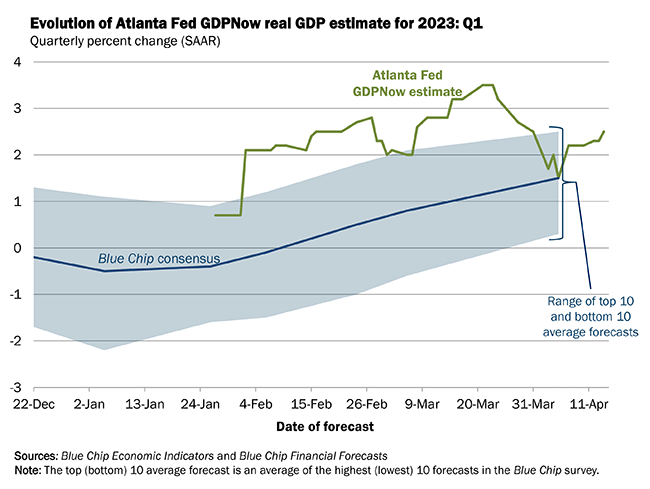

If we look at the Atlanta Federal Reserve’s GDPNow nowcast for US GDP growth, we see some apparently good news: GDP growth is presumably 2.5%.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2023 is 2.5 percent on April 14, up from 2.2 percent on April 10. After recent releases the US Bureau of Labor Statistics, the US Census Bureau, the US Department of the Treasury's Bureau of the Fiscal Service, and the Federal Reserve Board of Governors, the nowcasts of first-quarter real gross private domestic investment growth and first-quarter real government spending growth increased from -6.5 percent and 2.2 percent, respectively, to -5.9 percent and 2.6 percent.

While not indicative of an economy that is growing by leaps and bounds, the Atlanta Fed’s GDPNow nowcast shows an economy that is growing, not shrinking.

Does the data really agree with this?

Retail sales paint a somewhat muddled picture of economic growth.

According to the US Census figures, between January 2022 and January 2023, seasonally adjusted retail sales rose by over $49 Billion.

However, as the chart shows, between October and December of 2022, retail sales shrank by more than $13 Billion.

Moreover, from January 2023 through March 2023, seasonally adjusted retail sales shrank again, this time by over $8 Billion.

Put another way, March seasonally adjusted retail sales were $173 million less than in October, 2022.

It should be intuitively obvious that shrinking sales are incompatible with economic growth.

If we look at construction spending in the US, both as an aggregate total and broken out for residential and non-residential spending, we see that such spending (not seasonally adjusted) peaked variously between July and September of 2022, and has been declining ever since.

Declining construction spending is also incompatible with economic growth.

If we turn to manufacturing, we see that the value of new orders in manufacturing peaked on a seasonally adjusted basis in June of 2022, and has been declining ever since.

Declining new orders for manufactured goods is again incompatible with economic growth.

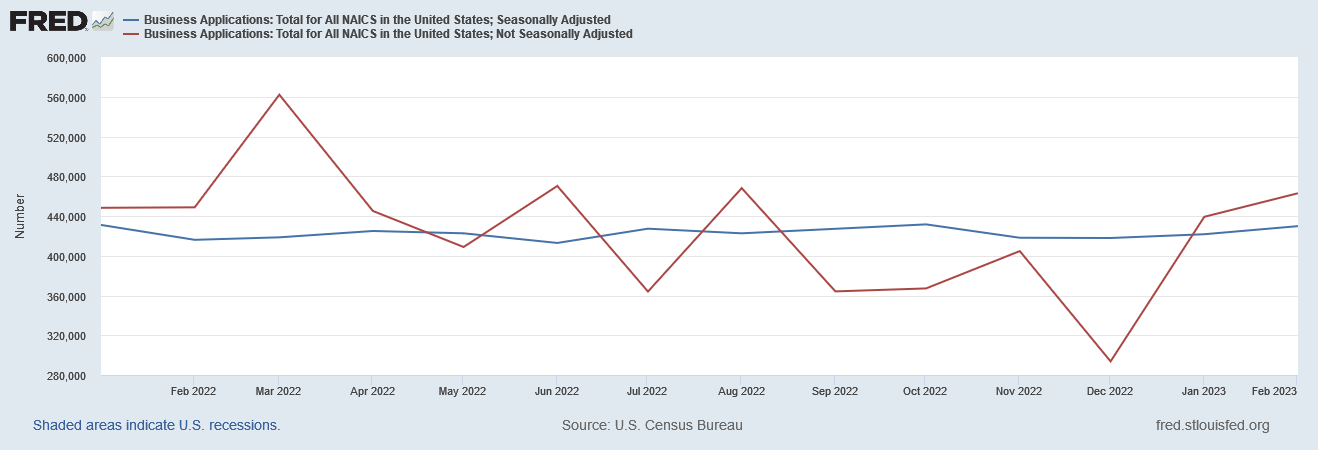

If we look at the Census’ tally for new business formations, as determined by applications for an Employee Identification Number (EIN), we get an extremely muddled picture.

