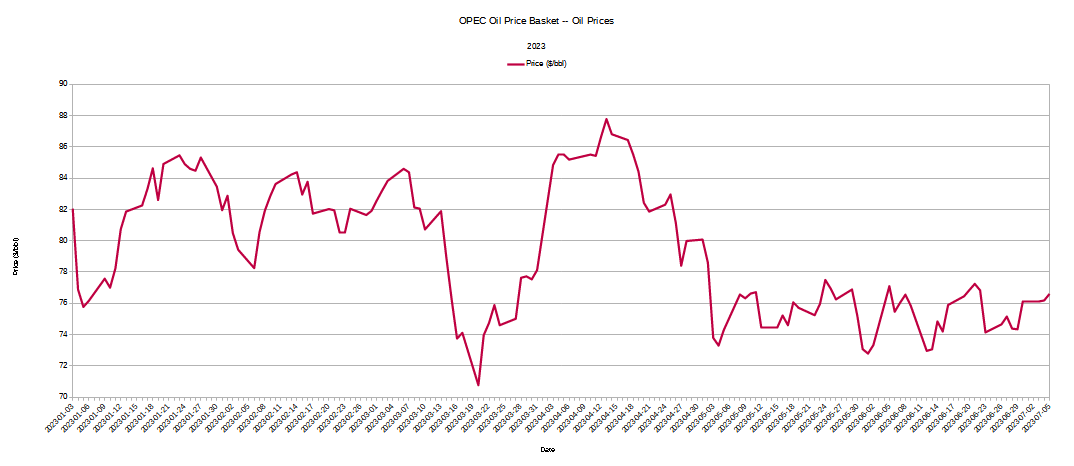

Nor is Russia’s situation unique. The OPEC nations have also announced production cuts to push up the price per barrel, only to have the gains either not materialize at all or fade very quickly, with the result that benchmark crude prices remain seemingly locked within a trading band, with Brent trading between $72/bbl and $78/bbl, and West Texas Intermediate trading $67/bbl and $74/bbl.

OPEC has succeeded in putting a floor price in place for crude, but has accomplished no more than that.

If we look at the oil price data for OPEC’s own OPEC Basket blend, the trading band for the past two months has been roughly the same as the Brent band—$72/bbl to $77/bbl.

Their announced oil production cuts in April succeeded in lifting the price briefly to just under $88/bbl, only to see the price fall back down to the trading band within a month.

OPEC prices, just like Brent and WTI prices, peaked in June of 2022, and have been on a steady downward trend ever since, achieving a problematic floor only within the past two months, after multiple production cuts.

As I have discussed previously, predictions of rising oil demand have simply not materialized, and despite multiple announced production cuts supply still seems to outpace demand.

Even OPEC oil ministers seem rather confused and confounded by the state of oil markets. As much as they, like so many others, tout China’s economic “recovery” and look to China for future oil demand growth, at the same time they are extending and deepening production cuts—an action indicative of declining demand, not growing demand.

OPEC last week underlined that Asia’s continued strong economic growth would account for virtually all the growth in demand for oil this year. Saudi Aramco added that China and India will drive oil demand growth of more than 2 million barrels per day (bpd) in the period. Just prior to these two comments, Saudi Arabia’s energy minister Prince Abdulaziz bin Salman said that OPEC and its allies are in “a state of readiness” amid a divergence between the physical and futures oil markets. These actions, he added, would be “precautionary […,] part and parcel of what we call being proactive and pre-emptive.” For oil trading insiders what these comments add up to is OPEC, and its de facto leader Saudi Arabia, setting the stage for further major ad hoc cuts in their oil production aimed at pushing oil prices much higher. The traders didn’t have to wait long. Saudi Arabia, on Monday morning, announced that it was extending its voluntary 1 million bpd production cut through August, sending oil prices rising by 1%.

One problem, of course, is that China’s economy is itself in decline, and its “recovery”after the end of Zero COVID has been somewhere between brief and nonexistent.

Even aspects of China’s own oil industry which would nominally point towards expanding supply and demand fail to translate into improved economic output at the end.

One reality that gets little attention is that China has been increasing its own crude oil production—China does not have a lot of oil, but it does have some, and what it has, it is pumping.

Unsurprisingly, this coincides with increased diesel and gasoline production from China’s oil refineries.

Yet it is worth noting that even though China has increased its diesel and gasoline production, neither is currently at peak production. Both diesel and gasoline production were in fact significantly higher under Zero COVID than since the ending of that policy.

But most crucially, increased oil production and refined products output has not translated into increased exports for China. The total value of both exports and imports has declined in recent months, significantly lower than peak levels achieved under Zero COVID.

Increased production is not being translated into either nominal or real economic benefit, a lack that is weighing heavily on world markets, dragging them down.

The lack of actual recovery in the Chinese economy is finally getting noticed and analysts are ratcheting down expectations accordingly, leaving the markets to price in less and less actual demand.

Data from China has sparked fears that the economic recovery from coronavirus lockdowns in the world's second-largest oil consumer is losing steam.

"The economic recovery in China following the lifting of coronavirus restrictions has been noticeably more sluggish than anticipated, even though the data for Chinese oil demand proved robust," Commerzbank analyst Carsten Fritsch said.

China’s economic deterioration is likely being amplified by rising interest rates, as central banks around the world attempt to grapple with rising and occasionally runaway consumer prices.

Higher interest rates eat into consumers' disposable income and could translate into less spending on driving and travelling, limiting oil demand.

They also drive up costs for manufacturers, and data suggests a slowdown in the sector is happening.

"There is no beating around the bush, factories are struggling across the globe as the sector shrank in Japan, the euro zone, the UK and the U.S. whilst slowed in China last month," PVM analyst Tamas Varga said.