If we look at the non-seasonally adjusted data, business applications declined generally from March through December of 2022, but recovered in the first 2 months of 2023 to achieve a marginal gain by February 2023 over January of 2022. However, the seasonally adjusted data shows a more gradual decline with no such recovery.

At a minimum, therefore, we have declining business formation (indicative of economic contraction, not expansion) between March and December of 2022, and depending on whether the seasonally adjusted or non-seasonally adjusted data is a more reliable representation of the situation, that decline has potentially persisted through February 2023.

These are not statistics that speak to sustained economic growth of any percentage.

Nor do the Census Bureau’s Indices of Economic Activity suggest a healthy and expanding economy for the US.

The aggregate index has been steadily declining since March of 2022.

So has the index for total construction spending.

Also the index for the value of manufacturing new orders.

And then there’s the index for the value of new orders for durable goods.

The index for new single-family homes for sale peaked in April of 2022 then began an extended decline.

The index for exported goods has also been declining.

As a general rule, an healthy economy sees things like exports increase, not decrease. Construction spending rises in an healthy economy. Home sales increase in an healthy economy. We are seeing declines and contractions on all these fronts.

A healthy economy is one that more or less fires on all cylinders. The US economy is clearly not firing on all cylinders.

To be sure, there are indicators showing areas of growth in the economy. The index for housing starts, for example, after moving mostly sideways throughout 2022, began 2023 by trending up.

Yet the US economy is not expressed solely by housing starts, nor by any other single economic metric. Nor is it wise to assess the economy solely on the basis of a monolithic GDP growth estimate (or even an estimate of GDP itself).

As we have seen time after time, again and again, the monolithic growth projections of the Atlanta Fed’s GDPNow nowcast fail completely to sustain any semblance of credibility. There are simply too many contradictory data points to accept the premise that the economy grew or is growing at the percentages presented. There are too many areas where economic growth is demonstrably not happening.

As we have seen repeatedly with each month’s data on consumer price inflation, the US economy has grown increasingly unbalanced and distorted, and is still unbalanced and distorted.

The Fed’s rate hike strategy has completely failed to resolve the distortion. Federal Reserve Governor Christopher Waller recently said as much publicly, describing core inflation’s movement as “sideways”.

Since the end of 2021, "core inflation has basically moved sideways with no apparent downward movement," Waller said in a prepared speech at the Graybar National Training Conference in San Antonio, Texas. On Wednesday, the Department of Labor said core CPI, which excludes volatile food and energy prices, jumped 5.6% Y/Y in March, compared with the 5.5% rise in February.

If core inflation has moved “sideways”, as Waller asserts, then not only has the Fed’s strategy failed to bring the economy back into balance, it has also failed to resolve inflation at all.

To be sure, the data does show that core inflation as measured by the Consumer Price Index for All Items Less Food and Energy has neither risen nor fallen in lockstep with headline consumer price inflation. Chris Waller has at least that much accuracy in his comments.

Arguably, one could say that core inflation has hovered around the 6% year on year level since January of 2022—that is both the median and average of the year on year percentage change for the Consumer Price Index for All Items Less Food and Energy.

This is a nuance that is not reflected in the GDPNow nowcast. It is not a nuance that could ever be reflected in a single monolithic number.

Which is why it is never advisable to simply go by a single growth metric or a single growth estimate. It is never enough to simply say “the economy grew by 2.5% last quarter” or even “the economy shrank by 0.5% last quarter”. To accurately apprehend the state of any economy, one has to have at least some understanding of what individual sectors and components of that economy are doing, where they are growing, and especially where they are not.

As the US Census data illustrates, there are many sectors of the US economy that are not growing, but are instead shrinking. The rising tide of economic growth is demonstrably not lifting all ships.

the "new housing starts" metric includes public housing, am i right?

if so that would explain the upward bump - cheap highrises near the commuter train to fulfill 15-minute prison goals https://www.save1familyny.org/about.html