Nor is China the only economy mired in recession at the moment. US manufacturing is also stuck in decline, providing another force to depress oil demand. Nor can we ignore the much deeper economic contraction in the European Union, where some countries such as Germany are sliding towards depression-like deflation.

Are such factors coming together to suppress global oil demand? There is certainly good reason to think so, particularly because US oil stocks have risen recently.

Rising oil stocks means falling oil demand.

There are other indicators of soft and declining demand for oil, such as the global oil markets relative non-reaction to the possibility that Libyan oil output could be disrupted altogether, as the feuding regimes seeking control over the country ratchet up their combative rhetoric over oil revenues in that fractured and war-torn country.

Fears have been raised of a damaging oil shutdown in Libya with implications for global energy markets after Libya’s strongman in the east, Gen Khalifa Haftar, warned of military action unless oil revenues are divided fairly within the next two months.

With the country long divided between two governments in the east and west and little prospect of presidential elections designed to reunify the country at least until next year, politicians in the east have threatened to put oil revenues under judicial control preventing the revenue reaching the Central Bank from the National Oil Corporation (NOC), the state-run oil firm.

It is difficult to consider the prospect of a shutdown of Libyan oil production as “damaging” when said prospect does not move oil prices even a little bit.

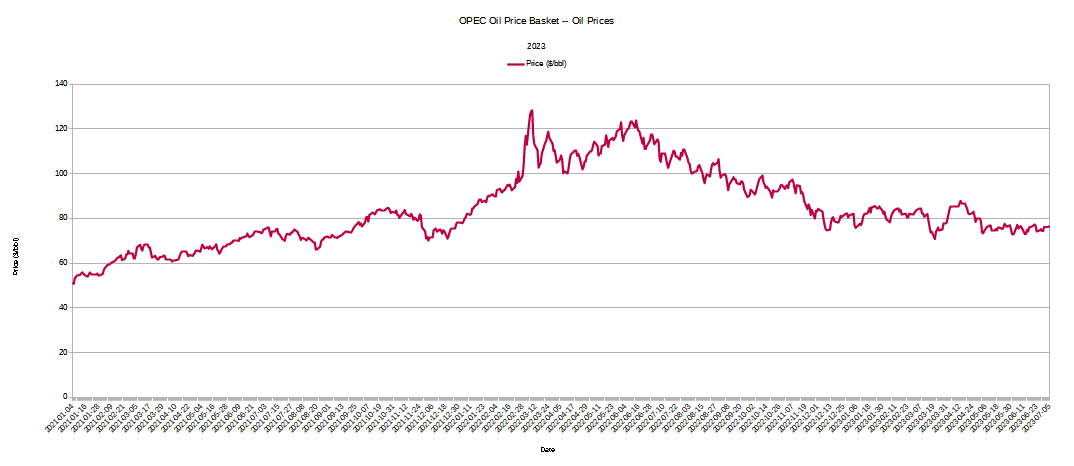

To appreciate the significance these disparate data points, let us look again at the oil price charts for Brent and West Texas Intermediate.

It is not merely that these benchmark oil prices are below where they were on the eve of Russia’s invasion of Ukraine. It is that the upper bound of their respective trading ranges is below where oil prices were on the eve of Russia’s invasion of Ukraine. When the entire trading band is taken into consideration oil prices are immediately seen as being even softer than the spot price itself might appear.

This is happening after China has ended Zero COVID and “reopened” its economy. This is happening three years after the United States locked down—three years after most of the world locked down in response to COVID.

This is happening with US manufacturing in a slump, with China in a slump overall, with Europe alternately in a slump and in a collapse. The only major economy not mired in stagflation and recession at the moment is India—yet even India has yet to see any significant increase in economic growth patterns, based on the relatively stable PMI trends in that country.

As the Manufacturing PMI chart shows, India’s manufacturing base has been fairly constant throughout the rise and fall of oil prices. It has neither retreated much nor risen much. Thus while India is not in recession at the moment, it is not realizing any incremental benefit from falling oil prices.

This may be due in part because India has one of the lowest labor force participation rates in the G20, at 48.5% for the first quarter of 2023.

With more than half of its working-age population not engaged in the labor force, India very likely is not able to take full advantage of situations like falling oil prices to boost its industrial output. Rapid response would necessitate having a larger pool of unemployed workers ready to go to work, as opposed to workers who either never joined the labor force to begin working or had dropped out for whatever reason.

This is the one major economy that is not currently experiencing inflation, stagflation, and/or recession.

The reason oil prices keep slipping is that, thus far, there is no part of the global economy where oil demand is able to rise much above where it is now, and, by all outward data, oil demand is in decline in most parts of the world.

For the first time in a very long time, perhaps ever, we are seeing a synchronized economic slowdown and contraction that literally touches almost every major economy on the planet. It is no exaggeration to say that every major economy is in the same race to the economic bottom, with stagnant and declining oil prices being the primary outward symptom of the global economic decline.

OPEC and Russia, in the end, have no choice but to continue to cut production. There is little point in pumping out oil that the world is not prepared to buy at a comfortable price point for the seller. They will cut production and extend those production cuts until oil prices themselves bottom out and show a sustained rise. Only then will oil supply be in approximate balance with oil demand.

The price of oil will continue to fall until the race to the bottom has ended.

I live in a very cold area of a northern country. An EV would be totally useless for me most of the year.

OPEC has totally alienated the people that want to continue with ICE vehicles by decreasing production to increase profit.

Because of their total neglect and greed alienating their customers...... I will buy an EV just to help ruin OPEC one day.

It’s disgusting how manufactured wars are used to increase oil price and then OPEC makes it worse by decreasing production. I can hardly wait till all oil countries are broke.